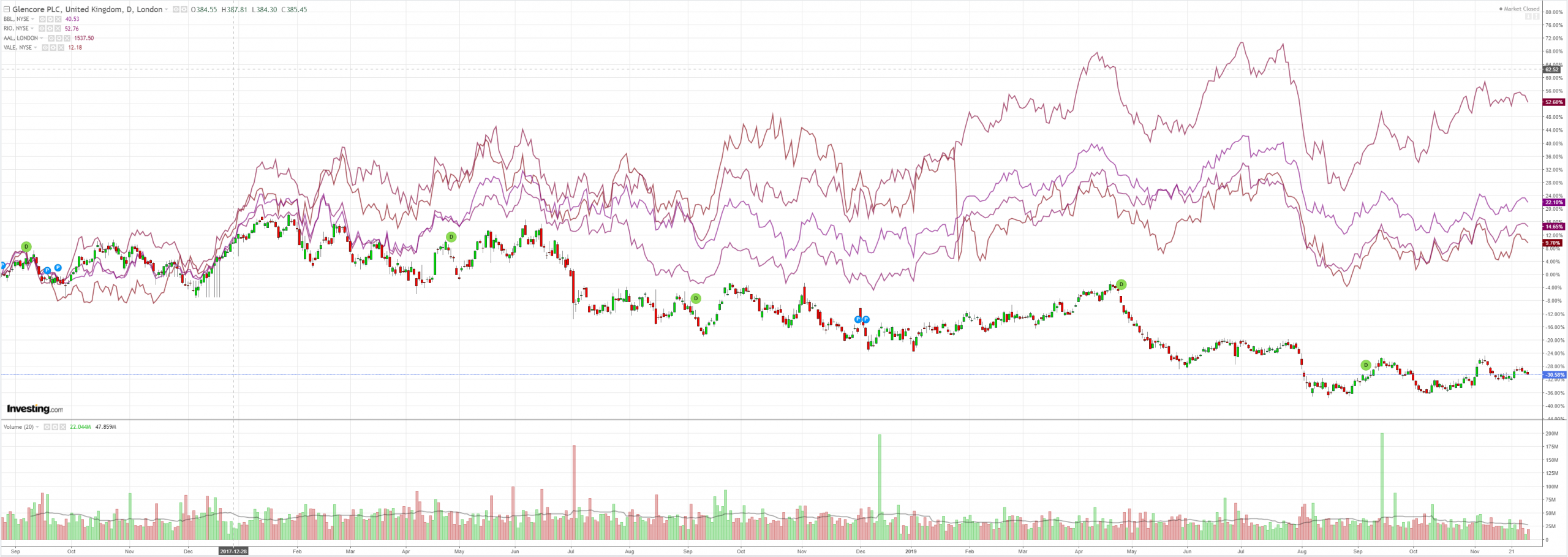

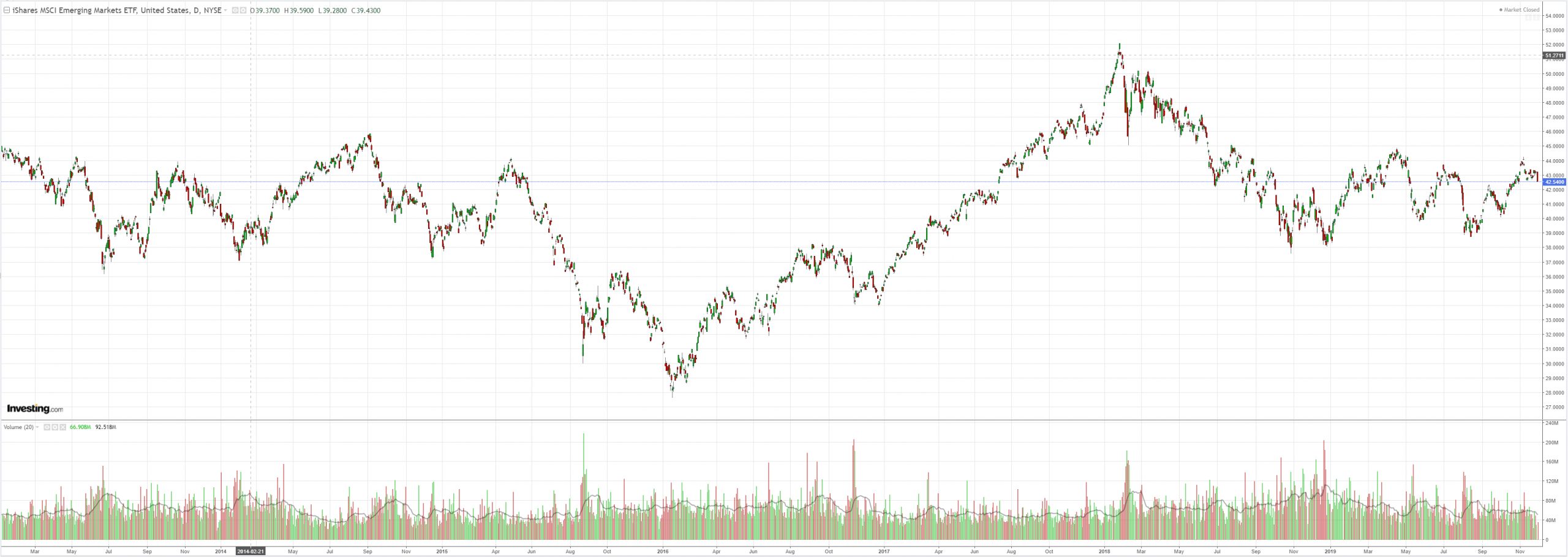

EM stocks were hammered