DXY roared back Friday night:

The Australian dollar was universally puked:

CFTC positioning was unchanged but the data concludes Wednesday so the late week fireworks will appear next week:

Gold is threatening to bottom:

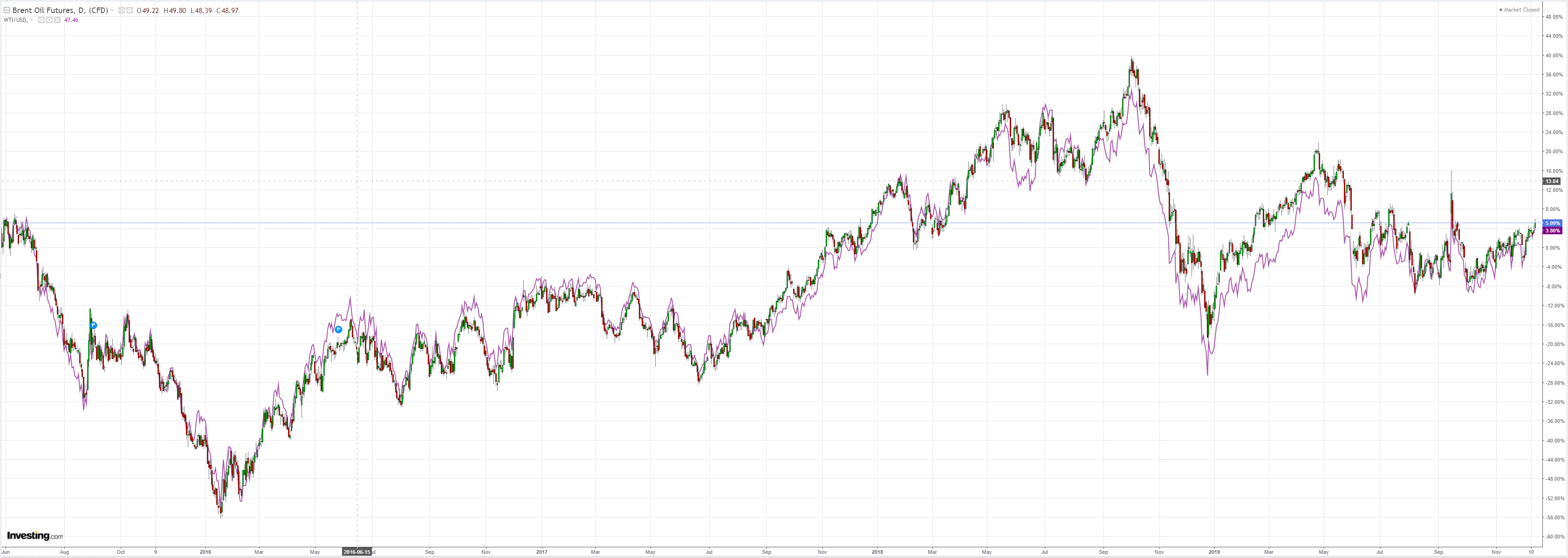

Oil is marching on:

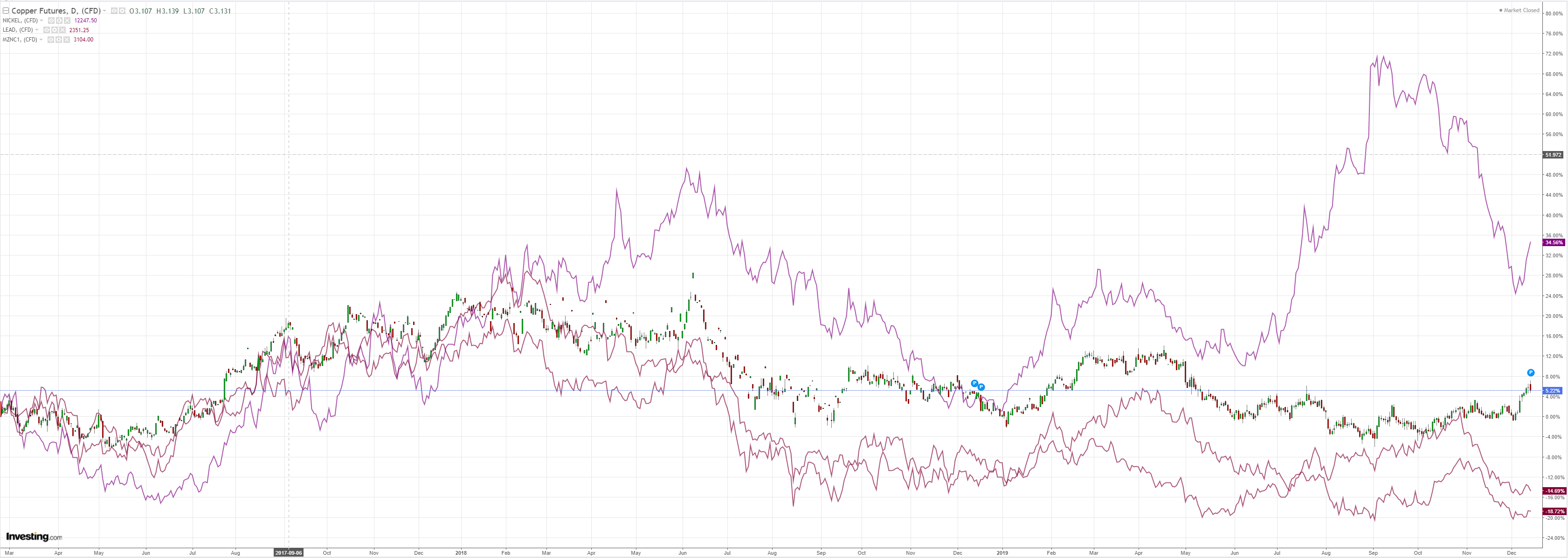

Metals meh:

