DXY was stable last night:

The Australian dollar spiked on ABS jobs numberwang:

Gold is still holding up:

Oil is off and running:

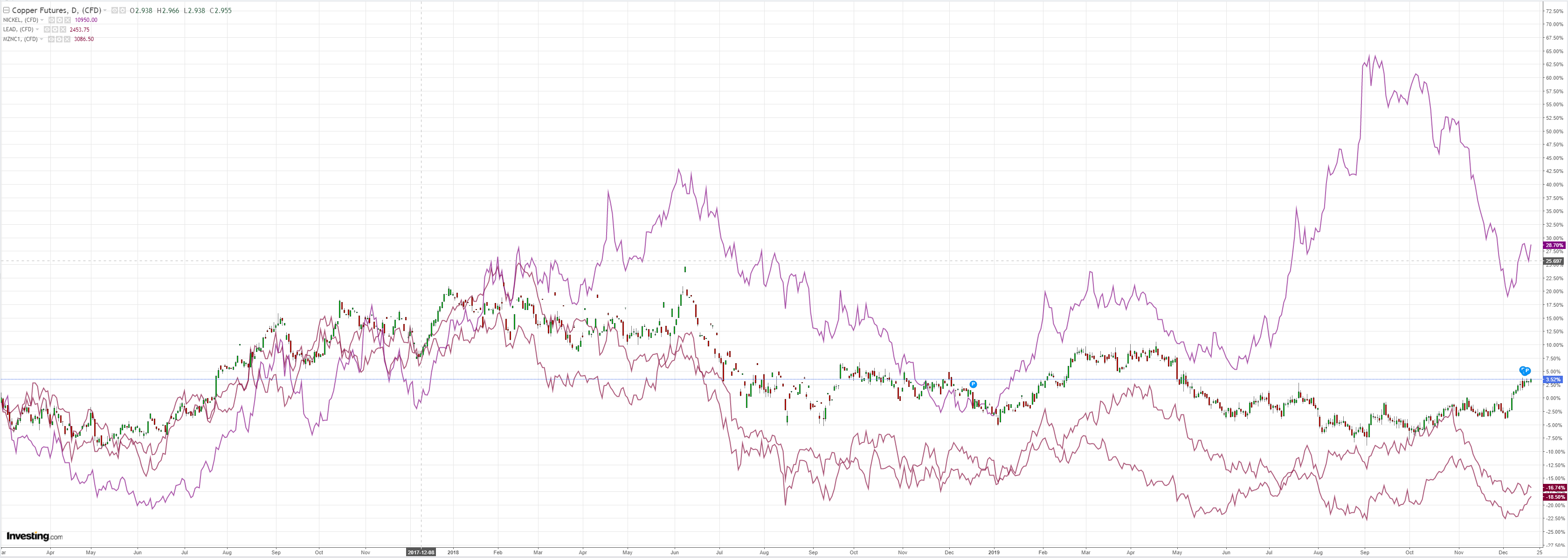

Metals were firm:

Miners stable:

