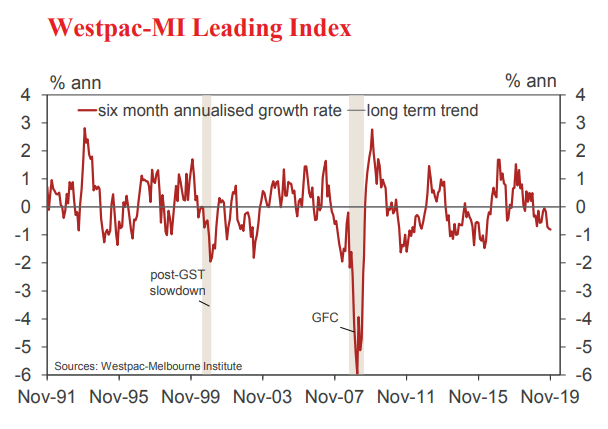

The six month annualised growth rate in the Westpac– Melbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, fell from –0.78% in October to –0.81% in November.

The Leading Index growth rate has now been below trend for the last twelve months and continues to point to weak economic momentum carrying well into 2020.

This signal from the Index is certainly consistent with Westpac’s own growth forecasts. We expect GDP growth in 2020 to be stuck at 2.1% which compares with trend growth of 2.75%.That modest growth pace reflects a flat consumer; further contraction in residential construction and disappointing business investment.

The Leading Index growth rate has deteriorated over the last six months from –0.17% in June to –0.81% in November. The main components driving the 0.64ppt shift have been a sell-off in commodity prices (–0.65ppts) and a more mixed performance on the Australian share market (–0.28ppts). The period has also seen a slightly bigger drag from renewed weakness in dwelling approvals (–0.08ppts) and the Westpac-MI Consumer Expectations Index (–0.05ppts). This has been partially offset by a widening yield spread as the RBA’s cuts in the cash rate have lowered short term rates (+0.23ppts) and a reduced drag from US industrial production (+0.15ppts).

The Reserve Bank Board next meets on February 4. The minutes of the December Board meeting strengthen our conviction that the Board is likely to ease rates further at the February meeting. The flow of economic data over the next six weeks will be critical to that decision, particularly updates around the labour market, retail sales and confidence. Given our forecasts, Westpac is comfortable with our current view that the RBA will reduce the cash rate from 0.75% to 0.50% at the February Board meeting.

Went to the mall last night. 80% all over the joint.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.