US manufacturing PMI (Markit) slipped from 52.6 to 52.5 (vs 52.6 expected), although services PMI did rise more than expected (52.2 vs 52.0 est., 51.6 previous). The Fed’s NY (Empire) manufacturing survey rose from 2.9 to 3.5 (vs 4.0 expected), the components mixed. Homebuilder sentiment (NAHB) rose from 70 to 76 (vs 70 est.) – the highest since Dec 1998 and near the 78 all-time high (1978). Apart from rising house prices, the NAHB cited home prices, the NAHB cited the good economy and the low unemployment rate as supportive for the housing industry.

Event Outlook

NZ: The Q4 consumer sentiment survey (Westpac) follows a Q3 reading at seven-year lows. Since then, the economy has shown signs of improvement, notably via the housing market. Business confidence (ANZ) rose to a 2019 high in November but remains in contractionary territory.

Australia: the RBA minutes are released. As per the decision statement, expect the tone around “long and variable lags” of policy to be emphasised as the RBA monitors the economy ahead of the next meeting in Feb. Oct lending indicators are released. This survey is replacing the housing finance survey and will contain revised data on finance approvals.

UK: Oct ILO unemployment rate is anticipated to edge up to 3.9% from 3.8%.

US: Nov housing starts and building permits data are released. Nov industrial production is expected to be up 0.8%, recovering Oct’s 0.8% decline. Oct JOLTS data are released.

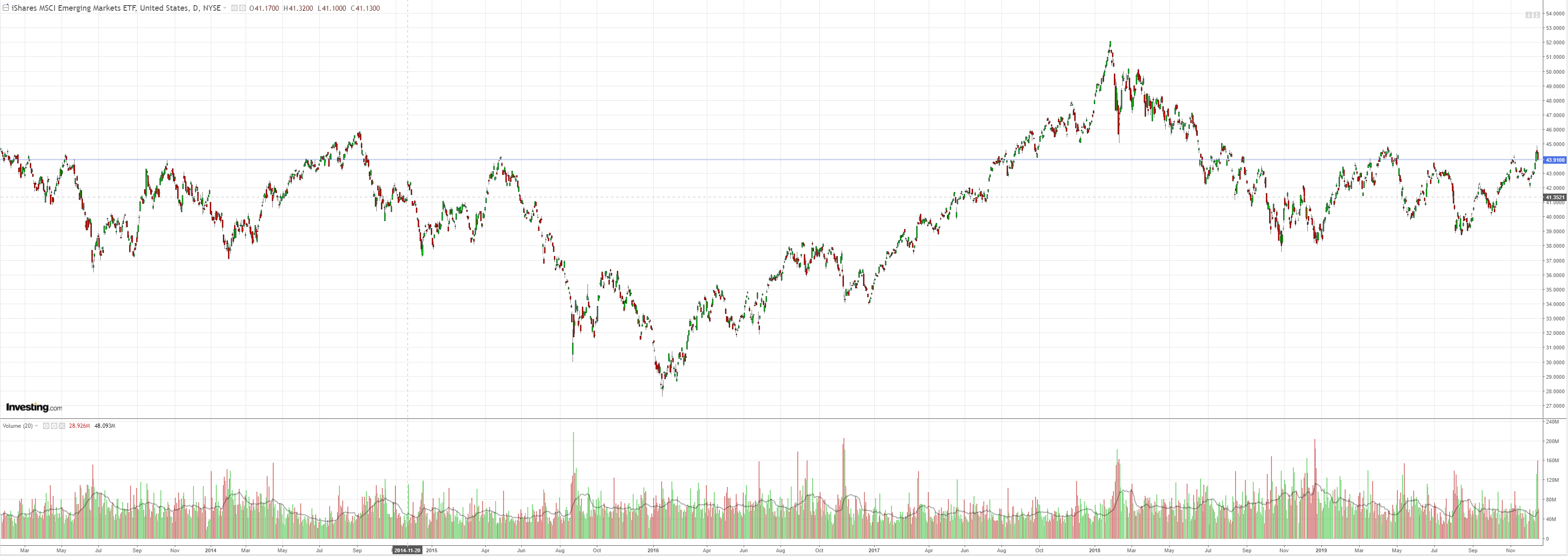

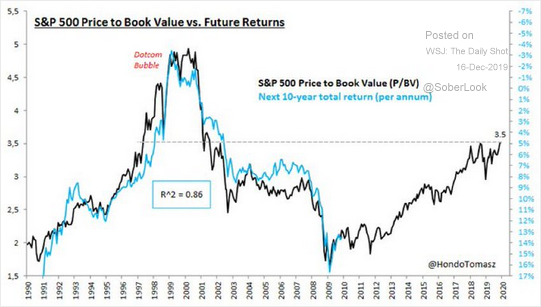

We’re more or less into an equaites bubble here given earnings are not going to come through.