by oil. A lot of thjese ETFs are little else:

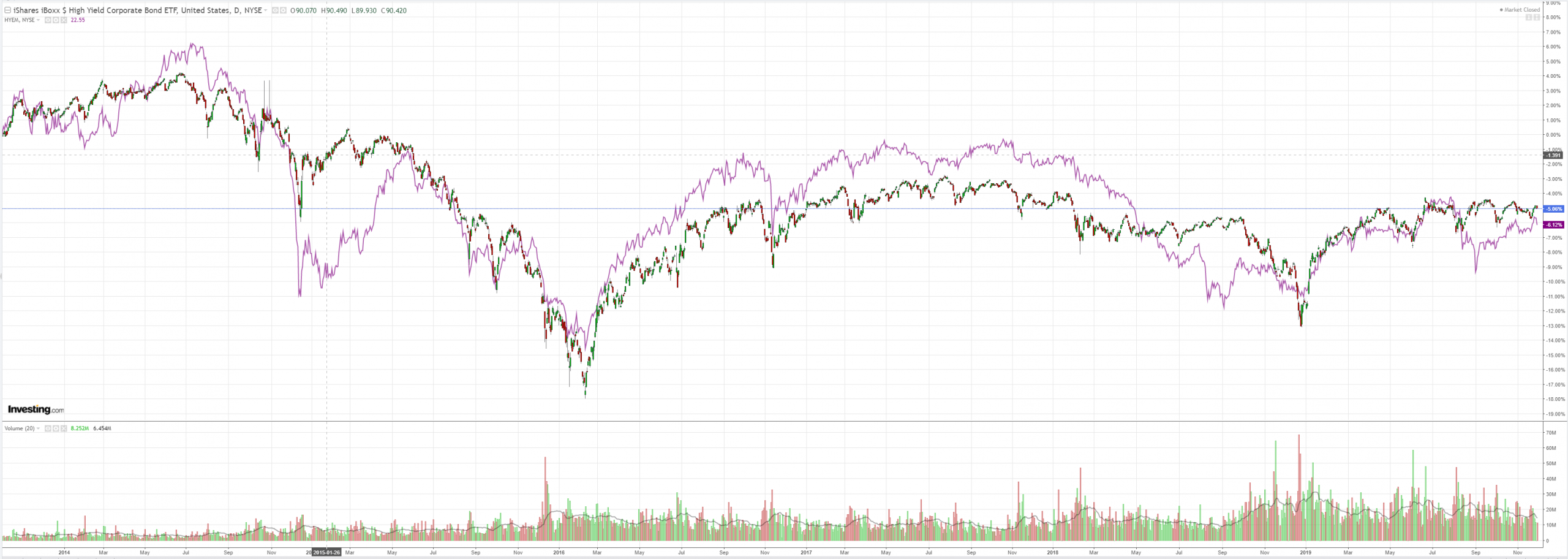

Junk too:

Advertisement

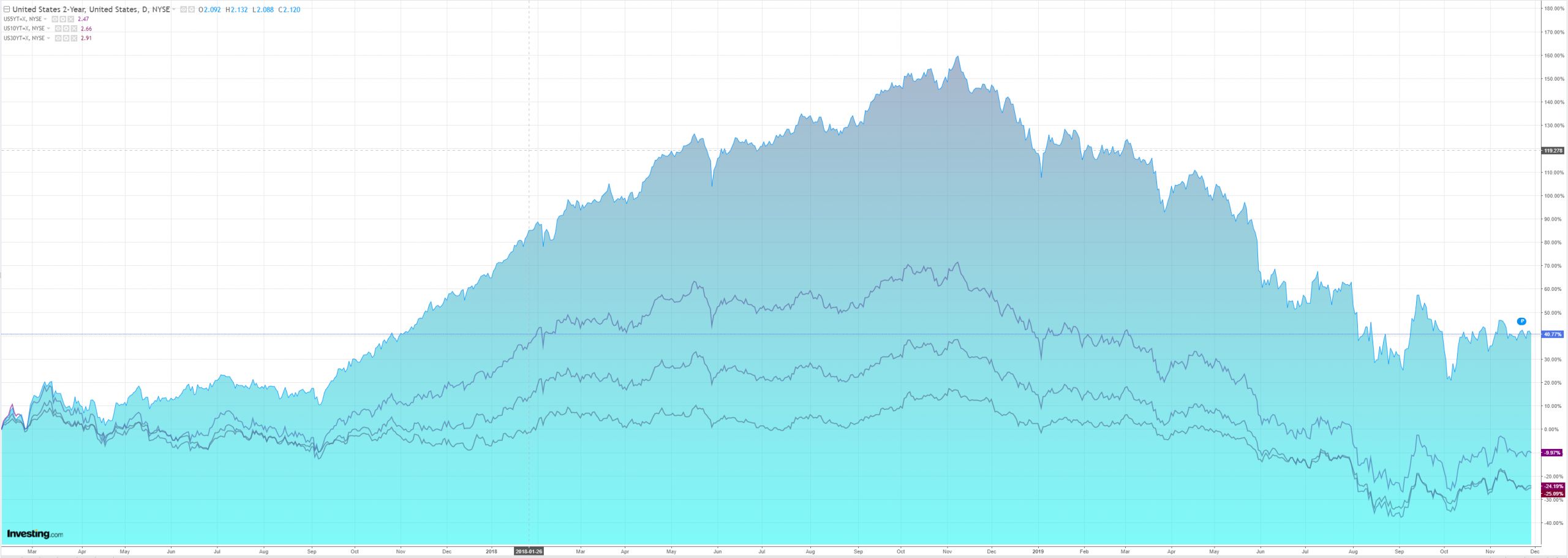

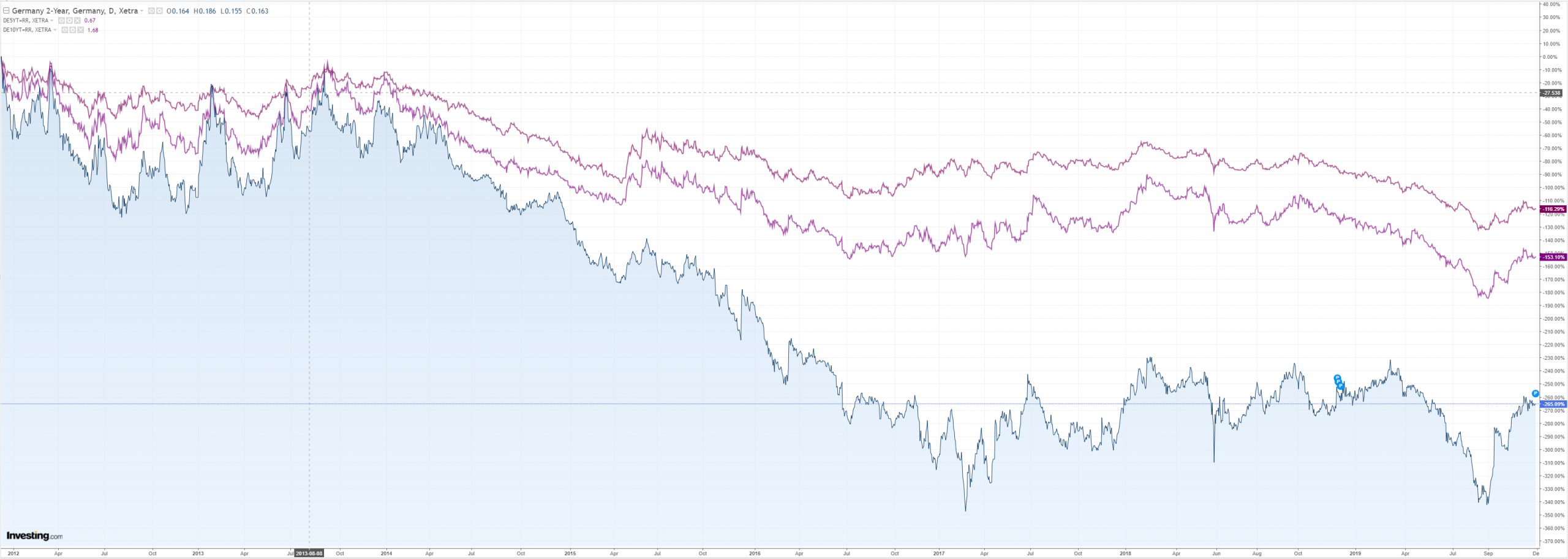

