DXY was up strongly Friday night as EUR sank:

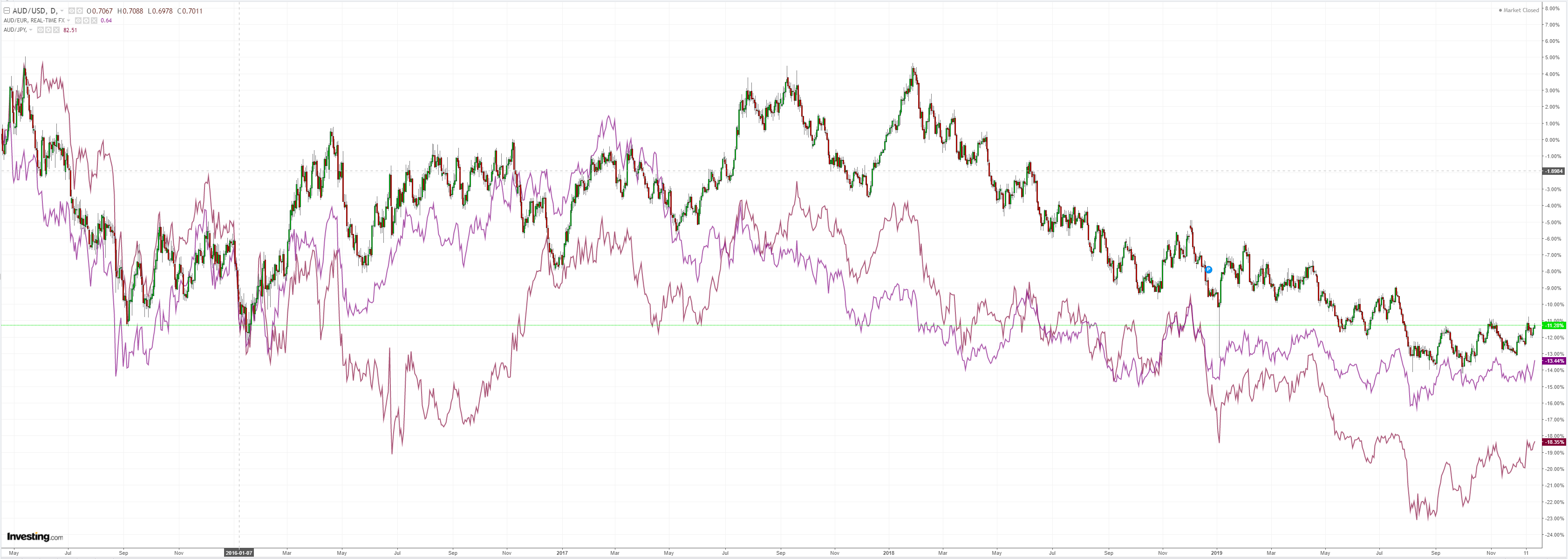

The Australian dollar jumped anyway versus DMs:

