Oil appears to want more shale, which it does not need:

Advertisement

Metals are still meh:

Miners rolled:

Advertisement

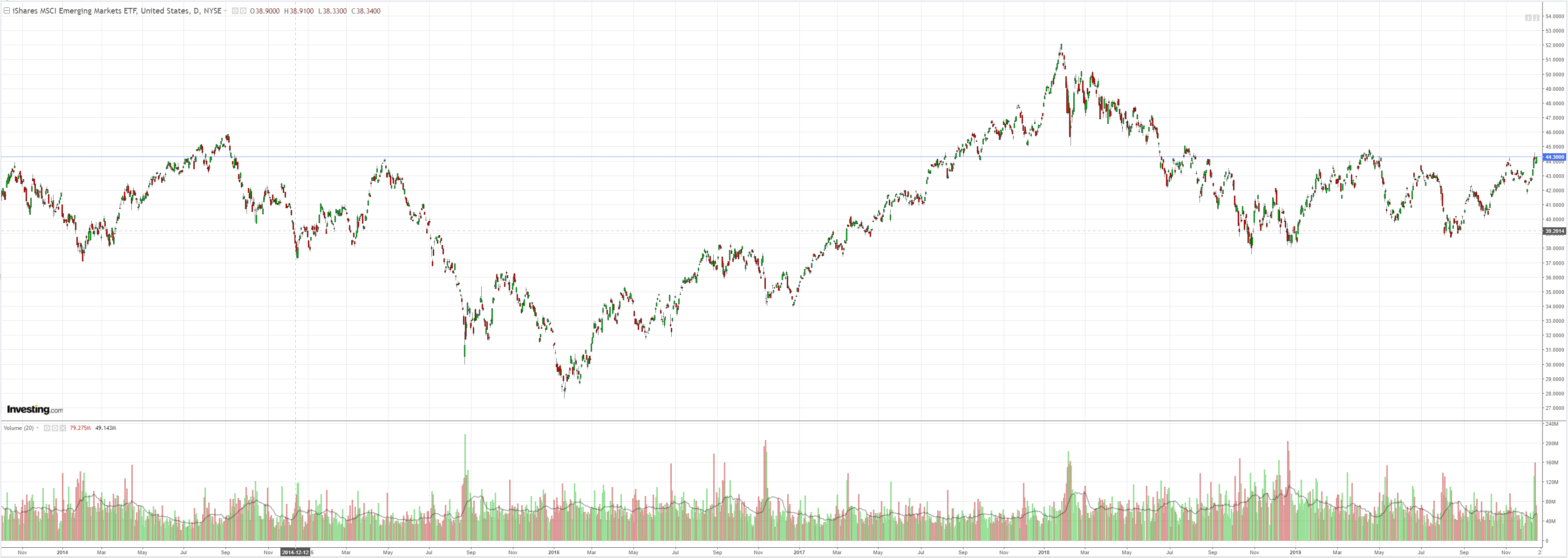

EM stocks jumped:

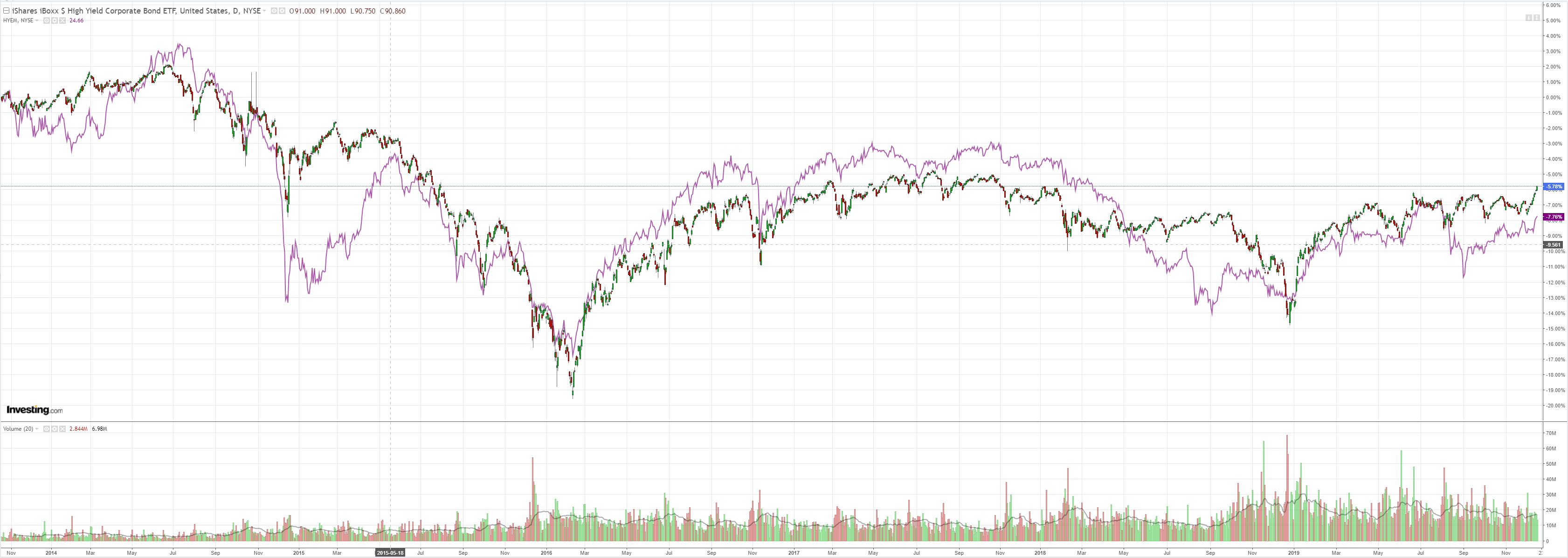

With junk:

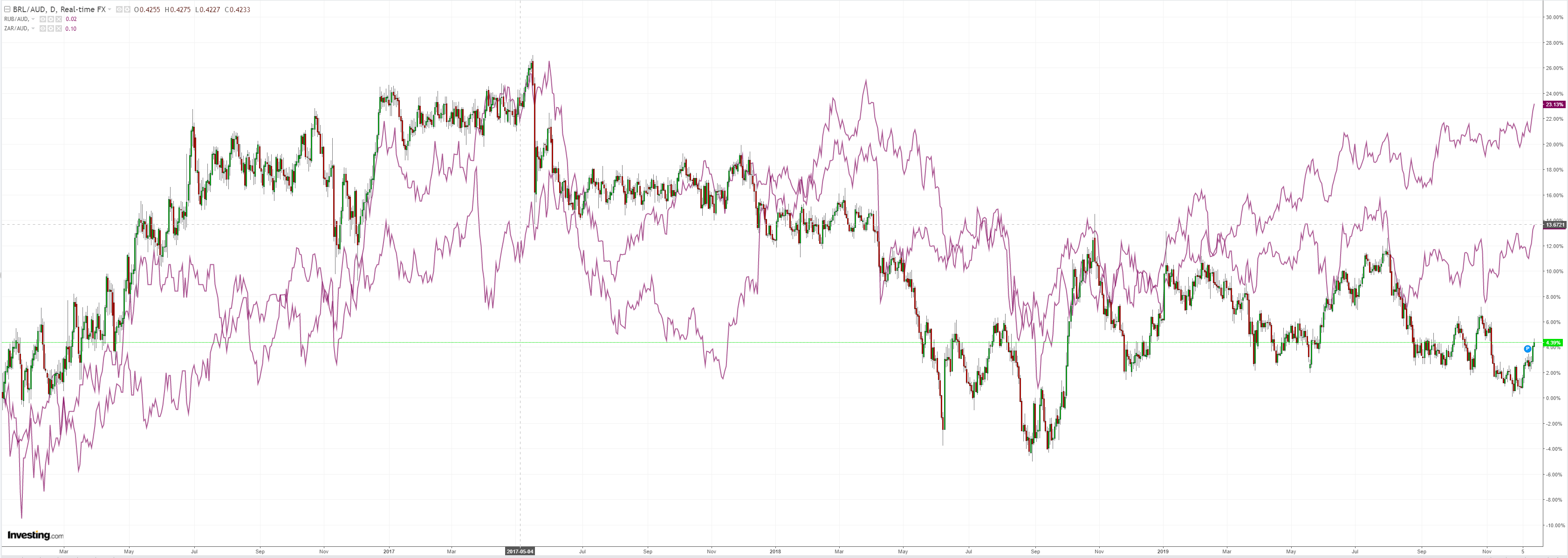

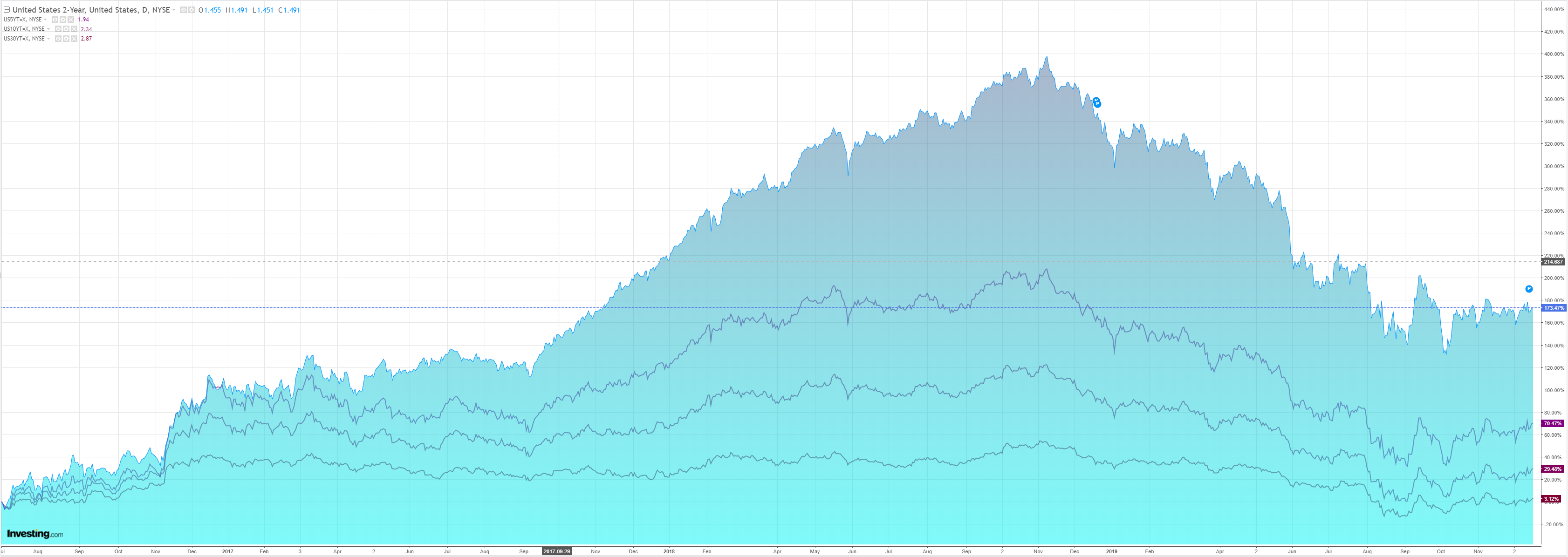

