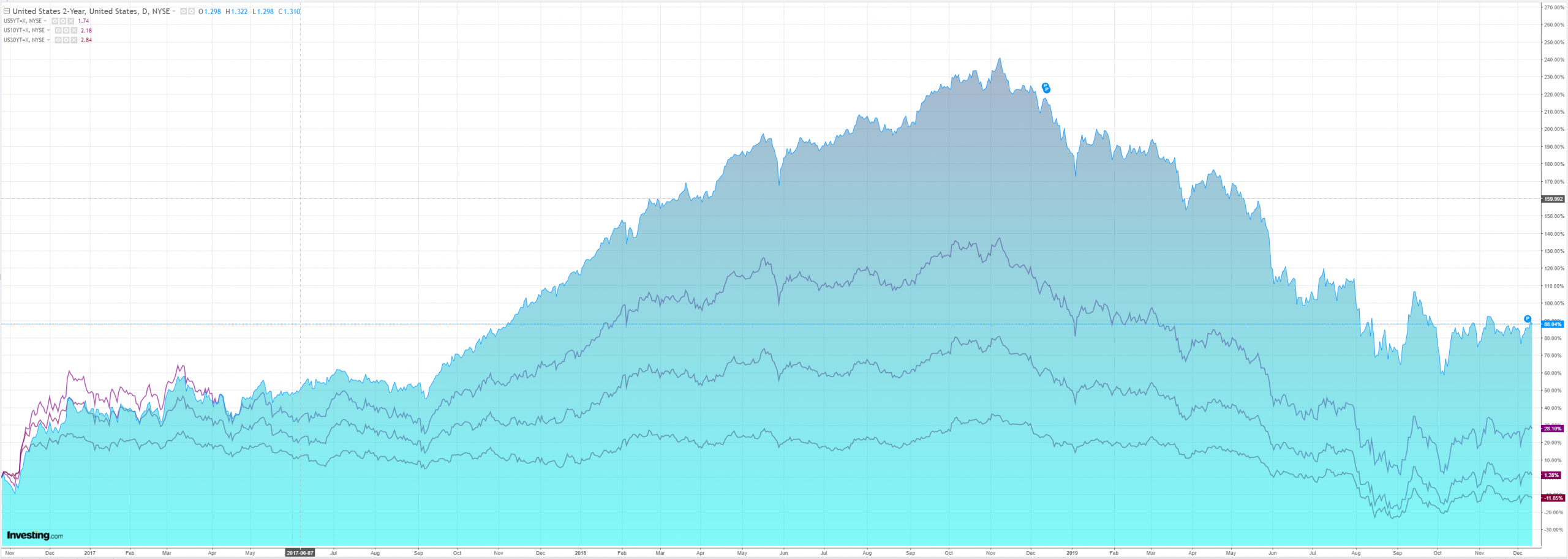

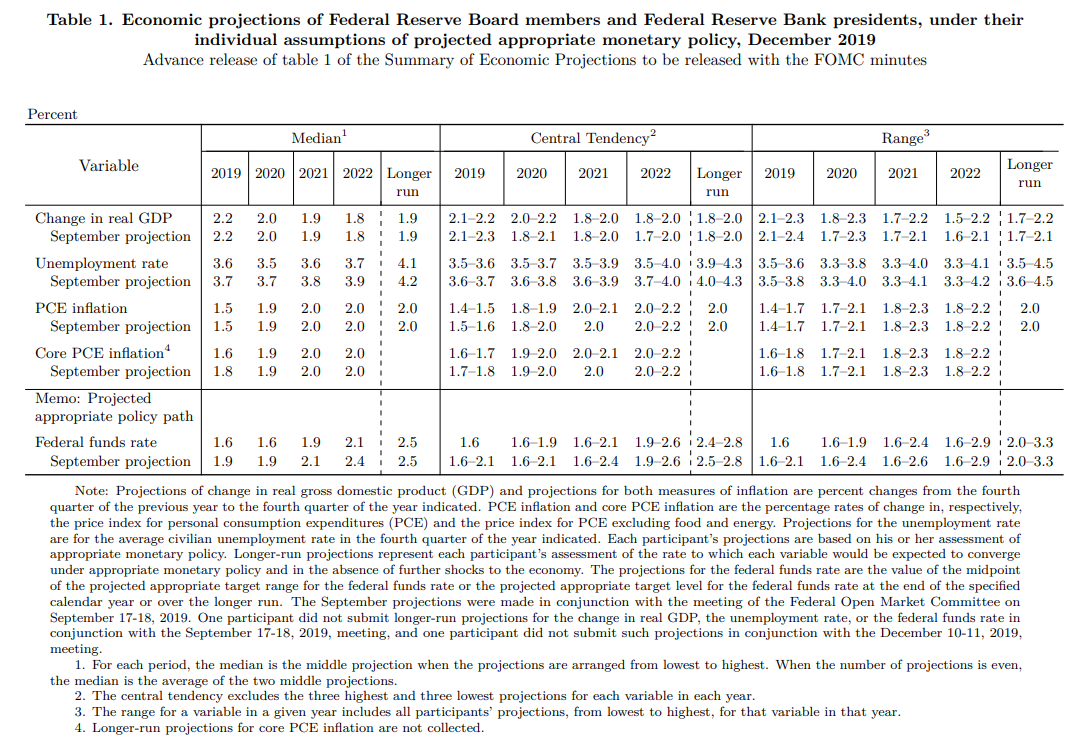

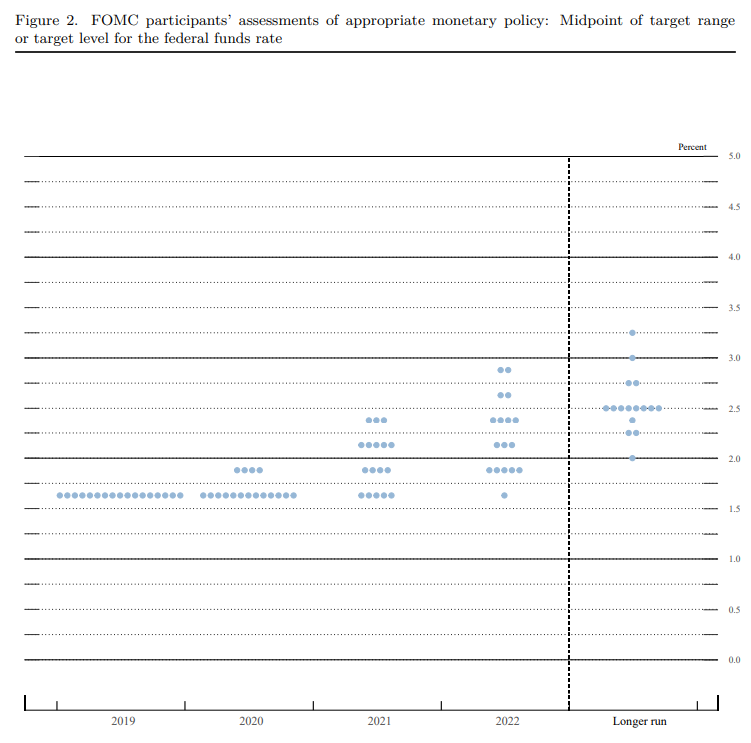

The US Federal Reserve kept the funds rate range unchanged at 1.50%-1.75% as was widely expected. The Fed said the “current stance of policy is appropriate,” and that it will continue to monitor upcoming information to “assess the appropriate” path of policy. That suggests policy is on hold until there is a material change in the outlook. The dot plot projections show the funds rate unchanged at end-2020, and then rising towards 2.5% over the long run. The policy statement was largely a reiteration of October’s, noting the labour market remains strong and economic activity has been rising at modest rate, while inflation and inflation expectations remain low. The vote was a unanimous 10-0.

US Nov CPI rose 0.3% (vs 0.2% expected), with the core up 0.2% (as expected), taking the annual pace to 2.1% (vs previous at 1.8%), and 2.3% core. All of the main components posted small gains, with energy prices leading the increases.

Event Outlook

NZ: Oct migration and Nov food prices are released.

Australia: the RBA bulletin of research articles are released.

Europe: the ECB policy decision is widely expected to unchanged. This is new President Lagarde’s first meeting and will also involve the quarterly update to macroeconomic projections.

UK: the General Election takes place tonight. Polling is open from 7am to 10pm GMT (6pm to 9am Friday AEDT). Exit polls are released at 10pm and the vote count typically ends around 2am GMT on Friday (1pm AEDT). Bookies odds currently imply around a 65% chance of a Conservative majority.

The Fed moved all:

Advertisement

Information received since the Federal Open Market Committee met in October indicates that the labor market remains strong and that economic activity has been rising at a moderate rate. Job gains have been solid, on average, in recent months, and the unemployment rate has remained low. Although household spending has been rising at a strong pace, business fixed investment and exports remain weak. On a 12‑month basis, overall inflation and inflation for items other than food and energy are running below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee decided to maintain the target range for the federal funds rate at 1‑1/2 to 1-3/4 percent. The Committee judges that the current stance of monetary policy is appropriate to support sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective. The Committee will continue to monitor the implications of incoming information for the economic outlook, including global developments and muted inflation pressures, as it assesses the appropriate path of the target range for the federal funds rate.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

The FOMC held rates and its projections showed no move either way for 2020. I would read this as slightly hawkish given markets have been pricing more rate cuts. But that’s not how the market saw it, taking it as dovish and buying reflation in every way possible.