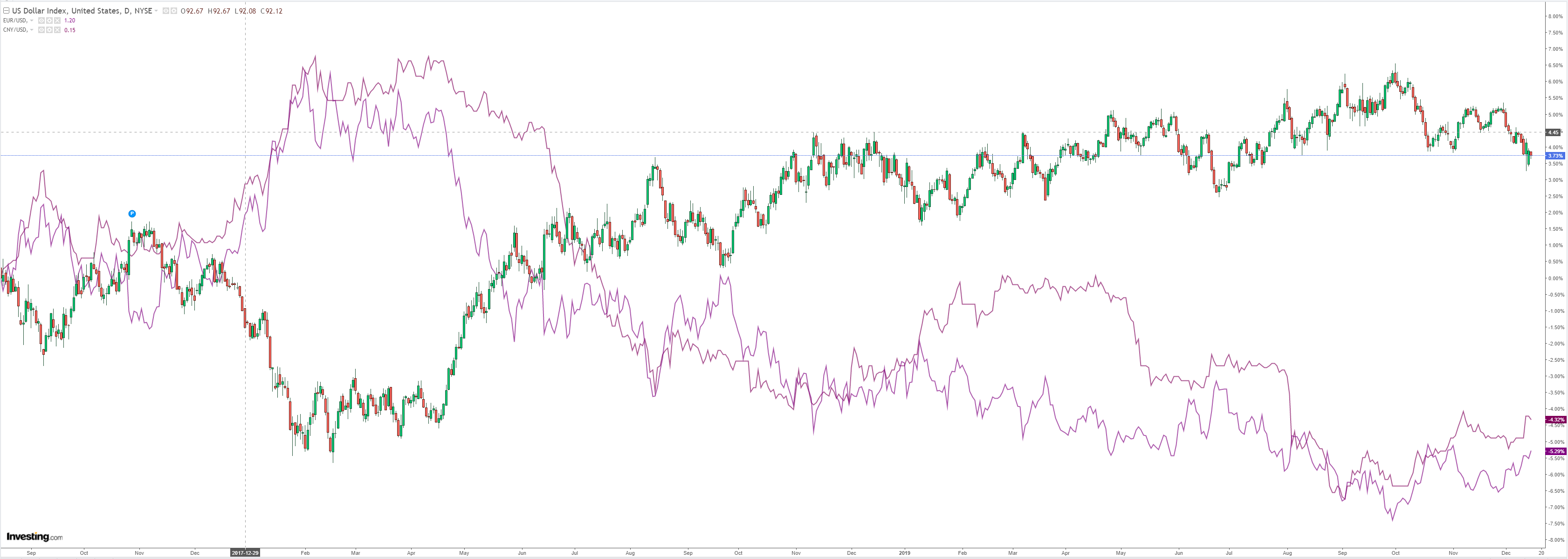

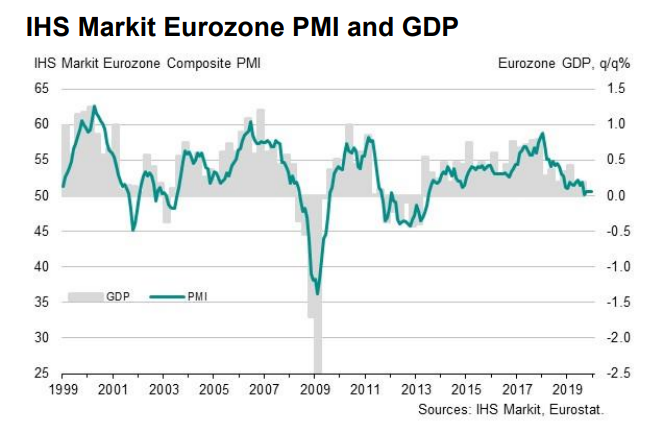

Whie US data was solid, European was terrible:

Advertisement

▪ Flash Eurozone PMI Composite Output Index(1) at 50.6 (50.6 in November). Unchanged.

▪ Flash Eurozone Services PMI Activity Index(2) at 52.4 (51.9 in November). 4-month high.

▪ Flash Eurozone Manufacturing PMI Output Index(4) at 45.9 (47.4 in November). 86-month low.

▪ Flash Eurozone Manufacturing PMI (3) at 45.9 (46.9 in November). 2-month low.

In short, the great European recovery is, in actuality, a deepening industrial bust, but let’s bid that EUR anyway because…deals.

So let’s ask how far this rally gets. It has only the thinnest of excuses in a little easing of political risk. The monetary easing has put a floor under the US economy via housing. But China is still slowing. Europe’s recovery will be weak. US growth is still the leader. The US dollar can’t fall overly far.