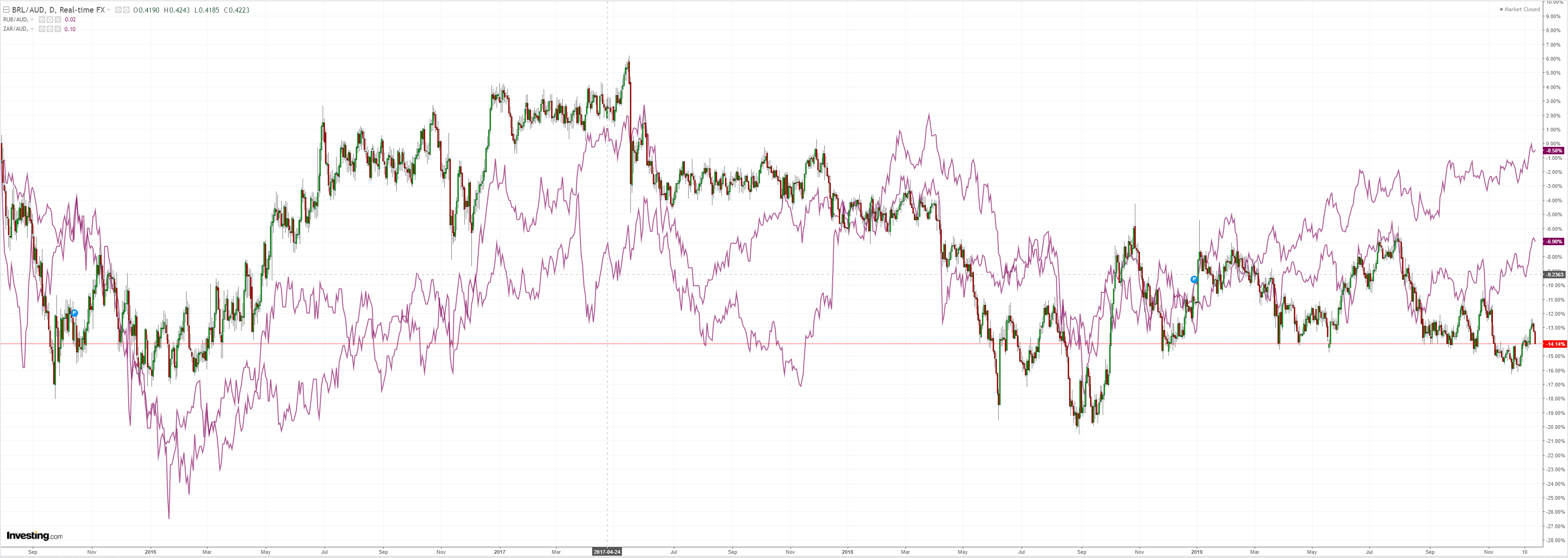

And EMs:

Surprisingly, net positioning on the CFTC moved more short last week to -46k contracts, though the trend is clearly towards more neutral:

Gold held on:

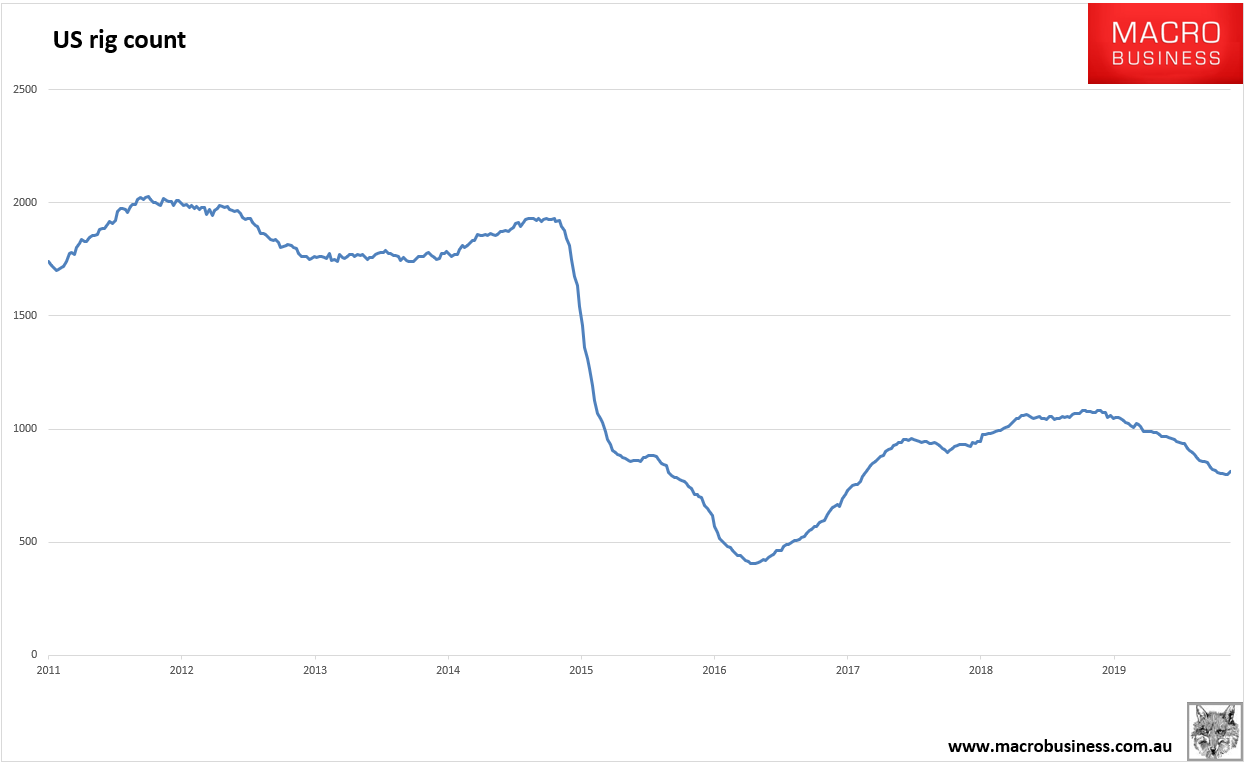

Brent fell as the US rig count jumped. The market does not need more oil:

Metals are trying:

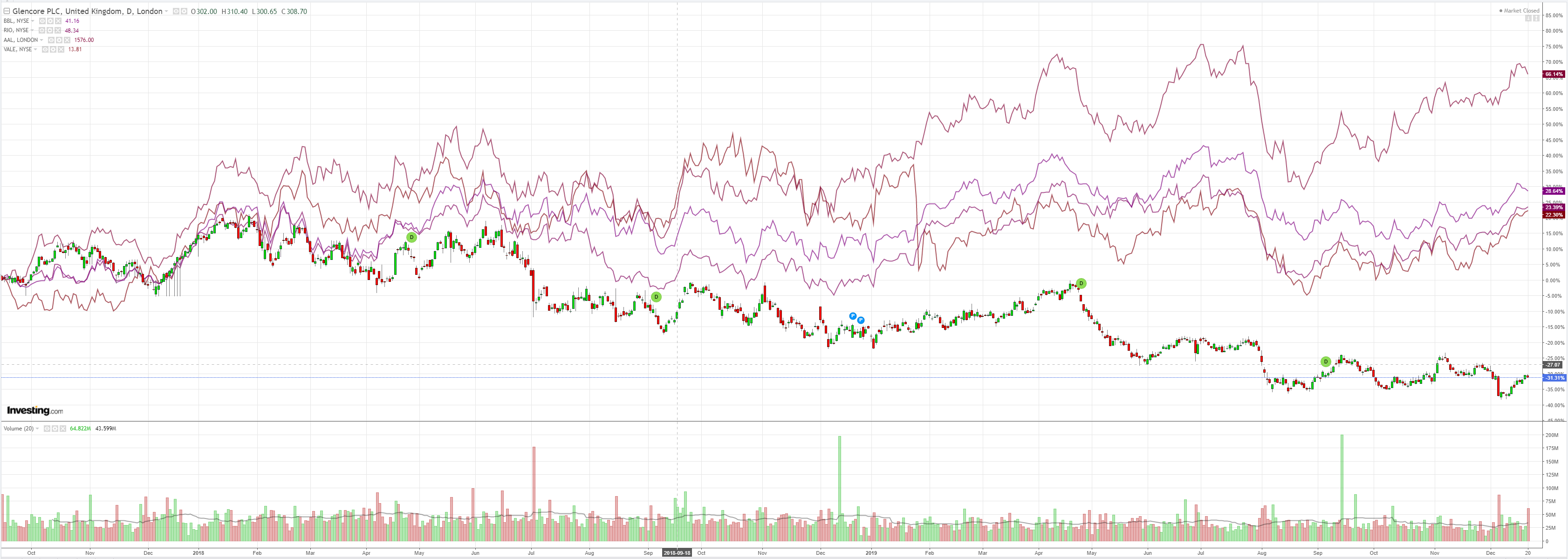

Miners struggled:

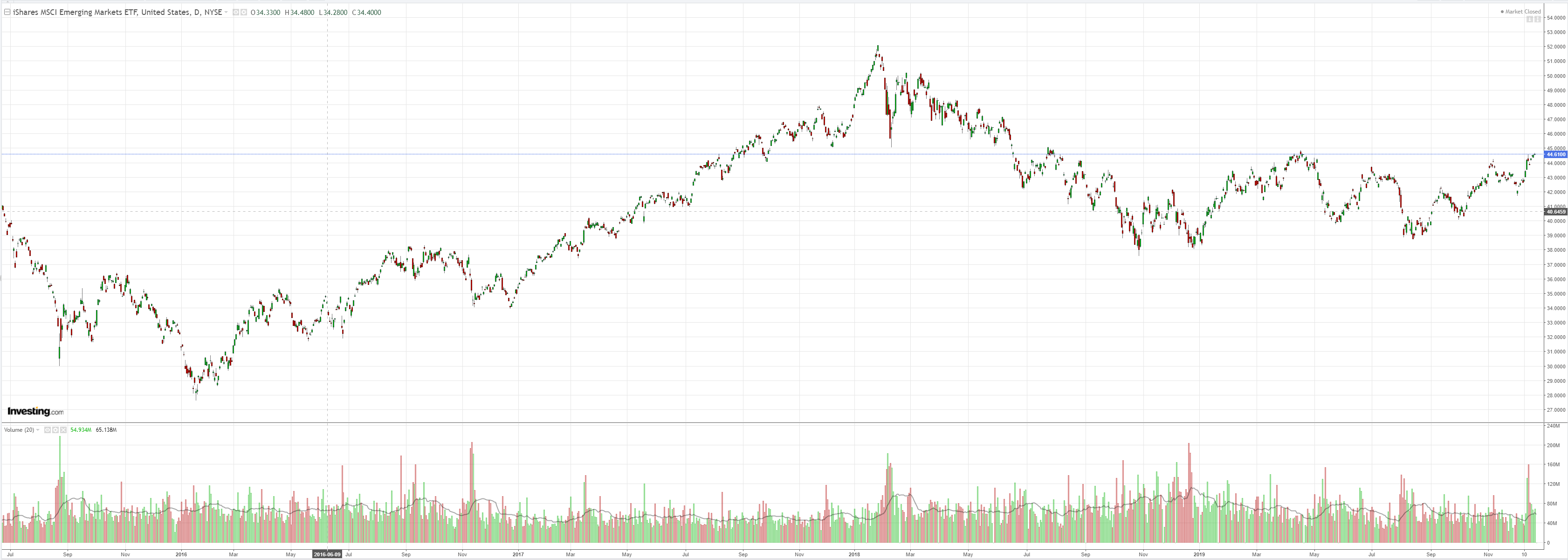

EM stocks are breaking out:

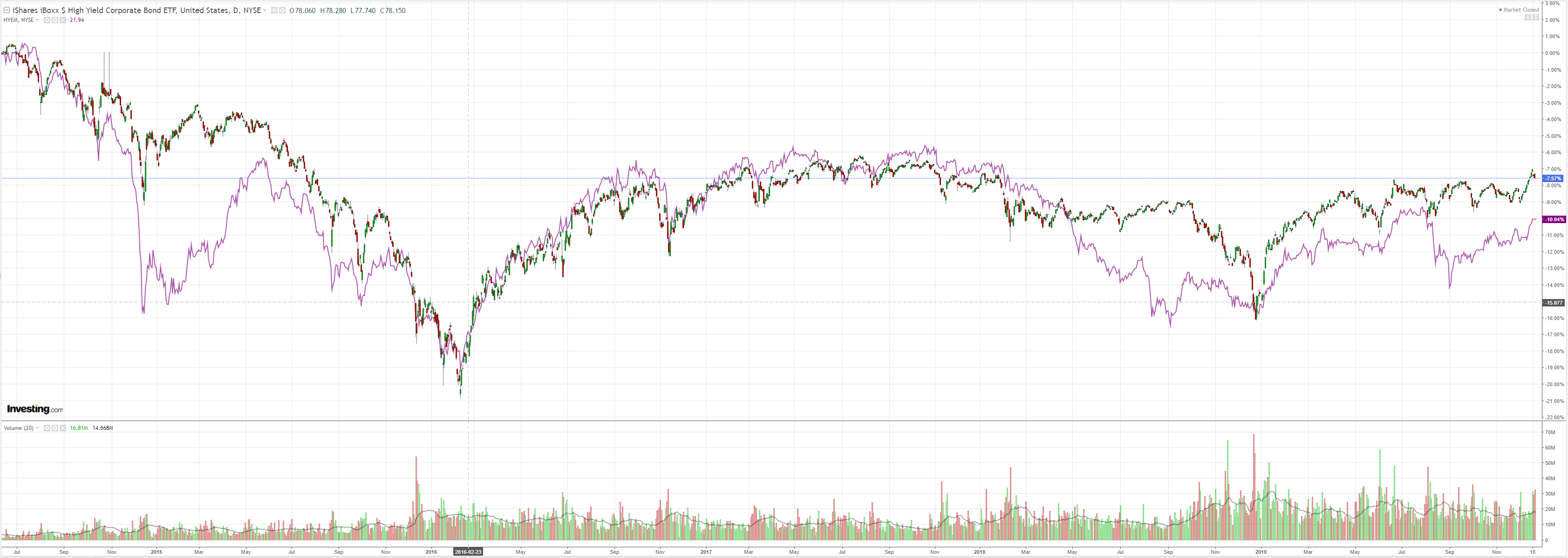

Junkk fell with oil:

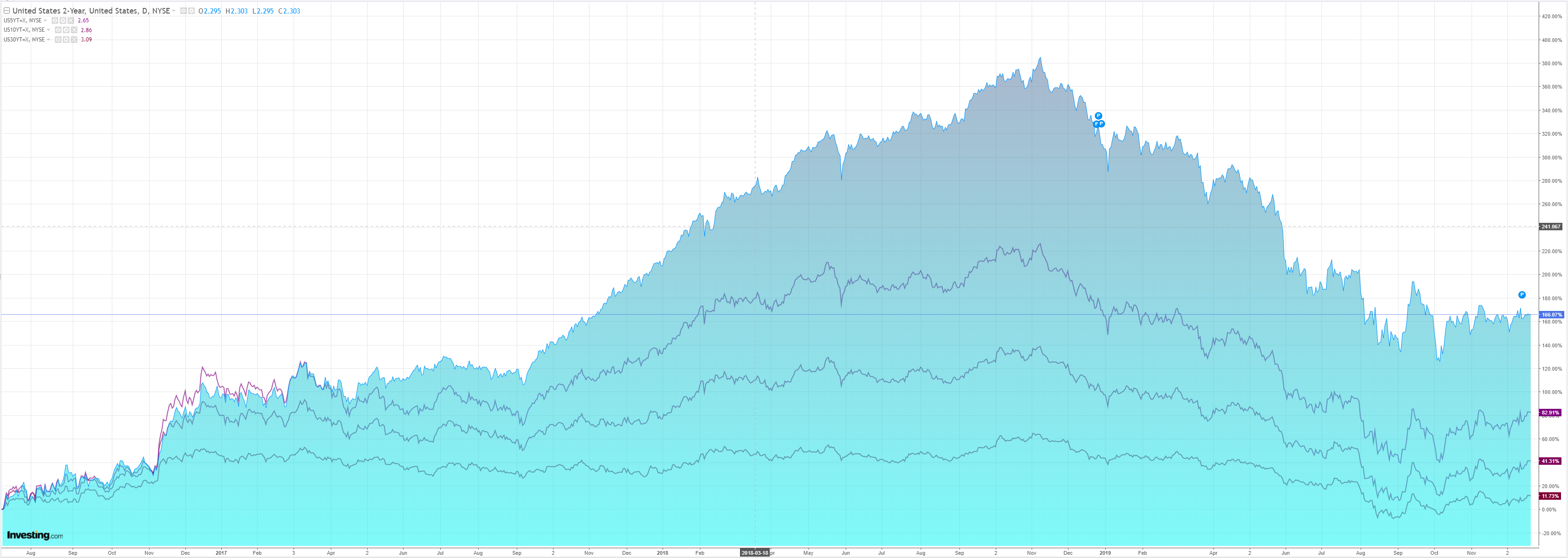

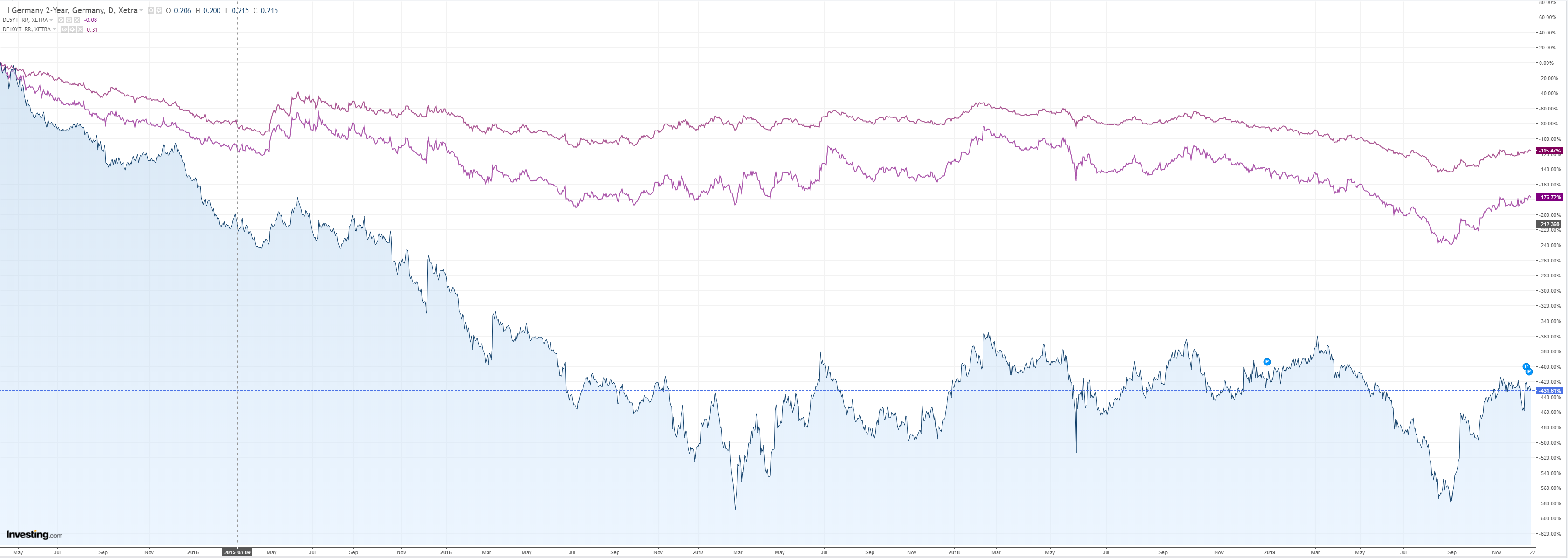

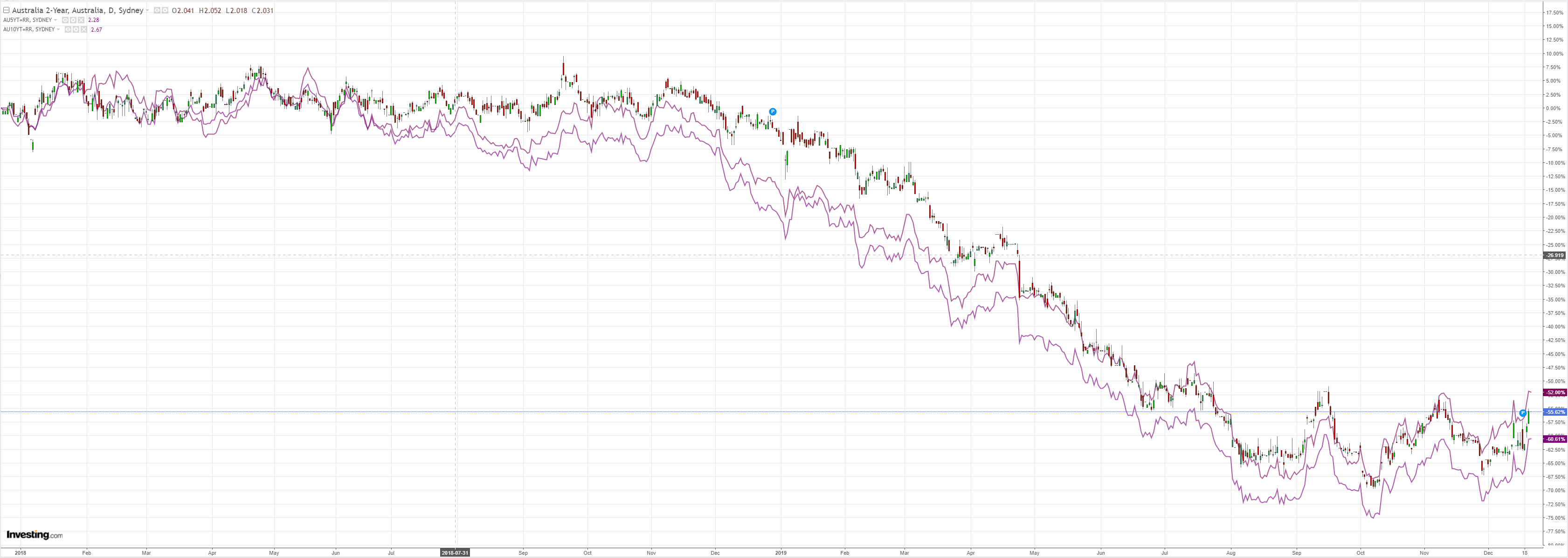

Bonds were mostly bid:

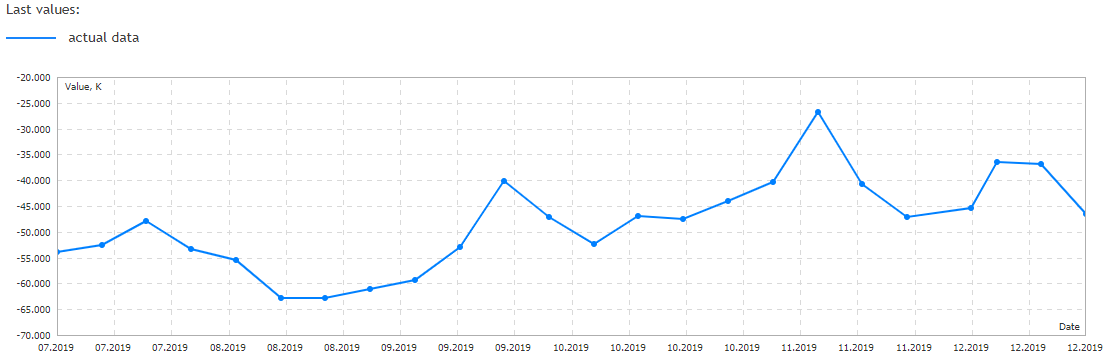

But not Aussie. That ABS numberwang report came at a bad time:

Nothing can stop stocks:

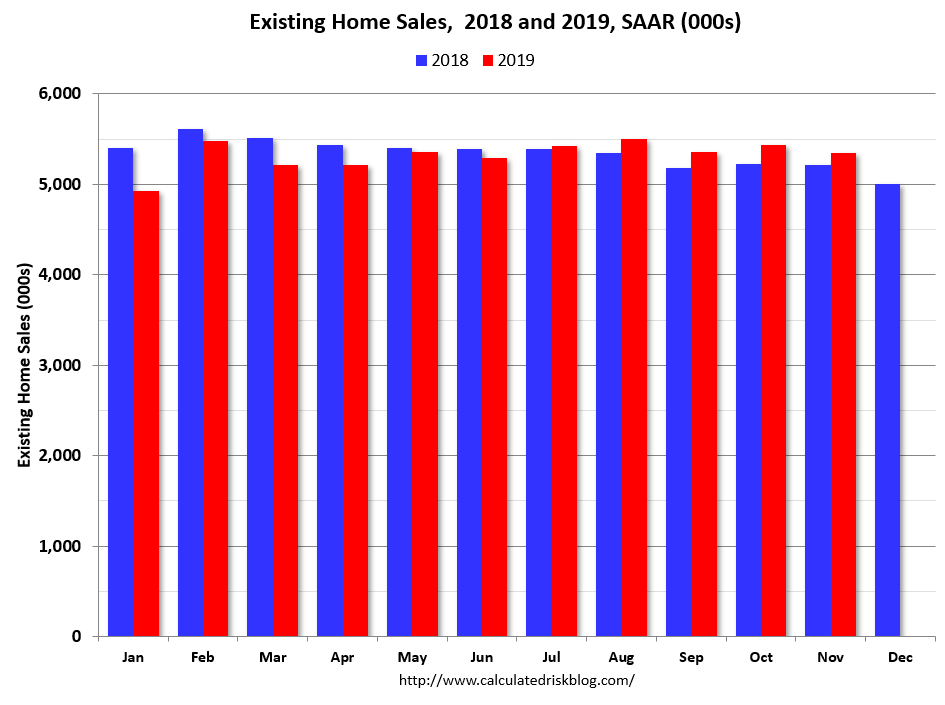

The US economy has been a story of two markets over 2019. The demand side has been strong with rising house prices, wages and consumption:

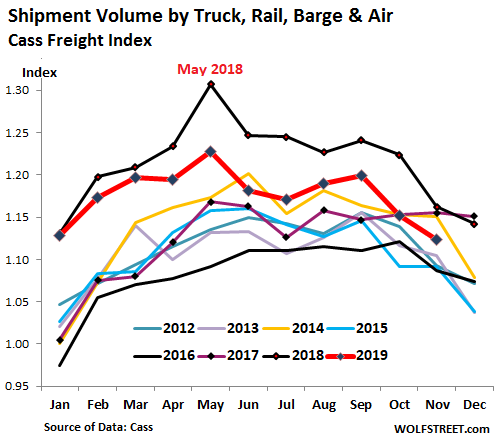

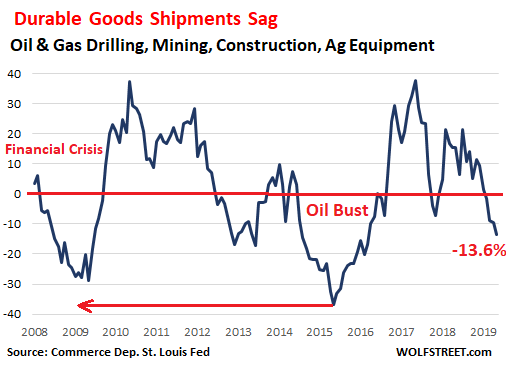

The supply side has been weak as global manufacturing slumped. Moreover, as growth has slowed, the latter has dragged down a lot of oil demand resulting in prices low enough to shake out US shale:

If the global reflation rally is now going to lift oil enough to bring more US drilling then this headwind is going to reverse.

And the USD is going to stay strong.

But so is the Australian dollar as commodities are bid, at least until markets work out that the without a falling USD there won’t be much global reflation to speak of.

They do not appear to be there yet. And with AUD market positioning remaining still quite short despite the recent bid, the path of least resistence reamins up in ths short term for the AUD as well.

This seems to be a pretty good time to be getting short. Even if there is a modest global reflation Australia is going to sit it out as unemployment rises and the RBA does more.

As well, the corrections coming to bulk commodities are as much about normalising supply as they are any impacts from the demand side so that is a nice back-up for an AUD headwind.

Thart gives you the two key inputs into AUD value both turning to headwinds pretty quick.