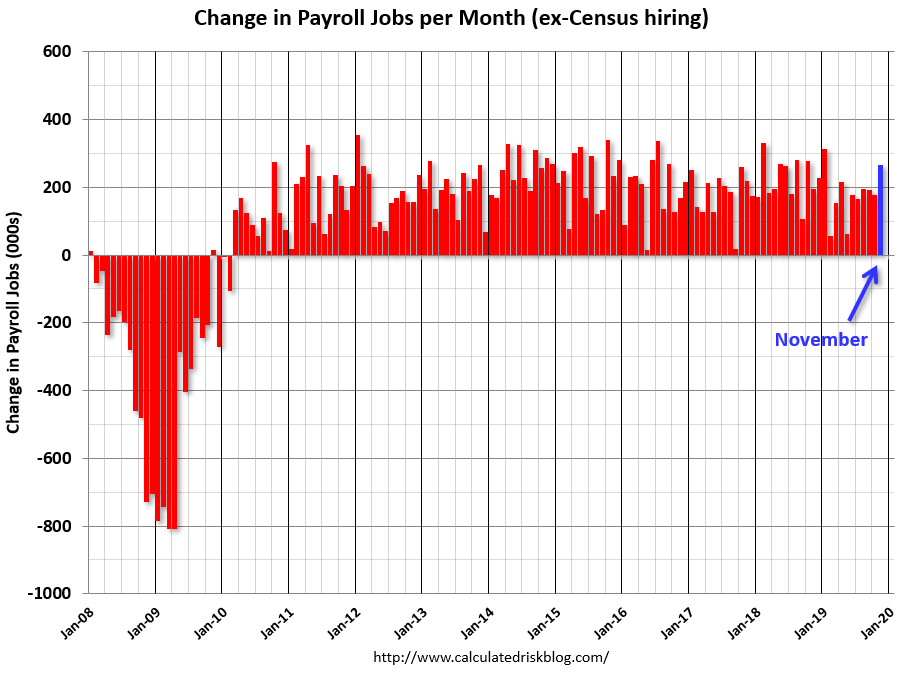

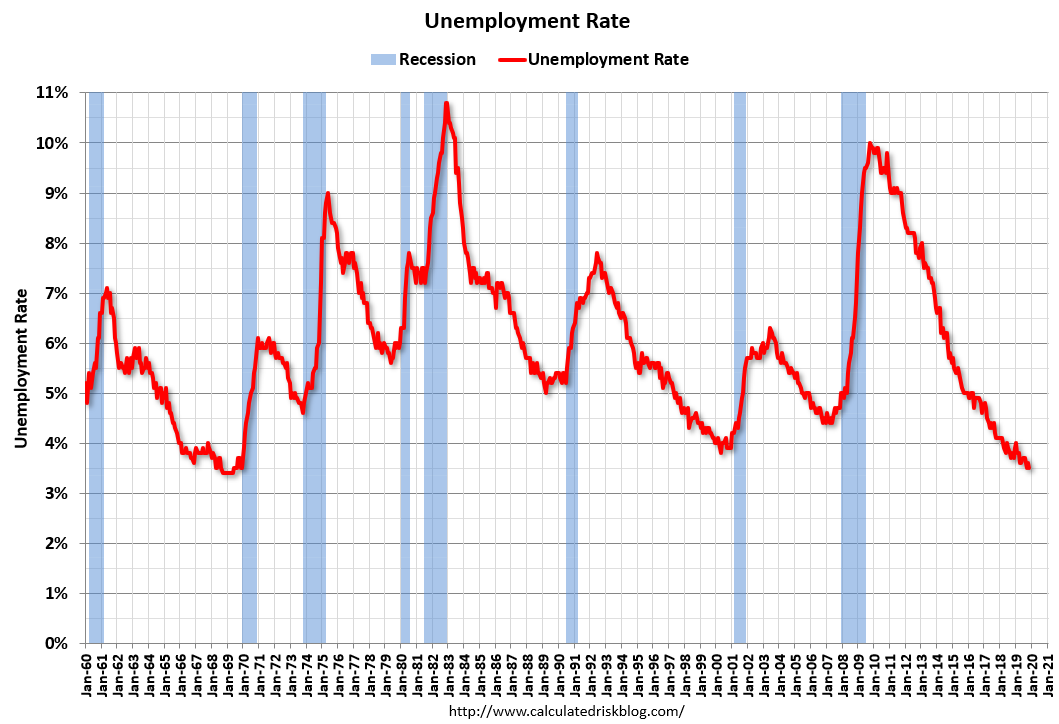

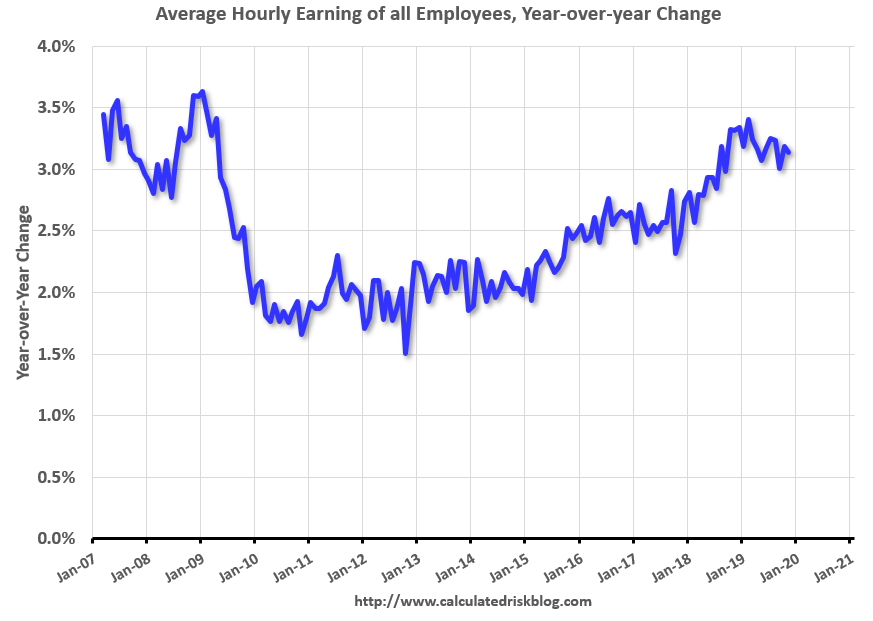

US non-farm payrolls rose 266k in November, easily beating the 180k median expectation, with October revised by +28k. The unemployment rate fell from 3.6% to 3.5%, underemployment fell from 7.0% to 6.9%, participation fell from 63.3% to 63.2% but retained an upward trend, and hourly earnings rose 0.2% (3.1% yoy).

Consumer sentiment (University of Michigan survey) also beat expectations, rising from 96.8 to 99.2 (vs 97.0 expected) – the highest since May. Both current conditions and future expectations components rose. Inflation expectations 5-10yr ahead fell from 2.5% to 2.3%.

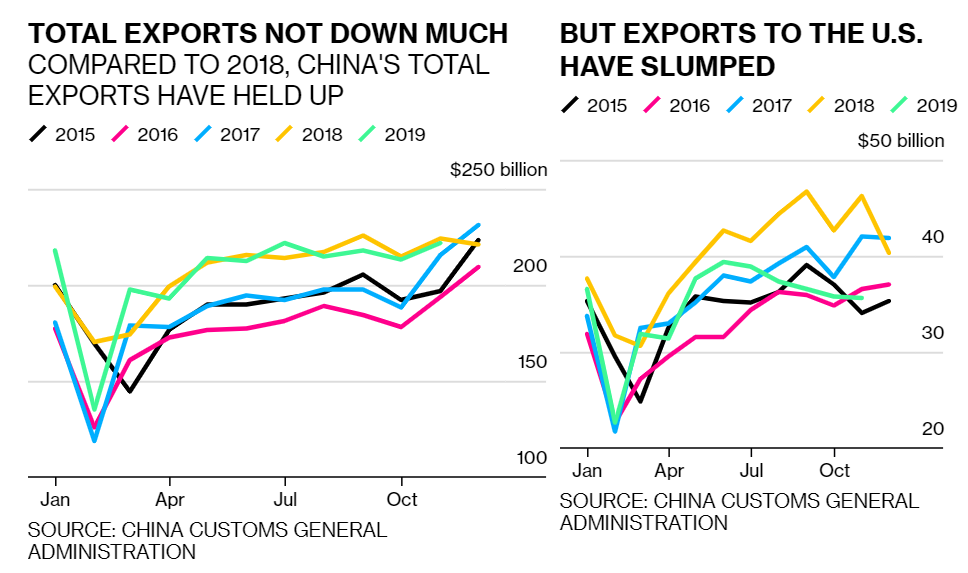

China’s November trade balance disappointed at CNY274bn (vs CNY300bn expected). Exports rose 1.3% (vs +1.9% expected) and imports rose 2.5% (vs 0.9% expected)

On the US-China trade talks, White House adviser Kudlow said in a CNBC interview that December 15 is an important date. He suggested a deal might be a little closer than where it was when he was last interviewed, characterizing the talks as “intense” and that the decision is totally up to the president. He warned that if the US does not get the necessary assurances, it will not go forward.

Event Outlook

NZ: Q3 manufacturing activity is released, and will help refine Q3 GDP estimates.

Japan: Q3 GDP final is expected to be revised up to +0.2% from +0.1%.

Europe: Dec Sentix Investor Confidence was last at -4.5, a still downbeat level despite the bounce in Nov.