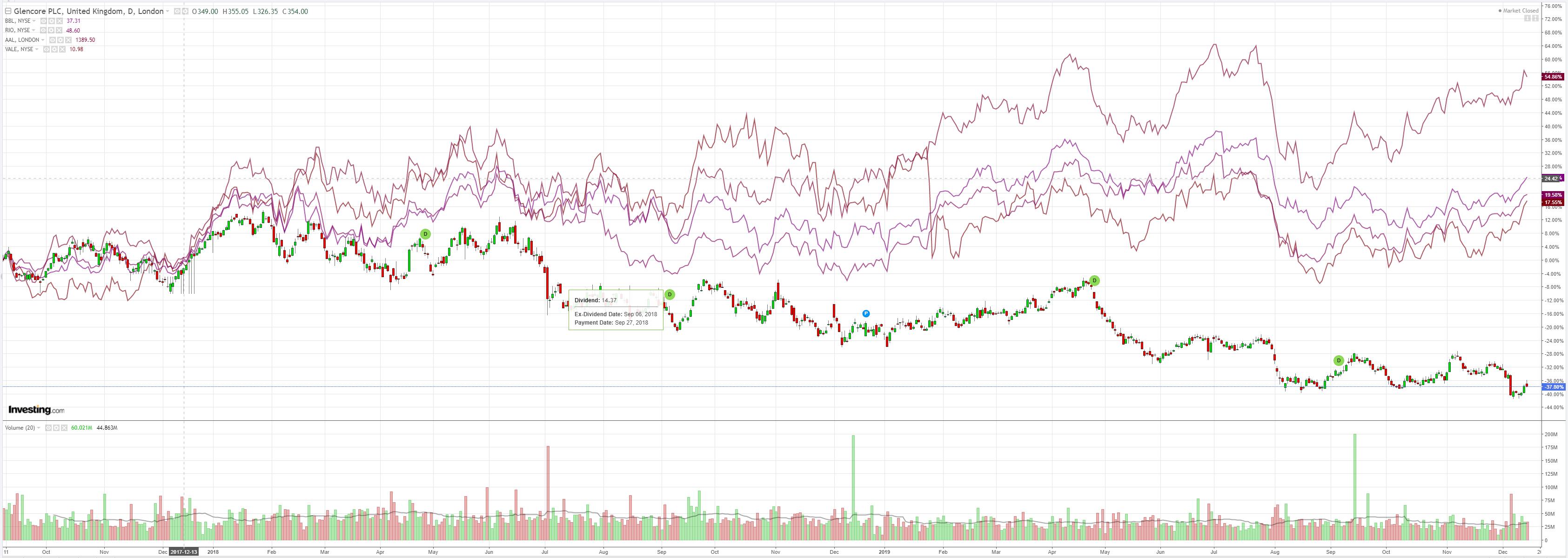

Miners to the moon still:

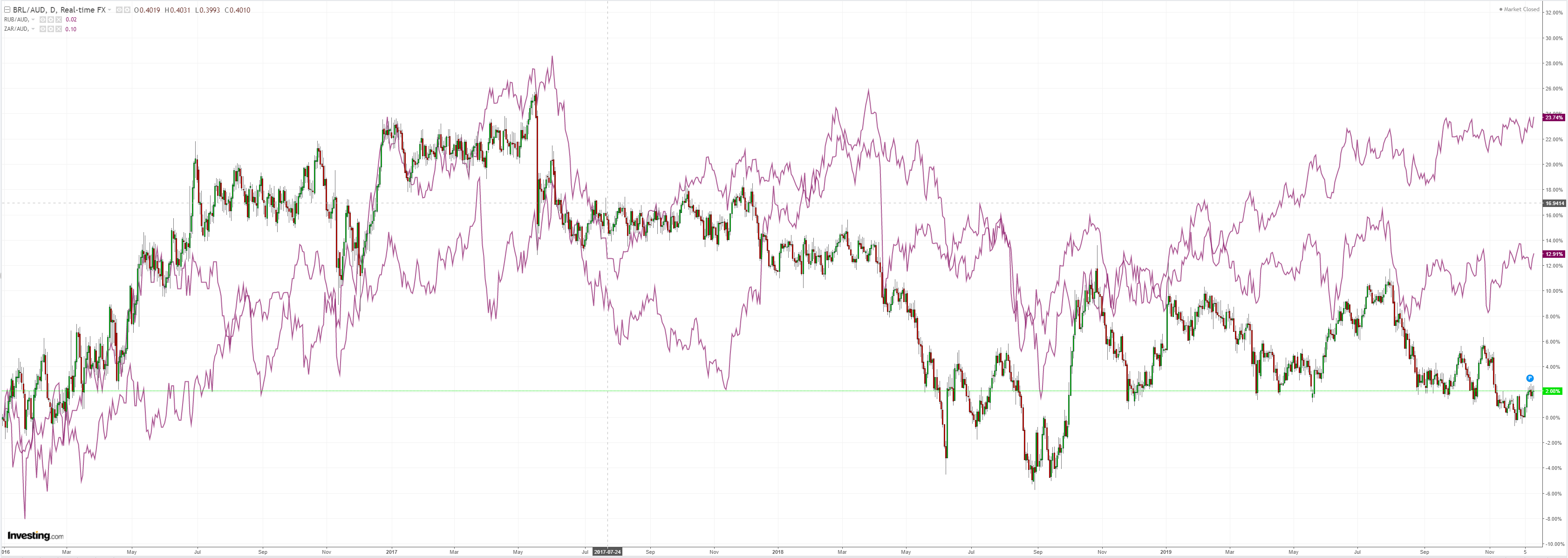

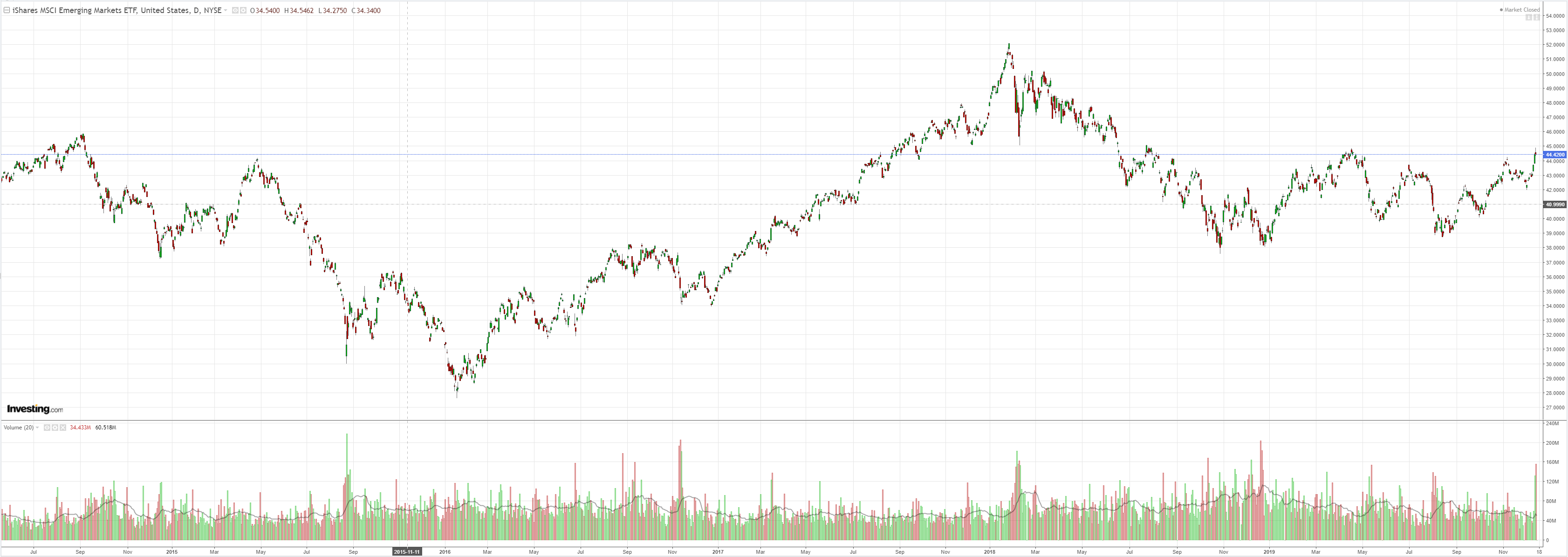

EM stocks flamed out:

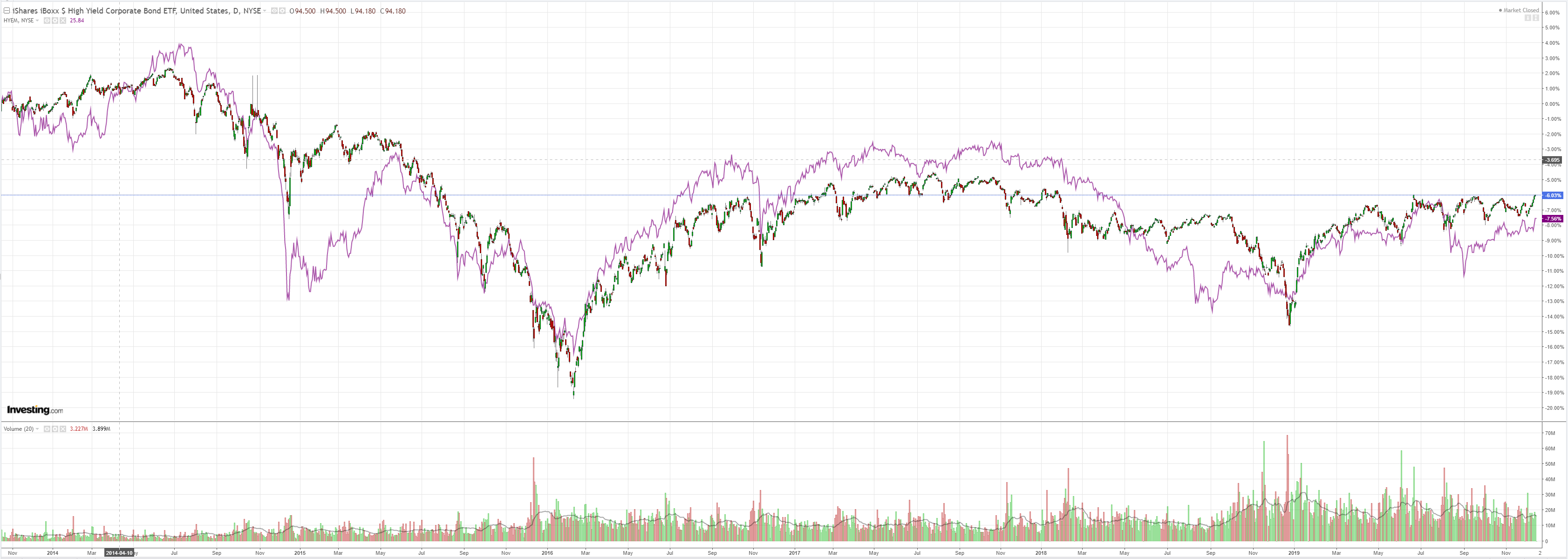

Junk was firm:

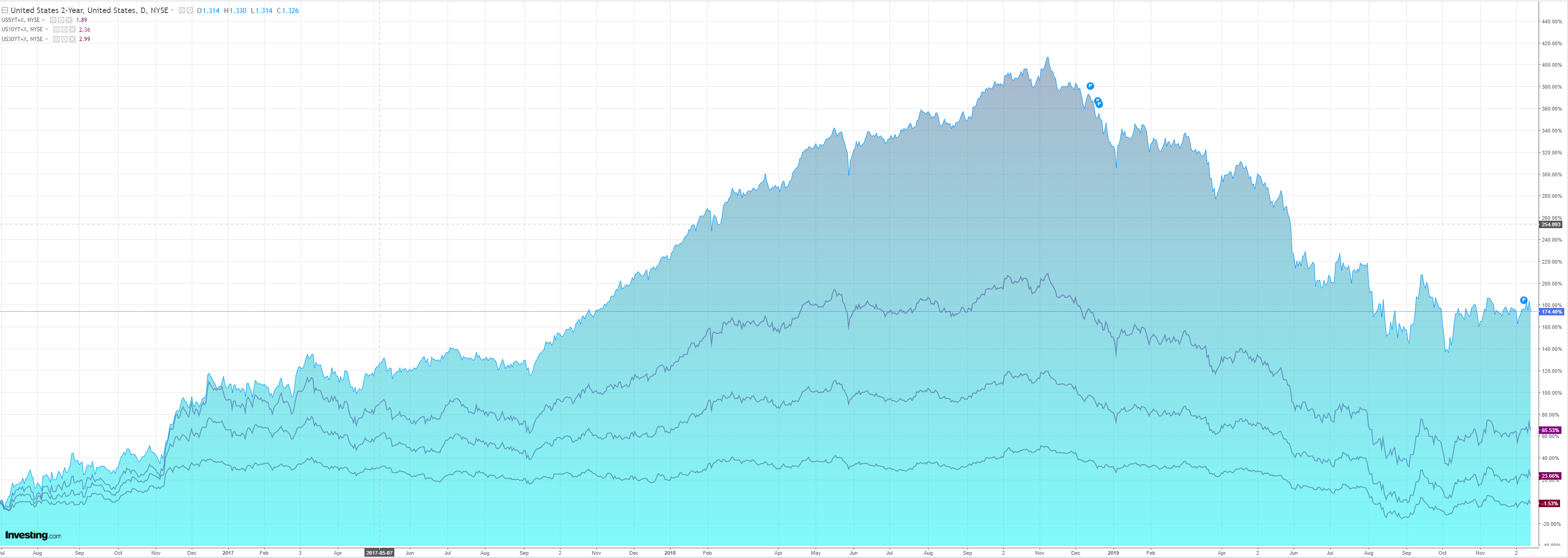

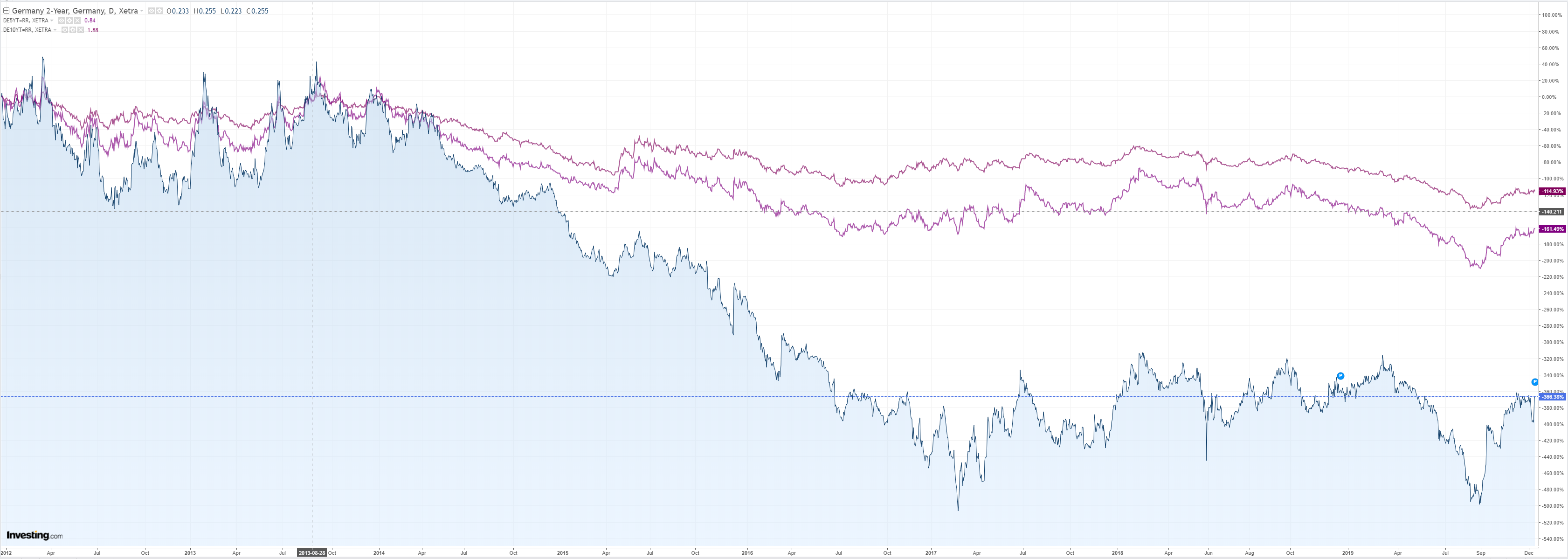

Bonds were bid bigly:

Stocks hardly budged:

Try to make sense of this, at the FT:

The agreement, which was confirmed by officials in both Washington and Beijing on Friday, commits China to buying at least $40bn of US agricultural goods annually, tightens protection for US intellectual property and bans the forced transfer of technology from US companies.

It also contains commitments on the Chinese side against competitive devaluations of its currency and measures to improve access to its market for US financial services groups. However, China did not make concessions on some of the biggest sources of strain in the bilateral relationship, such as its use of industrial subsidies and state-owned enterprises, as well as cybertheft, leaving those thorny issues to a later stage.