That’s the key. The market wants reflation and the Fed didn’t stand in its way so that was enough to bid everything.

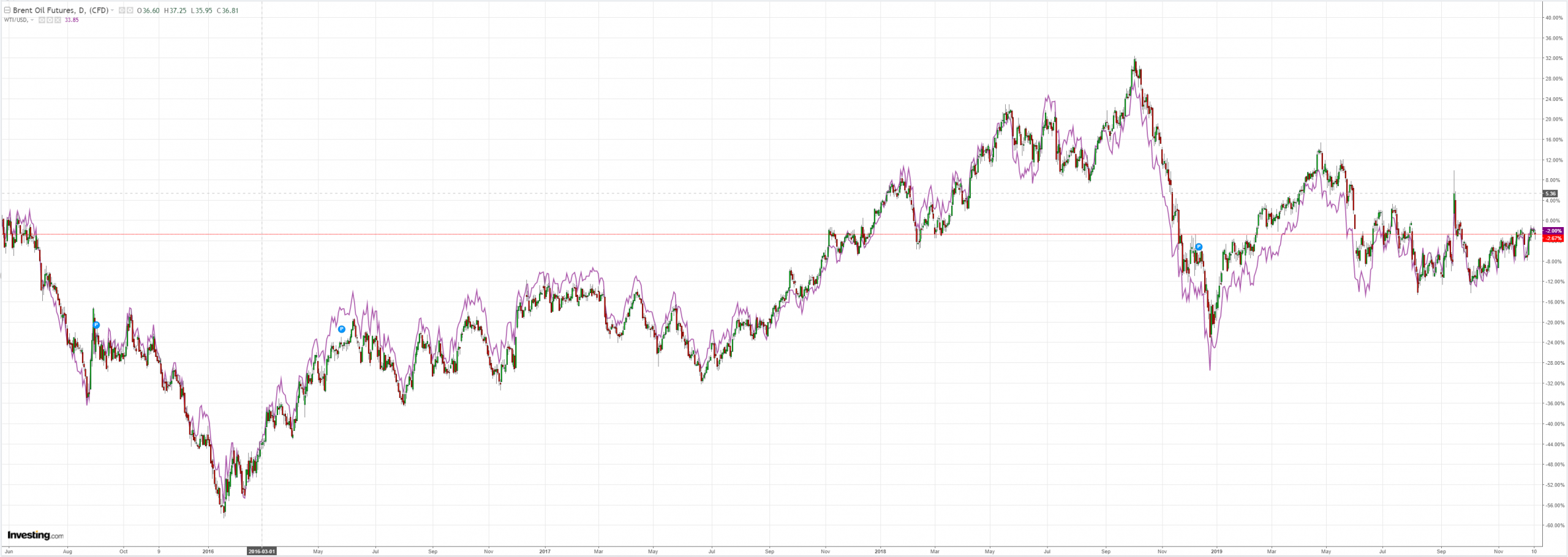

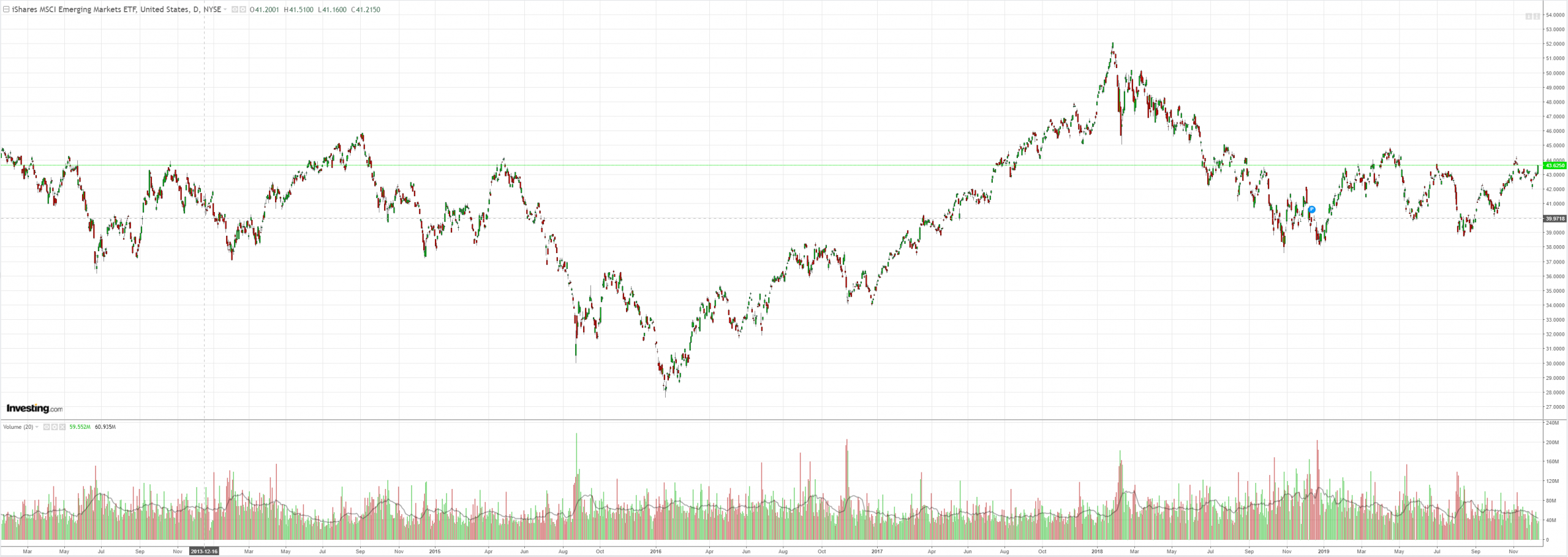

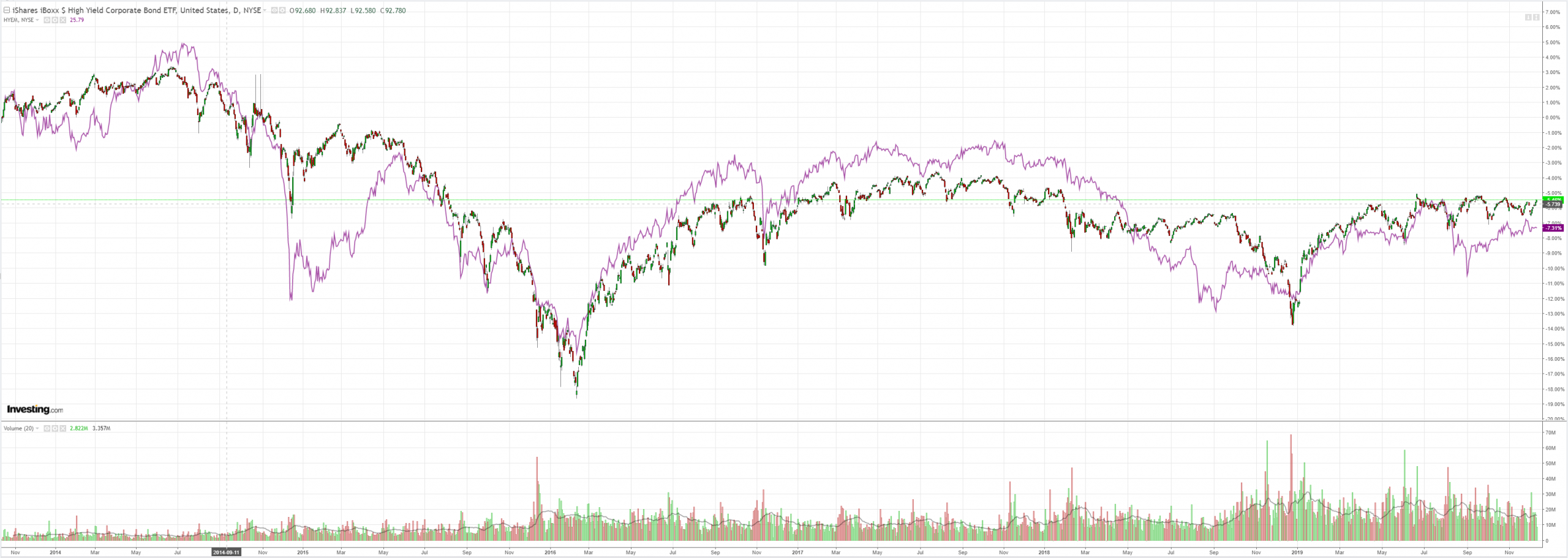

Whenever global growth rebounds, DXY tends to fall and the consequences are easy to predict. EUR rises. EM’s get bid. Junk debt rises. Commodites follow. The Australian dollar behaves like the Fed is its central bank.

Advertisement

I still have little faith in the great 2020 global growth recovery but the market doesn’t care for now. It’s got the sniff of reflation and is ready to price perfection.

The Australian dollar fills its spinnaker while such a gale blows.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.