DXY was up and away last night:

The Australian dollar was buoyed against DMs:

Not so much EMs:

Gold is hanging on:

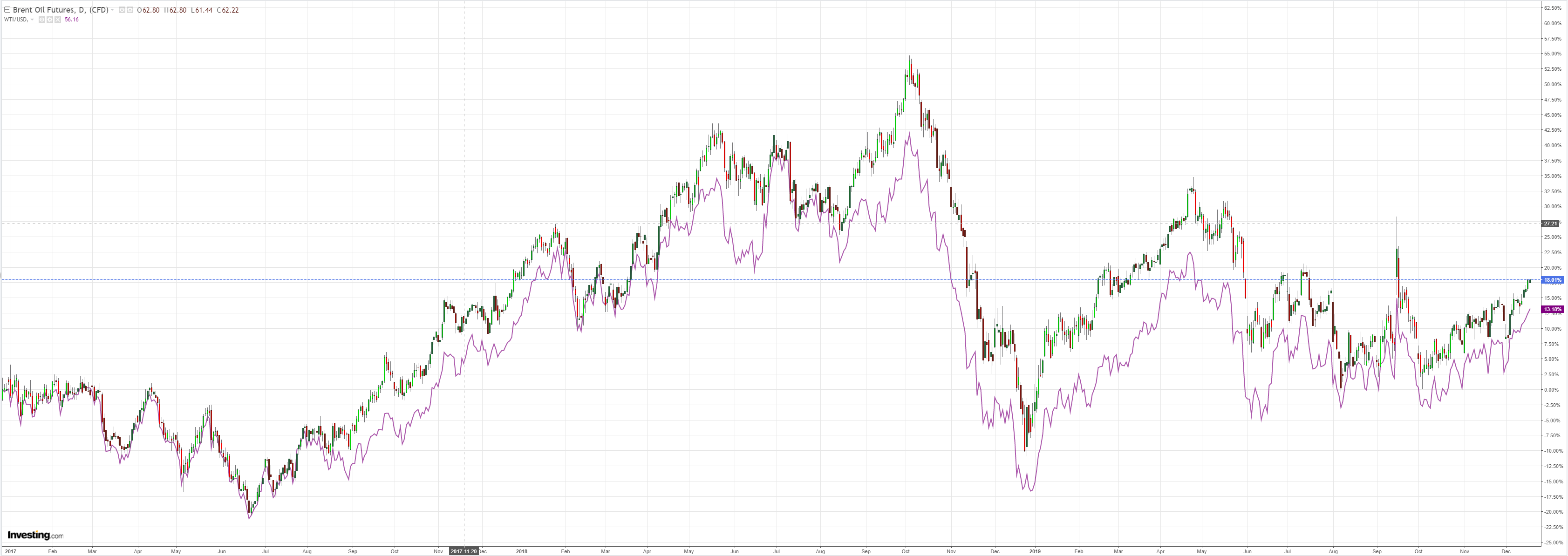

Oil is taking off on reflation hopes, shale to follow if this keeps up:

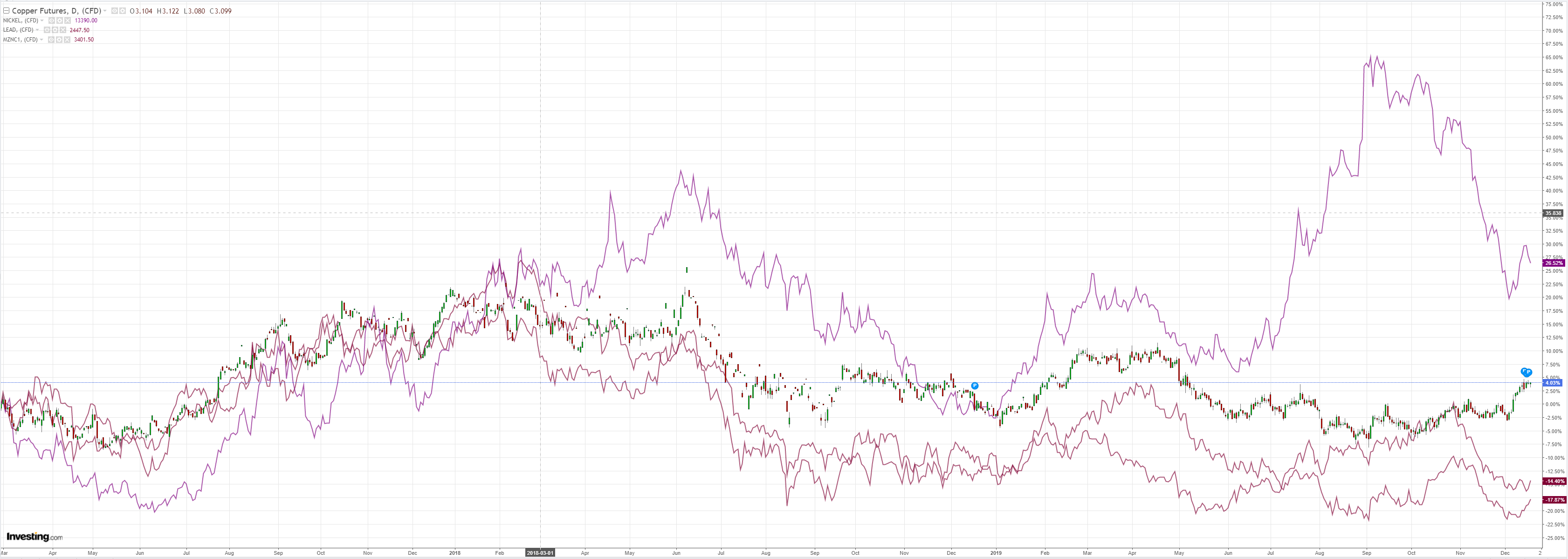

Metals did better but are still weak:

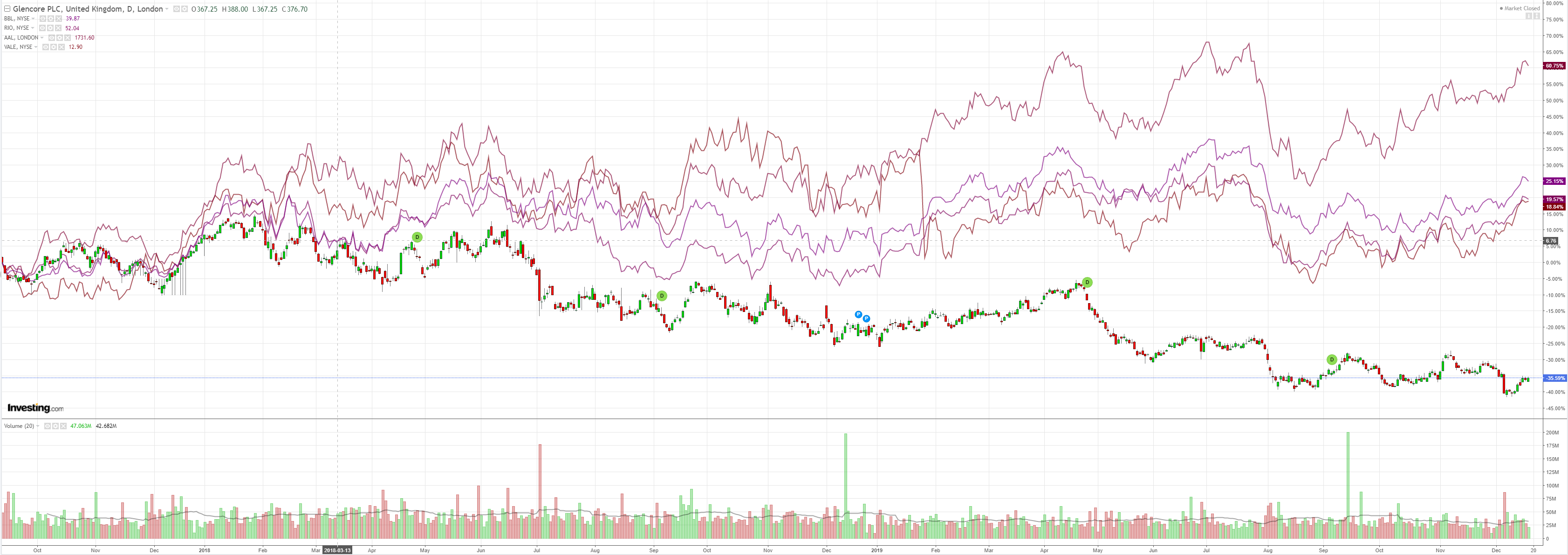

Miners fell:

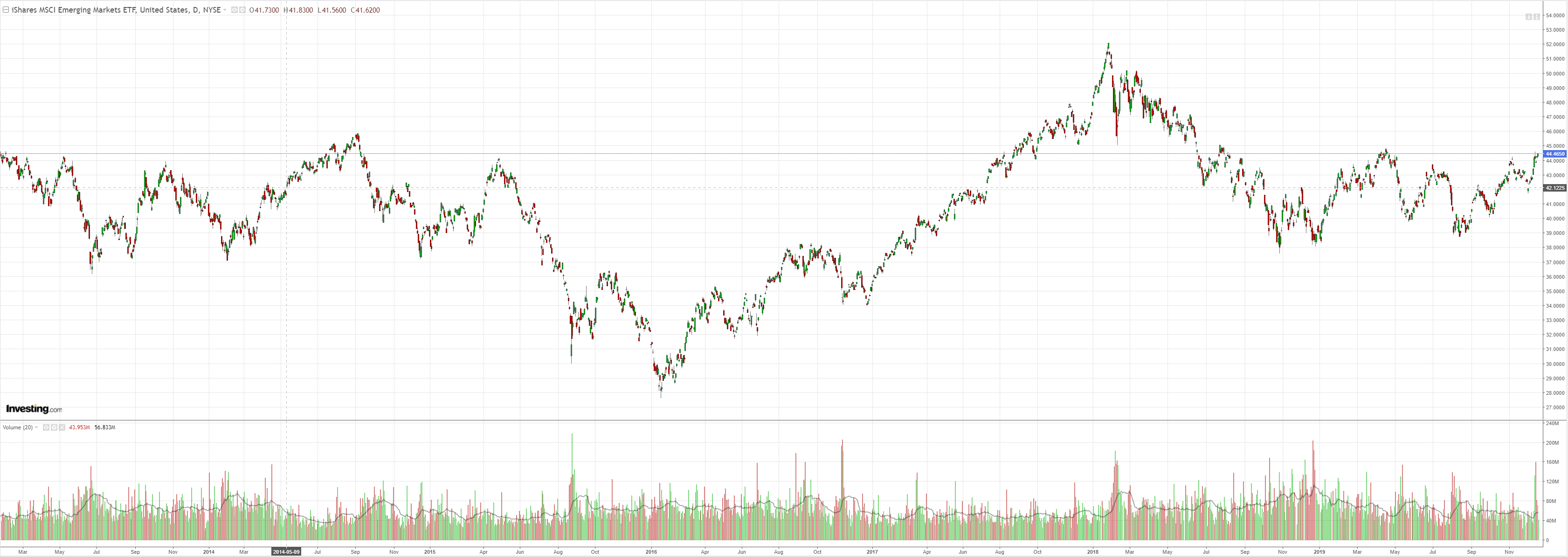

EM stocks lifted:

Junk is cheering oil reflation:

Bonds were all sold as oil adds inflation hope:

Stocks are still edging up:

Westpac has the wrap:

Event Wrap

US lawmakers started debate on whether to impeach US Pres. Trump, a vote expected by noon Sydney time.

Eurozone HICP inflation was confirmed at 1.0% yoy in the final reading for November, in line with expectations. Core inflation was slightly higher at 1.3% but remains well below the ECB’s target. Germany’s IFO business sentiment survey rose from 95.0 to 96.3 (vs 95.5 expected).

Event Outlook

NZ: Q3 GDP is estimated to have risen 0.5%, for a 2.3% annual pace. The pace of growth slowed in 2019, but recent data suggests Q3 should be the low point. Nov trade data is also released.

Australia: Nov employment is expected to be up 15k (Westpac fcs +8k) and see the unemployment rate hold at 5.3%.

Japan: the BOJ policy decision is expected to be unchanged. The Bank will likely reiterate its easing bias and new forward guidance that they expect “short- and long-term interest rates to remain at their present or lower levels”.

UK: the BOE policy decision is expected to be on hold. Note that at the November meeting, two dissenters called for cuts to the Bank Rate. The nine-person committee had previously voted unanimously for an unchanged Bank Rate at every meeting in 2019.

The key data release on the noght was US oil inventories which were down:

But, as you can see, it’s really just a rotation from oil to gasoline production.

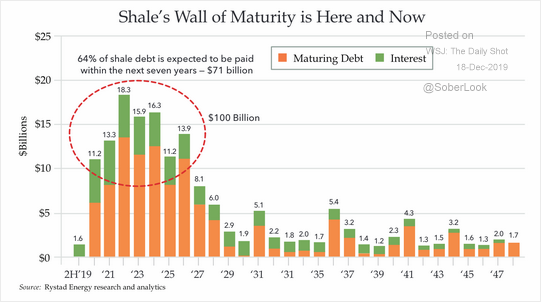

Oil is still in a glut despite the OPEC cuts. Prices are not high enough yet for more shale so they could grind up a bit more. Shalers have been feeling the heat in the $50s:

Drilling has fallen and they’ve been running down DUCs. There’s a wall of maturity ahead too:

The last thing the US economy needs is a spike in the long bond. It’s collapse single-handedly revived US property and its economy amid the trade shock.

The Fed isn’t going to chase oil anyway so I can’t see yields getting far.

But while it runs, in these days of unconventional oil and gas strength supports both the USD and AUD.