Total nonfarm payroll employment rose by 266,000 in November, and the unemployment rate was little changed at 3.5 percent, the U.S. Bureau of Labor Statistics reported today. Notable job gains occurred in health care and in professional and technical services. Employment rose in manufacturing, reflecting the return of workers from a strike.

…The change in total nonfarm payroll employment for September was revised up by 13,000 from +180,000 to +193,000, and the change for October was revised up by 28,000 from +128,000 to +156,000. With these revisions, employment gains in September and October combined were 41,000 more than previously reported.

…In November, average hourly earnings for all employees on private nonfarm payrolls rose by 7 cents to $28.29. Over the last 12 months, average hourly earnings have increased by 3.1 percent.

Advertisement

Things have softened but not materially and not enough to upset the US consumer who is a beast aand don’t you forget it!

The problem is, it is not fanning out into China. Weekend export data gave us the tale of the tape with exports still down 1.1% annually as US shipments crater:

Advertisement

In turn, that limits the spillovers to Europe which is already being eaten by China as it seeks to diversify its US trade risk. So any global rebound is stillborn so long as tarrifs remain in place. For that matter, so long as corporations are forced to decouple the US and China via shunted suply chains via fair means and foul.

This caps any involvement of the Australian dollar in another late cycle mini-bump to global growth.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.