Bonds were mixed:

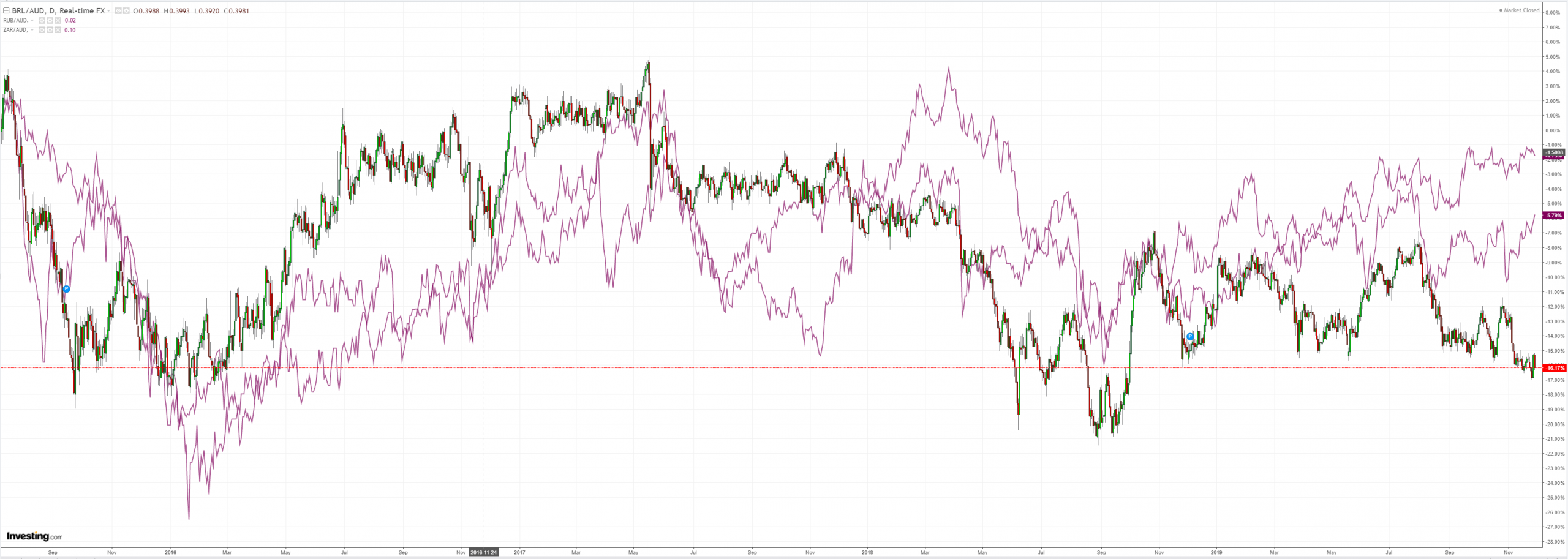

As Aussie sold off:

As stock pulled back, barely:

Advertisement

Westpac has the data wrap:

Event Wrap

Eurozone Nov. CPI inflation was slightly above estimates. Headline CPI declined 0.3%m/m (est. -0.4%m/m) for an annual pace of +1.0%y/y (est. +0.9%y/y) and core CPI rose to +1.3%y/y (est. +1.2%y/y). Oct. unemployment was in line with estimates at 7.5%, though Sep was revised up to 7.6% from 7.5%.

Canadian 3Q GDP of +1.3% annualised was in line with estimates, showing a sharp pullback from 2Q +3.5% annualised (revised down from +3.7%). A sharp slide in net exports and draw downs in inventories led the pullback, but there were solid gains in domestic demand and capex.

China manufacturing PMI at 50.2 beat expectations of 49.5 and the previous reading of 49.3, the data released on Saturday.

Event Outlook

NZ: Terms of trade are estimated to have risen 1.0% in Q3.

Australia: Q3 business indicators survey provides partials for Wednesday’s GDP release. Company profits are expected to rise 1.0% (Westpac fcs: -0.5%) while inventories decrease 0.2% (Westpac fcs: -0.5%, which would add 0.2ppts to GDP given that the rate of decline has moderated from Q2). Oct dwelling approvals are anticipated to decline 1.0%, -18.0%yr (Westpac fcs -2.0% in the month). Nov CoreLogic home value index is expected by Westpac to be up 1.8% based on movements in the daily index with Sydney posting a 2.7% gain.

Europe: ECB President Lagarde testifies to European Parliament.

US: Nov ISM manufacturing index is expected to rise to 49.5 from 48.3, in line with the movement in the Markit PMI measure, albeit significantly lower than its respective level of 52.2 (flash). Oct construction spending is seen to rise 0.4% after a 0.5% increase in Sep.

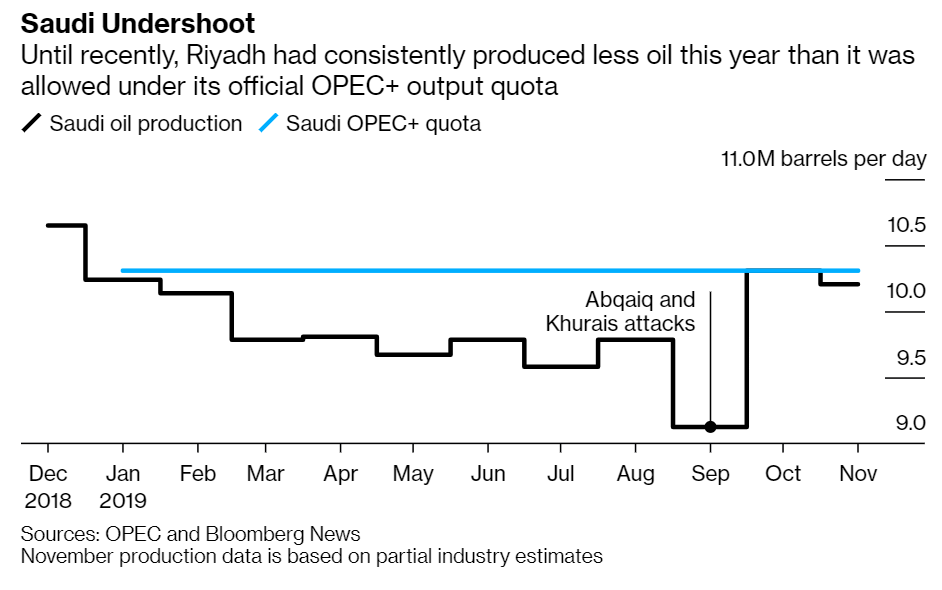

Prince Abdulaziz bin Salman, who took over from Khalid Al-Falih in September, will likely use his first OPEC meeting as Saudi oil minister next week to signal OPEC’s dominant producer is no longer willing to compensate for other members’ non-compliance, according to people familiar with the kingdom’s thinking. OPEC meets in Vienna on Dec. 5, followed by the larger OPEC+ alliance, which includes Russia, the next day.