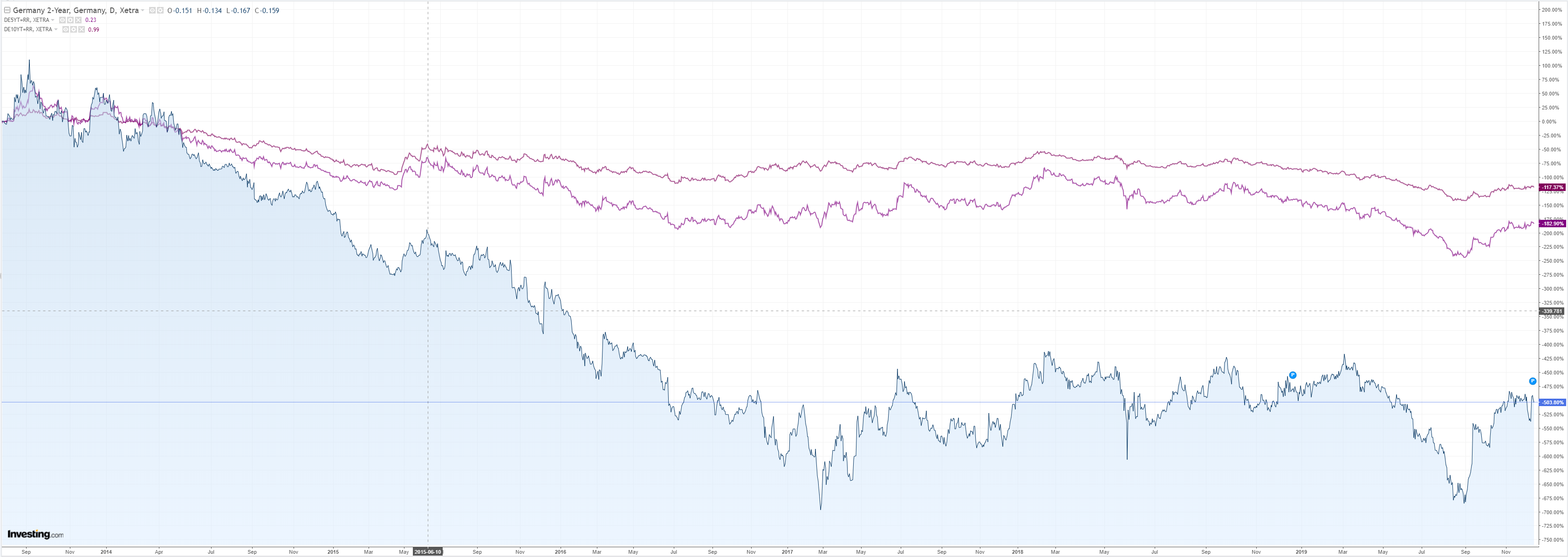

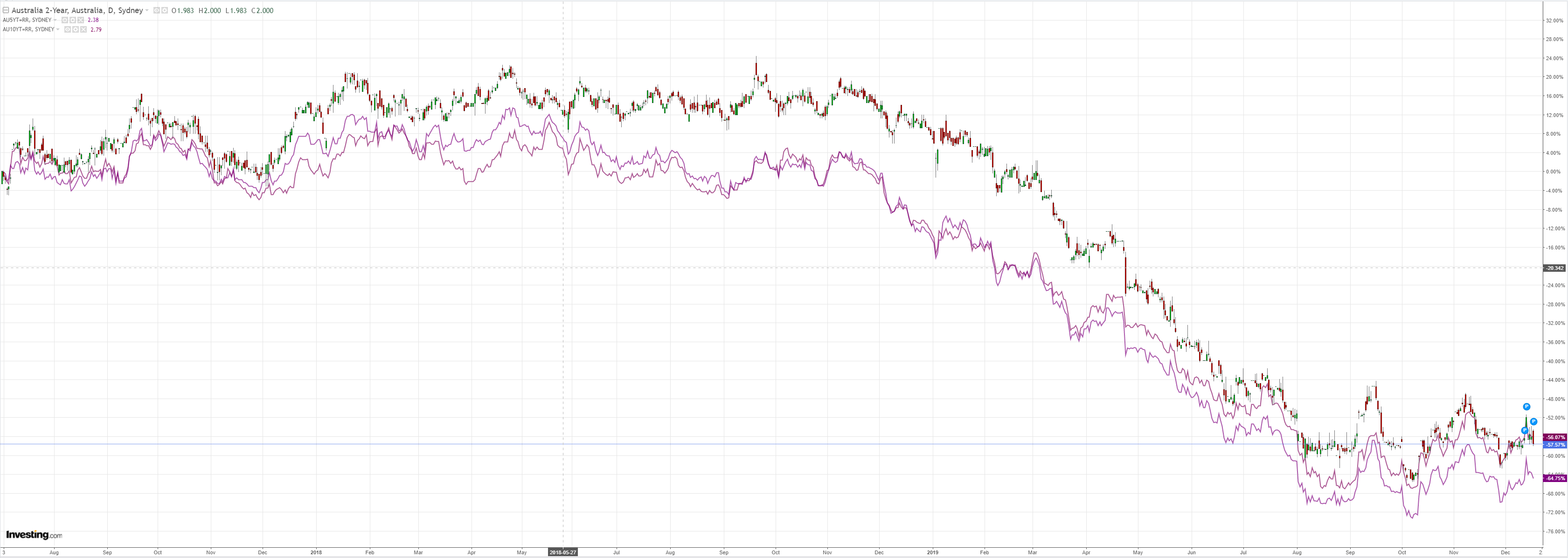

Bonds were a mix:

Advertisement

Stocks were still bid:

Westpac has the wrap:

Event Wrap

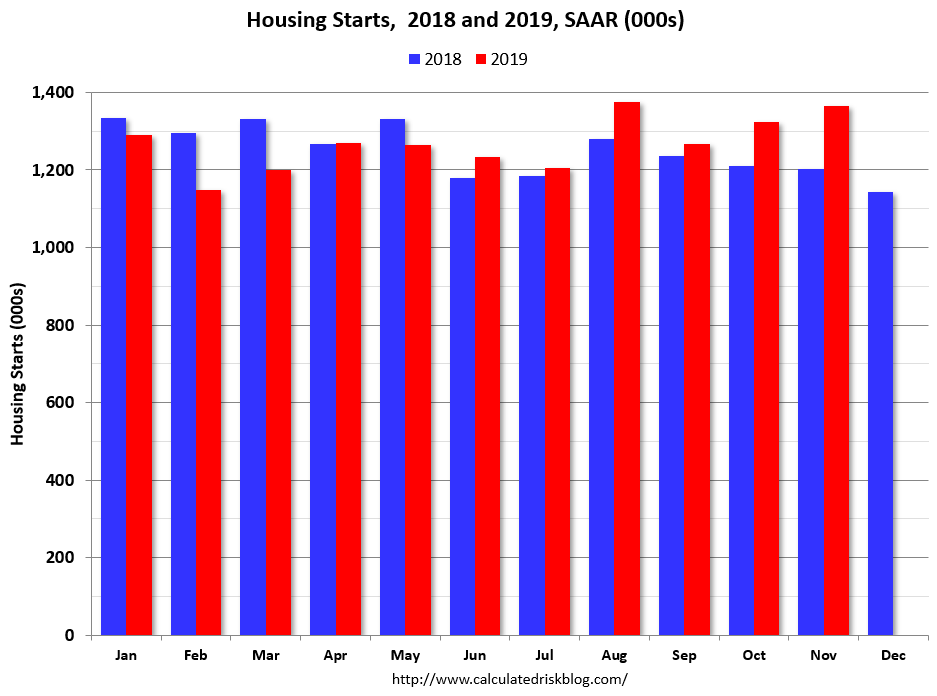

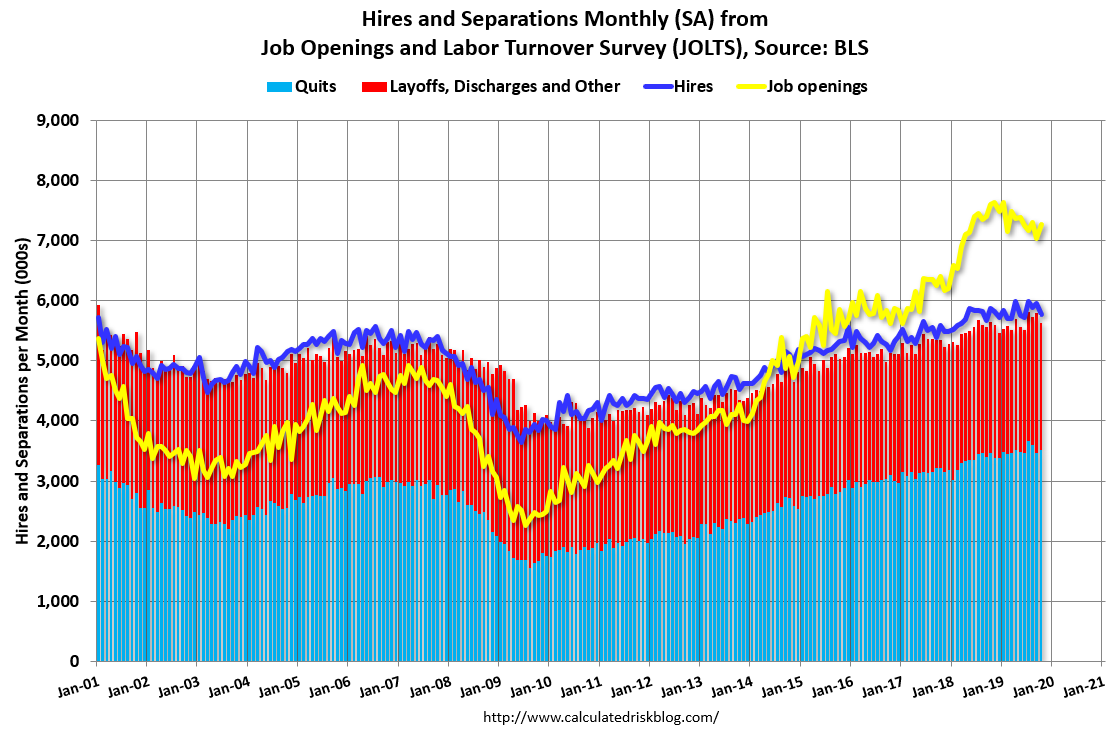

US industrial production rose 1.1% in Nov (vs 0.9% expected), as the impact of the GM strike and California fires and power cuts reversed. Housing starts rose 3.2% in Nov (vs 2.4% expected). JOLTS job openings rose 235k to 7.267m (vs expectations at 7.009m), consistent with the strong jobs market.

Event Outlook

NZ: The Q3 current account is expected to remain at -3.4% GDP, although upward revisions to GDP could increase the number. Goods trade volume fell but so too did profit remittances overseas.

Australia: Westpac-MI Leading Index is released.

Europe: ECB President Lagarde speaks in Frankfurt. Dec IFO business climate is anticipated to edge up to 95.5 from 95.0 in Nov.

UK: Nov CPI is expected to show annual core inflation hold at 1.7%.