The earnings bounce will be muted. But that never stopped a raging bourse before, via Damien Boey at Credit Suisse:

Advertisement

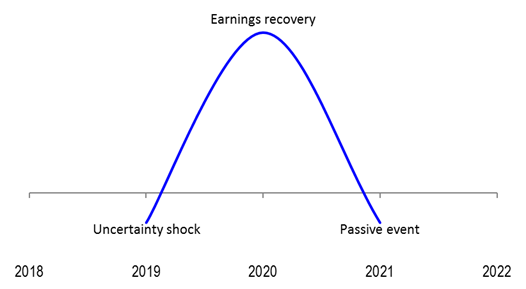

Here is our best graphic attempt to draw a Christmas-tree like figure, and also tell a story about risks. More likely than not, we have earnings recovery to look forward to in 2020 – the growth outlook almost has to look better than what it did in 2019, if for no other reason than 2019 was horrible. But earnings recovery is wedged in between two extreme, and negative states of the world – ongoing uncertainty shocks from US President Trump’s trade war, and an eventual implosion of passive investing longer-term.

Somewhere over the rainbow, investors are cognisant of the risk that higher bond yields and higher volatility will lead to disorderly de-leveraging across markets, ultimately with negative implications for risk appetite and cyclical exposures. Put differently, they are rightly concerned that both the risk free rate and equity risk premium will rise, with the equity risk premium potentially rising faster than the risk free rate. These discount rate movements dwarf whatever happens with earnings in discounted cash flow valuation models, leading to very perverse outcomes. For example, we can have some bond proxies do well with rising bond yields and earnings recovery.

We feel that the multi-factor approach, suitably calibrated, helps us to allow for these perversities now. Momentum captures the near-term undershooting risk from uncertainty shocks, value captures the 2020 recovery story, and quality captures the risk of a passive event longer term.

The complication we are finding is that Trump’s trade war is merging the two extreme ends of the rainbow. We are at risk of experiencing both an uncertainty shock and passive investing event now at the same time. These dynamics are very favourable for quality and arguably defensive momentum investing today. But they also set up a value rotation opportunity tomorrow, when the dust settles.

At no time in the process of this decade long bull market have I considered price action to be a bubble. But we’re on the verge of it today with high valuations and only a lousy earnings recovery to bring them down:

Advertisement

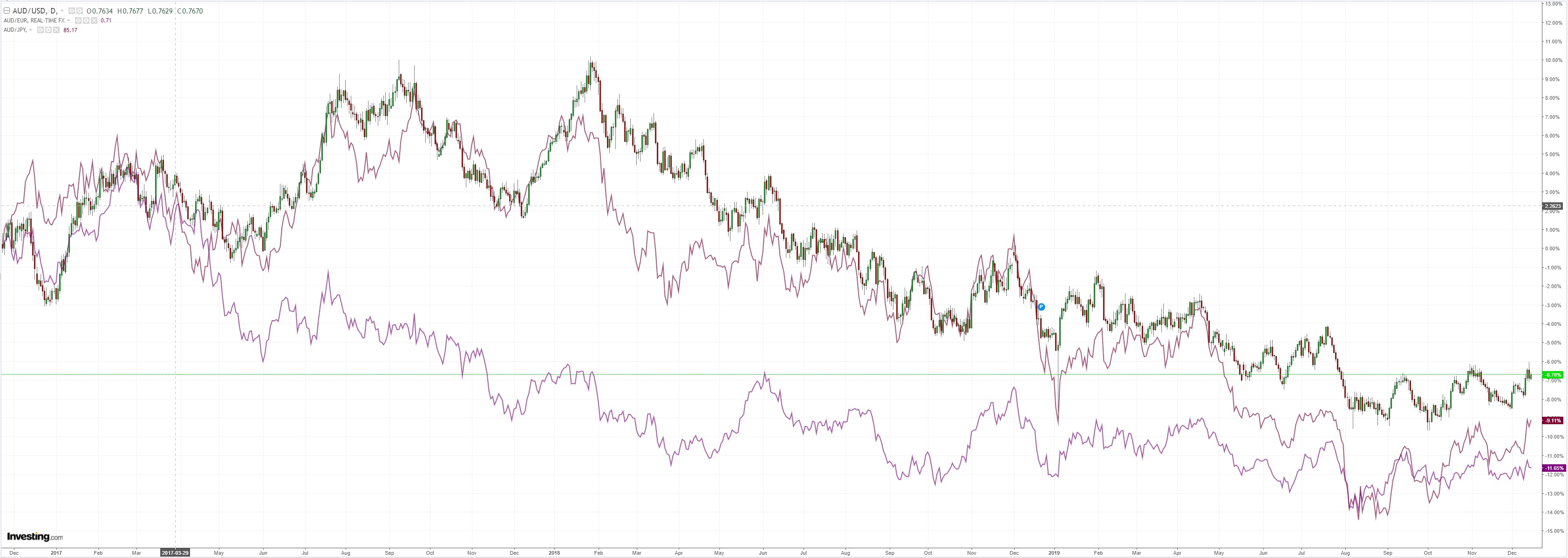

So long as it inflates, the Australian dollar can try to rise against the gale of the weak local economy and more RBA easing.

But when it pops there will be shit over everything, including the AUD.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.