In exchange for those concessions, the US agreed not to proceed with a new escalation in levies on $156bn of Chinese consumer goods planned for Sunday, and it will cut tariffs on $120bn of Chinese imports that were introduced in September to 7.5 per cent from 15 per cent. Washington is still maintaining 25 per cent tariffs on about half of all Chinese imports, worth about $250bn, which were introduced since the trade war began between the world’s two largest economies in March 2018.

The agreement still needs to be legally vetted and translated. It is expected to be signed in early January and take effect a month later.

Versus WSJ:

Chinese negotiators struck a more cautious tone. At a hastily arranged press conference…Vice Commerce Minister Wang Shouwen, one of China’s lead negotiators, said the U.S. had agreed to remove the remaining tariffs on Chinese products “in stages.” Mr. Lighthizer said there was no such agreement on that, and suggested China believes further reductions could be negotiated in later phases of the deal.

…the Chinese negotiators, led by Mr. Liu, President Xi Jinping’s point man on U.S. trade, balked at guaranteeing the purchases for fear that such managed trade could violate the rules of the World Trade Organization and cause friction between China andits other trading partners.

…“China has yet to confirm this pledge or provide any details on how they will meet it,” said Brian Kuehl co-executive director of Farmers for Free Trade, which backs removing tariffs and opening markets. “There are rightfully many doubts about the president’s claim that China will purchase $50 billion in ag products in a single year—more than twice the level of pre-trade war annual purchases.”

At Friday’s briefing, Ning Jizhe, a top deputy of the National Development and Reform Commission, hewed to the position Beijing has maintained throughout the negotiations: “Expanding trade cooperation must be based on market principles and WTO rules.”

That emphasis raised questions about whether China committed to any big purchases of U.S. products at all…

Larry Kudlow alos appeared at CNBC and declared that the ag purchese were over two years. Not even the administration appears to know what has been agreed.

Lingering doubts are normal but these are gaping holes and there is no way to close them because the agreement itself is being kept secret. It all reads like El Trumpo sat down in front the mirror and agreed with himself how he would capitulate, then signed that agreement with himself, and everyone else is just an observor in the charade. There’s no definition, no benchmarks and no enforcement.

As such, El Trumpo has now negotiated himself into such a corner that Beijing can decide at its leisure whether it wants him re-elected (buy ag big) or a Democrat (buy none at all).

If this it the linchpin in a 2020 global recovery then good luck! Global growth has been slowing on multiple fronts in 2019:

- trade volumes have fallen materially;

- business investment has slumped amid geopolitcal tensions;

- a global car sales shock has transpired, led by China;

- a universal oil and commodities glut has prevented new projects;

- a post tax cut US economy has slowed;

- China is dis-leveraging and being rocked by a vehement Hong Kong rebellion;

- Europe has been held back by Brexit uncertainty and its externally led economy.

The trade deal and UK Brexit vote lifts a little of the geopolitcal fog but not enough to really matter.

The key problem is that the US/China trade deal does nothing to dispel Cold War 2.0 fears. The deal is thin, confused and opaque. The US and China remain very much at each other’s throats on trade and technology and, most pointedly, in Hong Kong.

Chinese supply chains will remain under pressure so long as Hong Kong freedoms are in jeopardy and the threat of more tarrifs remains. Any risk assessment for new investment will either repatriate capital or send it into alternative emerging markets to China, which will contonue to de-globalise.

This means minimal respite for China’s external sector in 2020, a US economy that will continue to lead global growth at a moderate pace, and only a modest rebound for Europe as Brexit negotiations resume.

That is not to say that the market can’t run for a while on hopes for better. With phase two trade non-deal negotiations beginning soon there’s now a platform for the jawboning of equities through to the US election, which is what this is really all about.

In sum, I can’t see anything beyond a modest global bounce out of this, and therefore continued US economic outperformance. That means a USD that refuses to fall and reflate the global economy more widely.

It’s impossible to know when the market will shift from voting to weighing machine again but the Australian dollar rally is running on fumes regardless.

David Llewellyn-Smith is Chief Strategist at the MB fund and MB Super which is overweight international shares that will benefit from a falling Australian dollar.