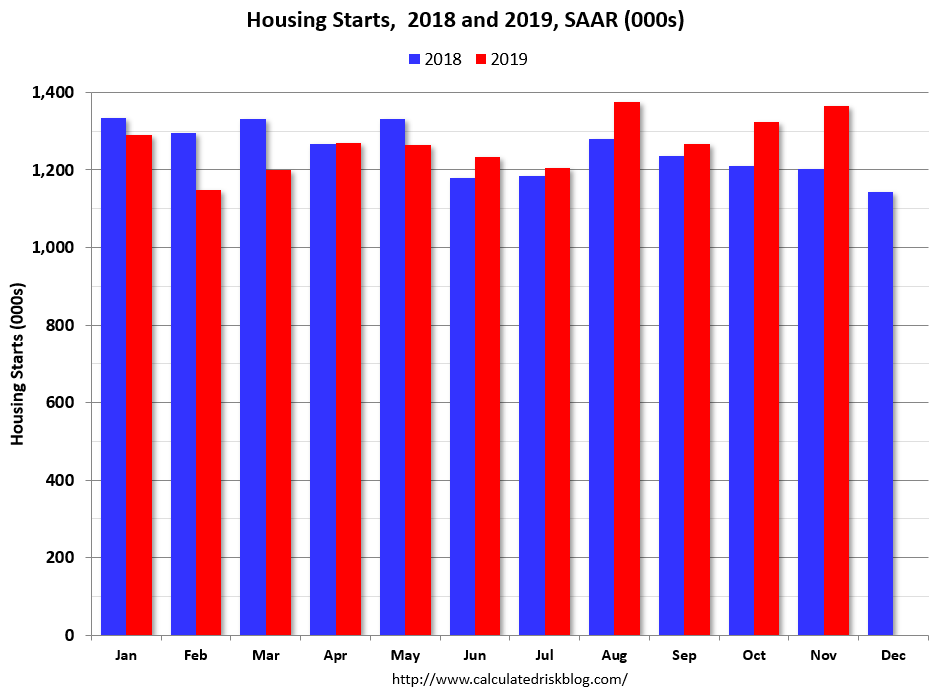

Housing Starts:

Privately‐owned housing starts in November were at a seasonally adjusted annual rate of 1,365,000. This is 3.2 percent above the revised October estimate of 1,323,000 and is 13.6 percent above the November 2018 rate of 1,202,000. Single‐family housing starts in November were at a rate of 938,000; this is 2.4 percent above the revised October figure of 916,000. The November rate for units in buildings with five units or more was 404,000.

Building Permits:

Privately‐owned housing units authorized by building permits in November were at a seasonally adjusted annual rate of 1,482,000. This is 1.4 percent above the revised October rate of 1,461,000 and is 11.1 percent above the November 2018 rate of 1,334,000. Single‐family authorizations in November were at a rate of 918,000; this is 0.8 percent (±1.3 percent)* above the revised October figure of 911,000. Authorizations of units in buildings with five units or more were at a rate of 524,000 in November.

JOLTS were terrific:

The number of job openings edged up to 7.3 million (+235,000) on the last business day of October, the U.S. Bureau of Labor Statistics reported today. Over the month, hires and separations were little changed at 5.8 million and 5.6 million, respectively. Within separations, the quits rate was unchanged at 2.3 percent and the layoffs and discharges rate was little changed at 1.2 percent. …

The number of quits was little changed in October at 3.5 million and the rate was unchanged at 2.3 percent. Quits increased in other services (+66,000) and educational services (+12,000). Quits decreased in retail trade (-63,000) and in durable goods manufacturing (-21,000).

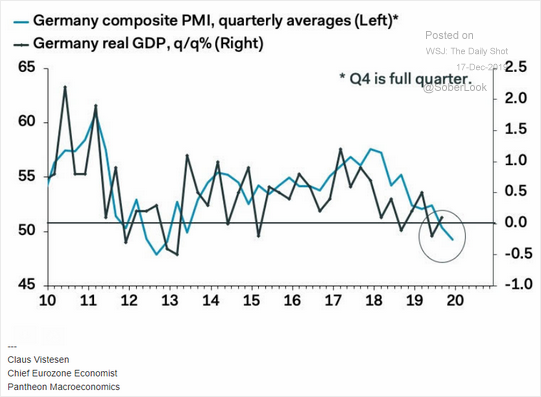

Meanwhile, Europe is going nowhere:

Advertisement

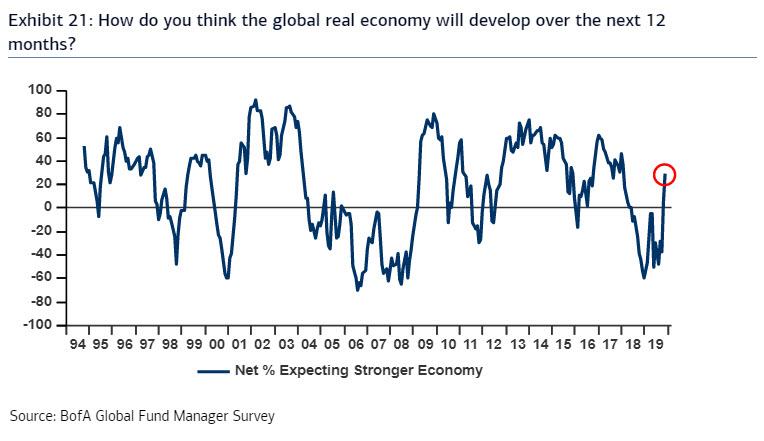

But there is hope that the combined US and China bounces, weak as they are, will finally have an impact:

That’s the hope of global fundies, via BofML:

Advertisement

The problem will eventually be it’s not enough for profits:

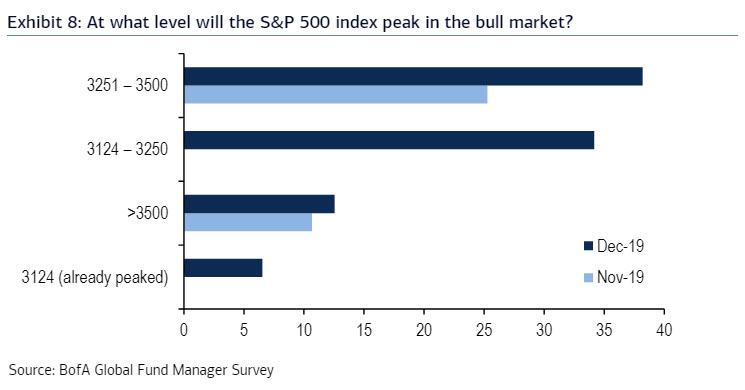

But it’s all in for now:

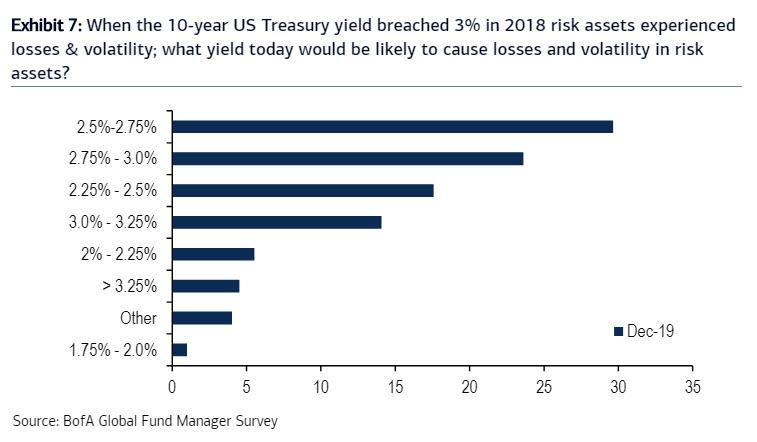

Until bond yields rise:

But what if they don’t? There’s not enough stimulus yet. The US is only growing moderately. Chian will keep slowing. Europe’s rebound will be modest.

Quantitative failure is more a risk than quantitative success. Especially in Australia where monetary policy efficacy has collapsed for the real economy.

There’s still no reason to own the Australian dollar.

——————————————-

David Llewellyn-Smith is Chief Strategist at the MB fund and MB Super which is overweight international shares that will benefit from a falling Australian dollar.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

{kind=link}