…The cheating has been widespread. Iraq, for example, should be pumping no more than 4.51 million barrels a day; but in some months it produced nearly 4.8 million barrels a day. Kazakhstan accepted a limit of 1.86 million barrels a day, however, it has produced closer to 1.95 million barrels. Nigeria agreed a quota of 1.68 million barrels a day, but has regularly pumped more than 1.8 million barrels a day.

Russia has pumped more oil than allowed by the OPEC+ deal in eight months this year. It has complied with the agreement in only three months of this year — May, June and July — when disruption to the key Druzhba oil pipeline pushed production below its OPEC+ target.

Advertisement

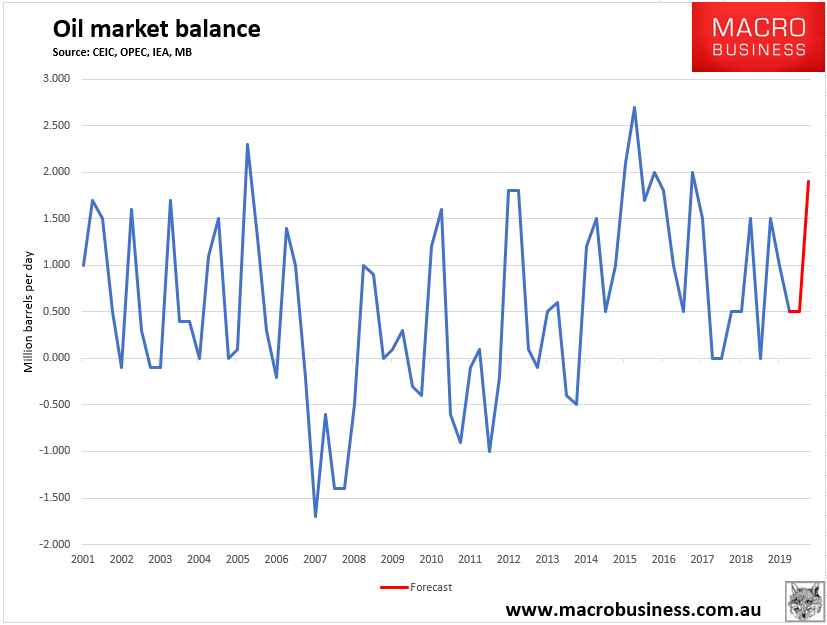

I still see a material glut ahead:

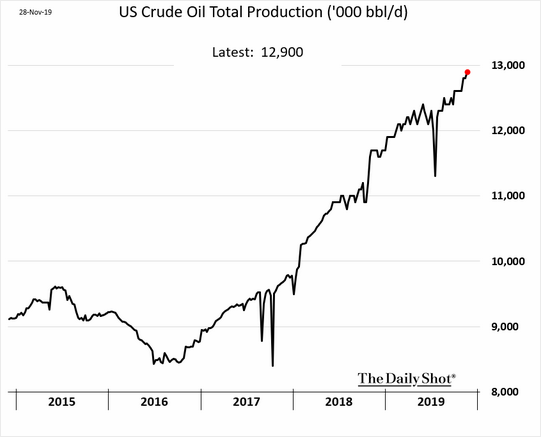

With no end to US supply:

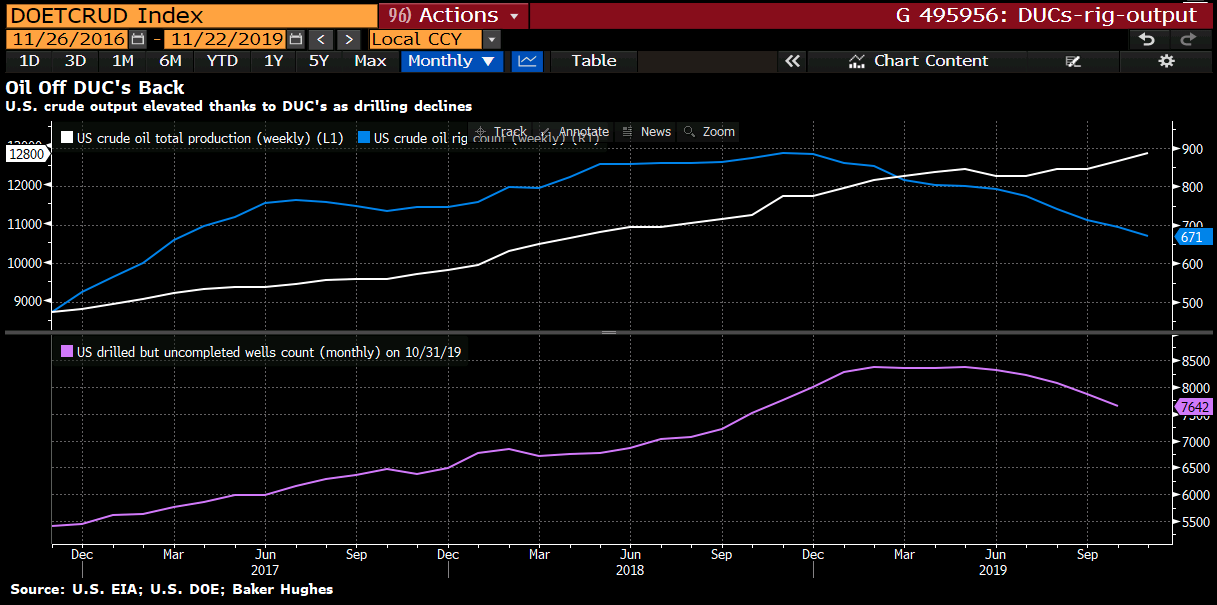

As the falling rig count is managed via the DUC rundown:

Advertisement

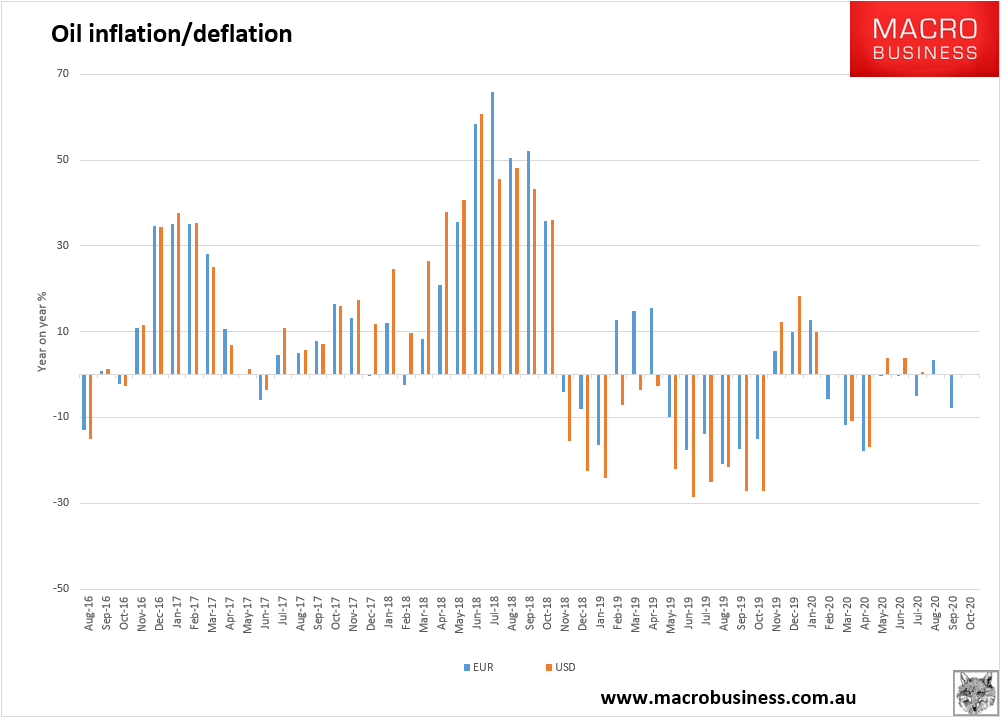

Which won’t help global inflation:

Or the Australian dollar:

Advertisement

At a certain point we would have needed higher oil to reboot US shale and its DUC inventory but not if OPEC+ is going to give up on managing the market.

We might get a little pop in the AUD today following better China PMIs but where oil goes the Australian dollar typically follows.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.