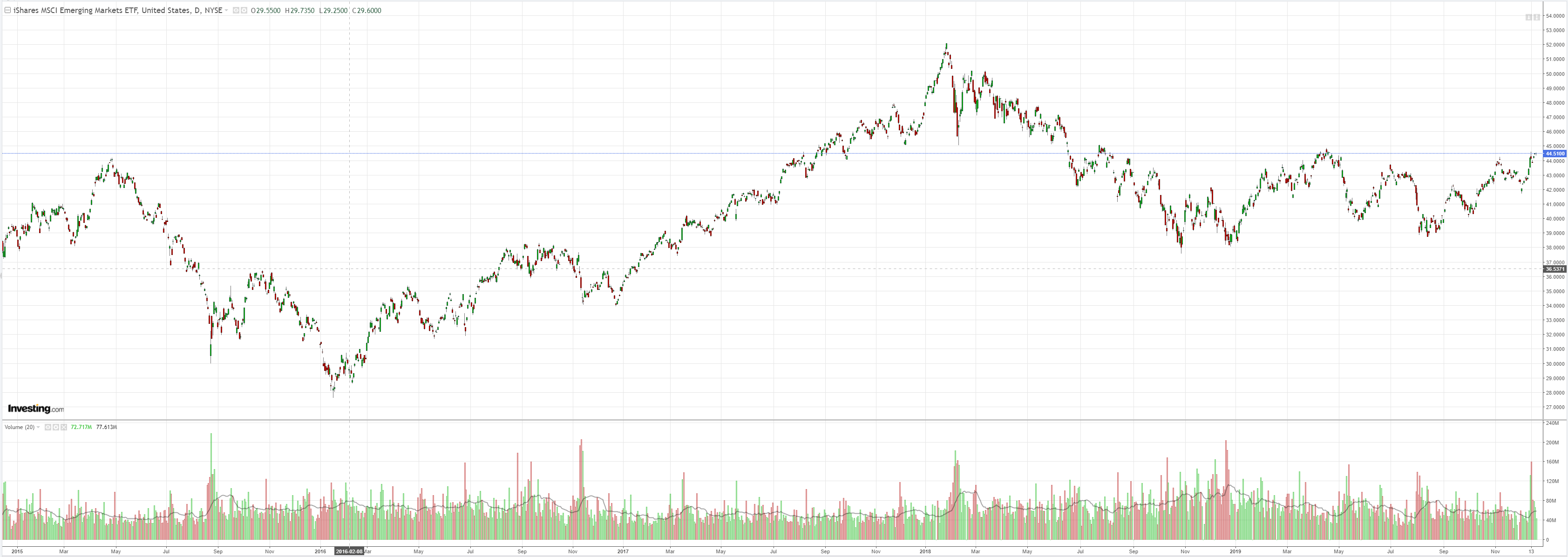

EM stocks too:

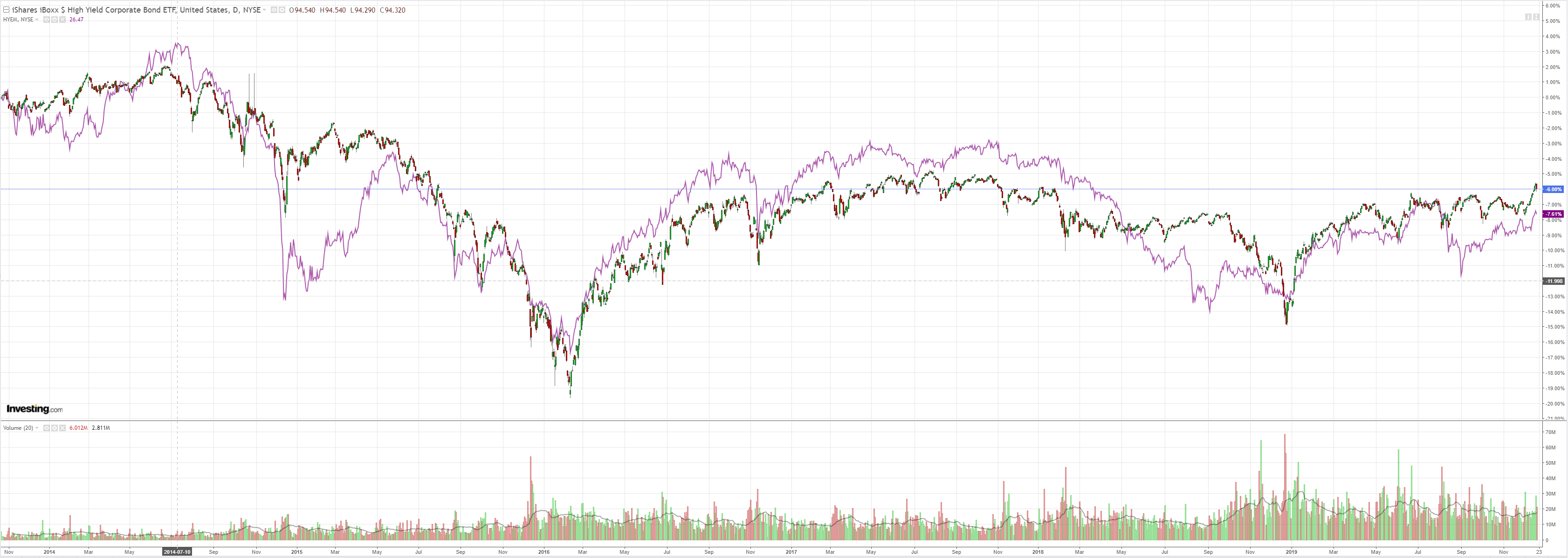

Junk fell:

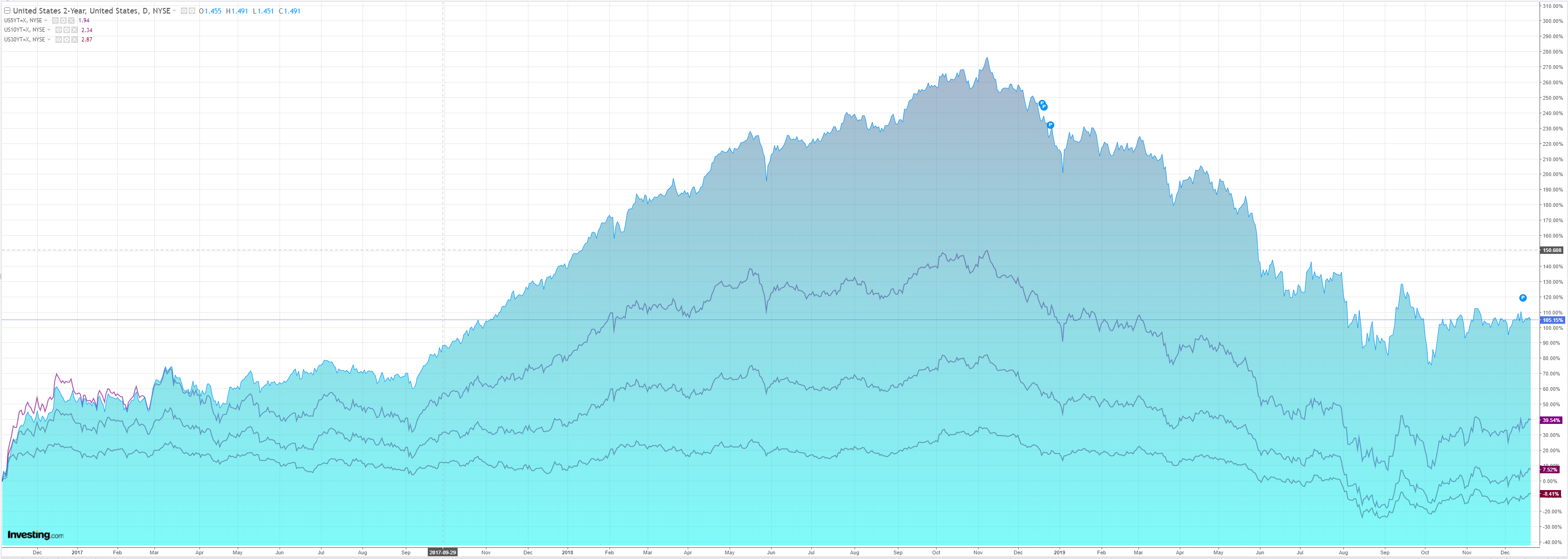

Treasuries were bid:

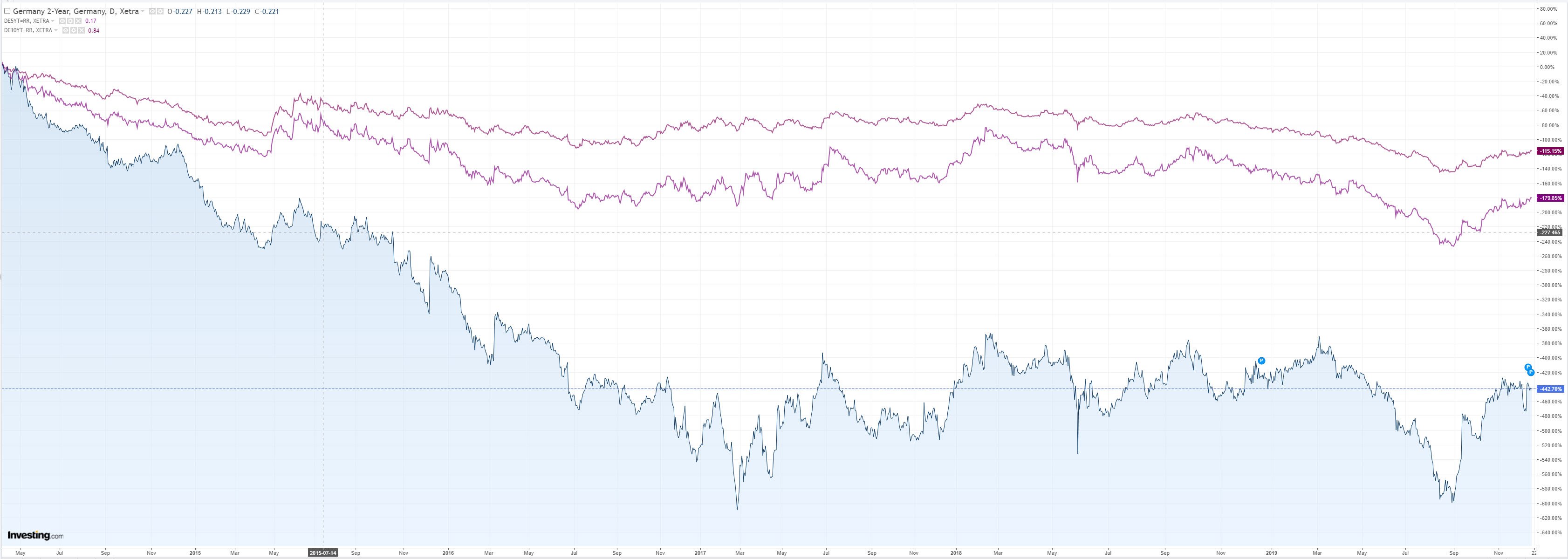

Bunds sold:

Aussie got pole-axed on numberwang:

Stocks are focussed on the moon:

Westpac has the wrap:

Event Wrap

Although the US data was of second and third tier importance, it was consistently disappointing. US jobless claims rose from 1671k to 1722k (vs 1676k expected). The Philadelphia Fed business survey fell from 10.4 to 0.3 (vs 8.0 expected). Existing home sales fell 1.7% in Nov (vs -0.4% expected). Conference Board’s leading index was flat in Nov (vs +0.1% expected).

FOMC member Bullard said in a WSJ interview that rates can remain on hold in 2020, adding the bar for any rate change is high. He said the rate hike in Dec 2018 was a mistake, the steepening in the yield curve is a positive, and firms are learning to cope with the trade uncertainties.

The BoE left the repo rate at 0.75% and QE totals unchanged, as had been widely expected. The vote was 7-2, Saunders and Haskell voting for a 25 bps cut for a second consecutive month. The minutes showed that the committee think time is needed to assess the impact of the general election.

Sweden’s central bank hiked its policy rate (repo rate) from -0.25% to zero and signalled it expects to remain on hold for some time. Inflation has been close to the Riksbank’s target of 2.0% per cent since the start of 2017.

Norway’s central bank, Norges Bank, remained on hold at 1.5%, as was widely expected. The Governor emphasised no tightening is expected over the forecast horizon, in contrast to market interpretation.

Event Outlook

NZ: Consumer confidence (ANZ) survey bottomed in September and sits slightly above the long term average.

Japan: Nov CPI is expected to rise to 0.5%yr from 0.2%yr.

Europe: Dec consumer confidence is anticipated to decline to -7.6 from -7.2.

US: Q3 GDP final is likely to confirm 2.1% annualised growth. Nov personal spending and personal income are both expected to be up 0.3%. PCE annual headline inflation is seen to edge up to 1.4%yr from 1.3%yr while core inflation cools to 1.5%yr from 1.6%yr.

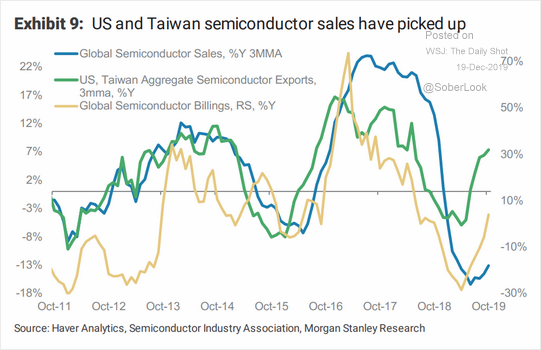

Not much market moving there. A few charts to gauge where the reflation is at. First, the leading indicator of semi-conductor sales:

Some life there but second derivative improvements will not be enough before long. We’ll need growth.

The most hopeful chart on that front is this one on global inventories:

There is some room there for restocking, though a lot less the last two mini-cycle truns in 2013 and 2016. It confirms my view that any bounce in global manufacturing will be moderate at best.

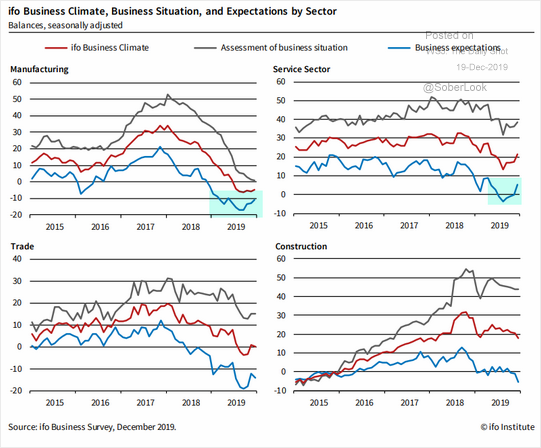

Europe is feeling the hope and not much else:

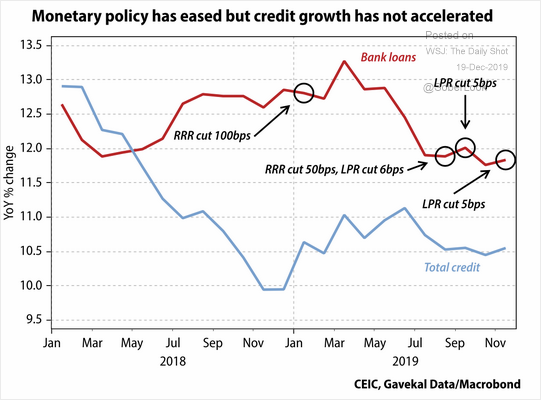

While the big missing ingredient, a Chinese rebound, is still a lock:

ABS jobs numberwang for a day cannot paint over this picture. We’re in for a moderate at best global bounce, held back largely by Chinese slowing, and that will not be good for the AUD next year.