DXY was stable last night:

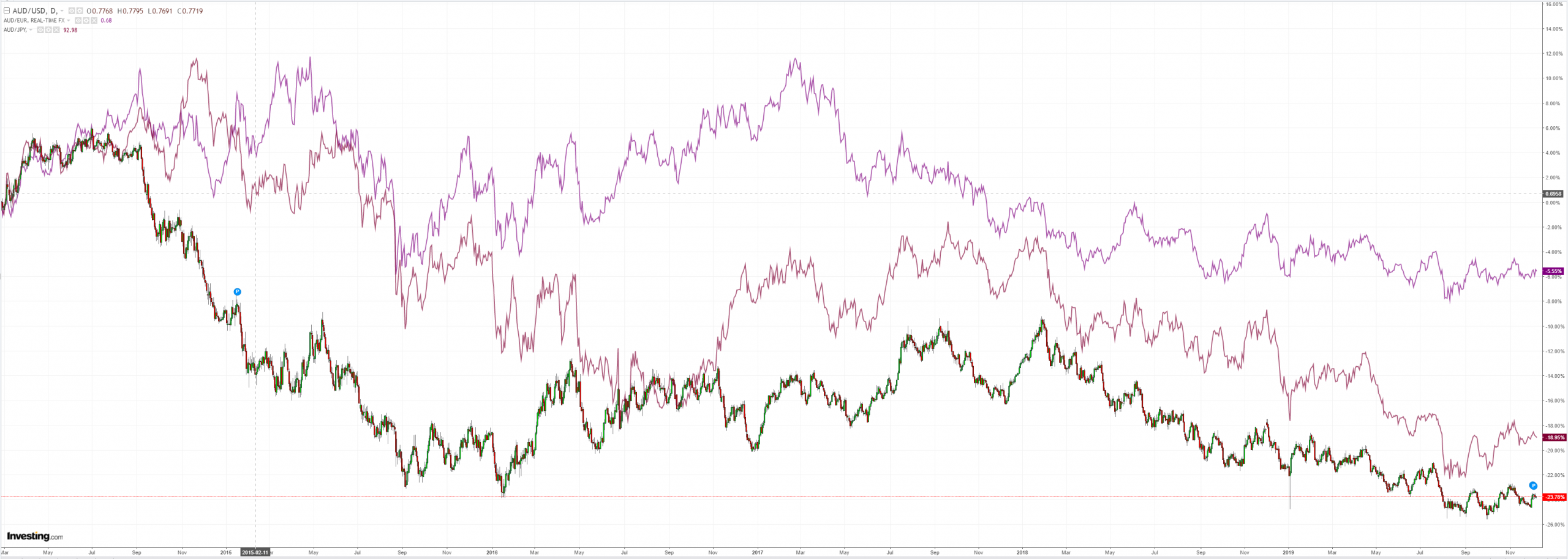

The Australian dollar eased versus DMs:

And EMs:

Gold is struggling:

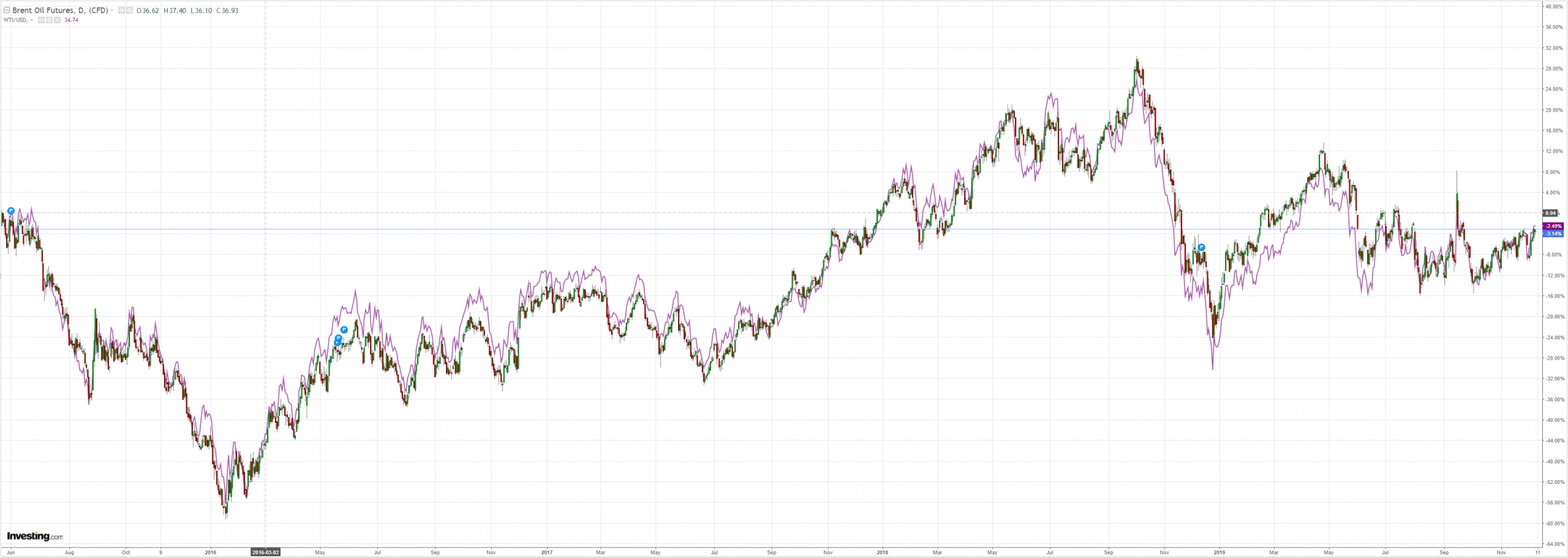

Oil is firm after the surprise OPEC deal:

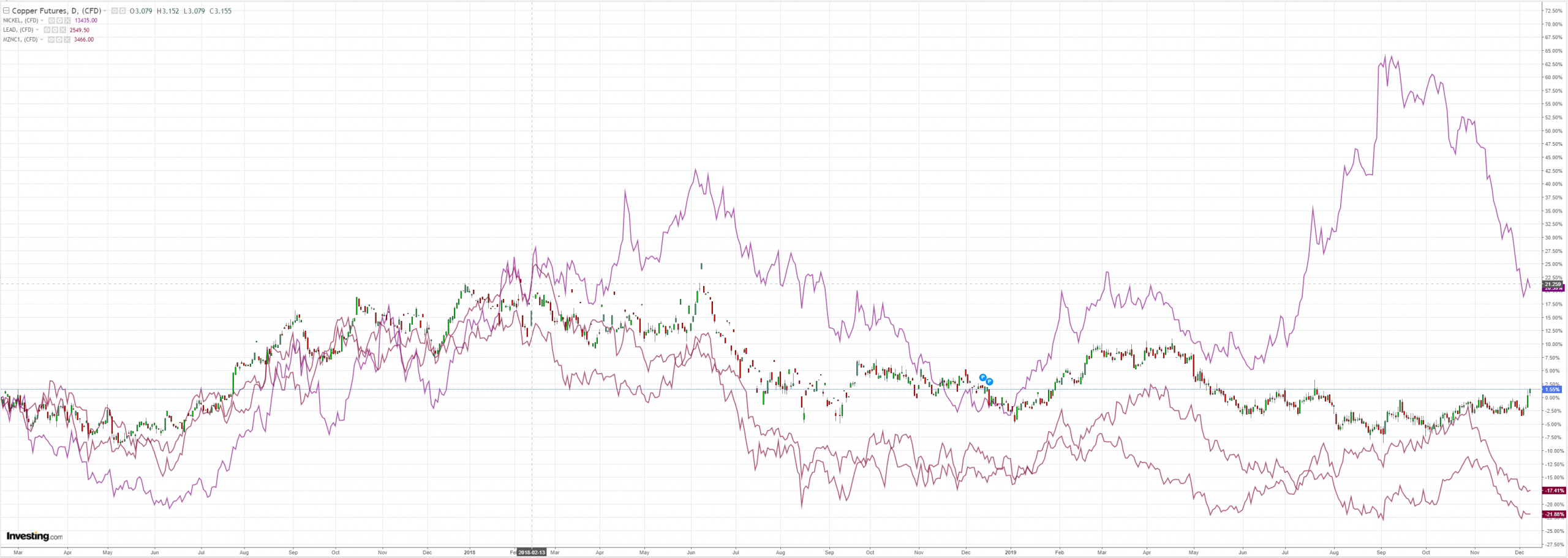

Metals are weak but copper has bounced:

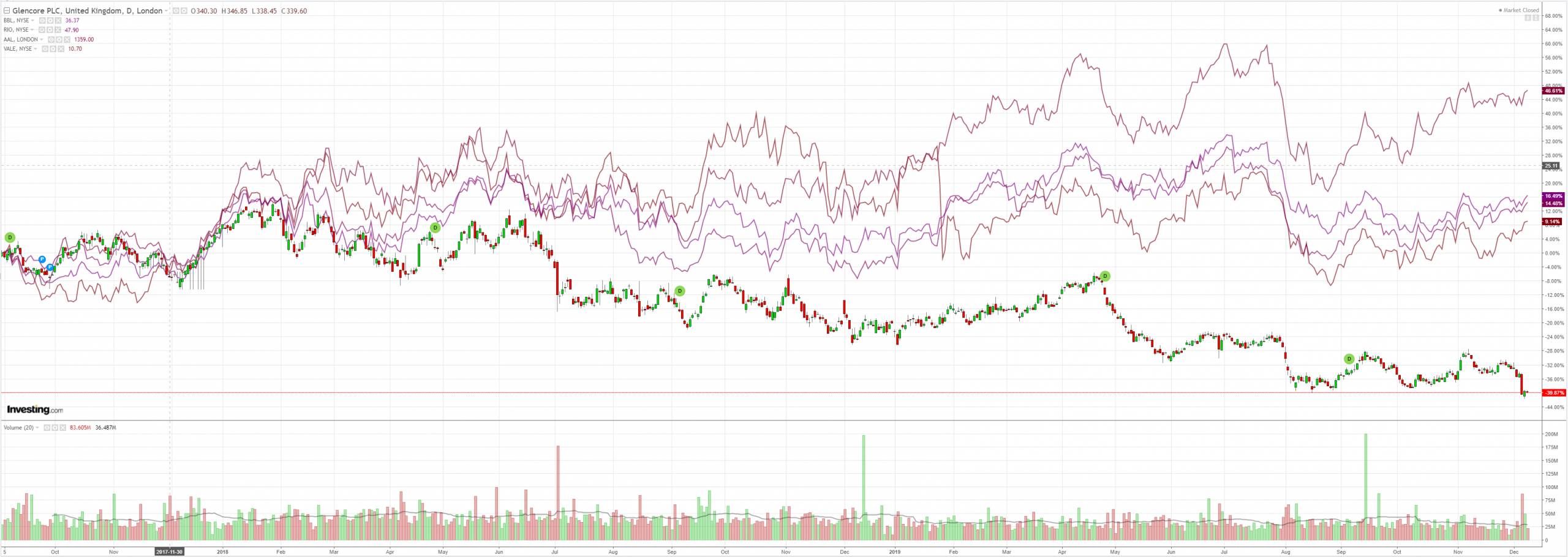

Miners continued on:

EM stocks struggled:

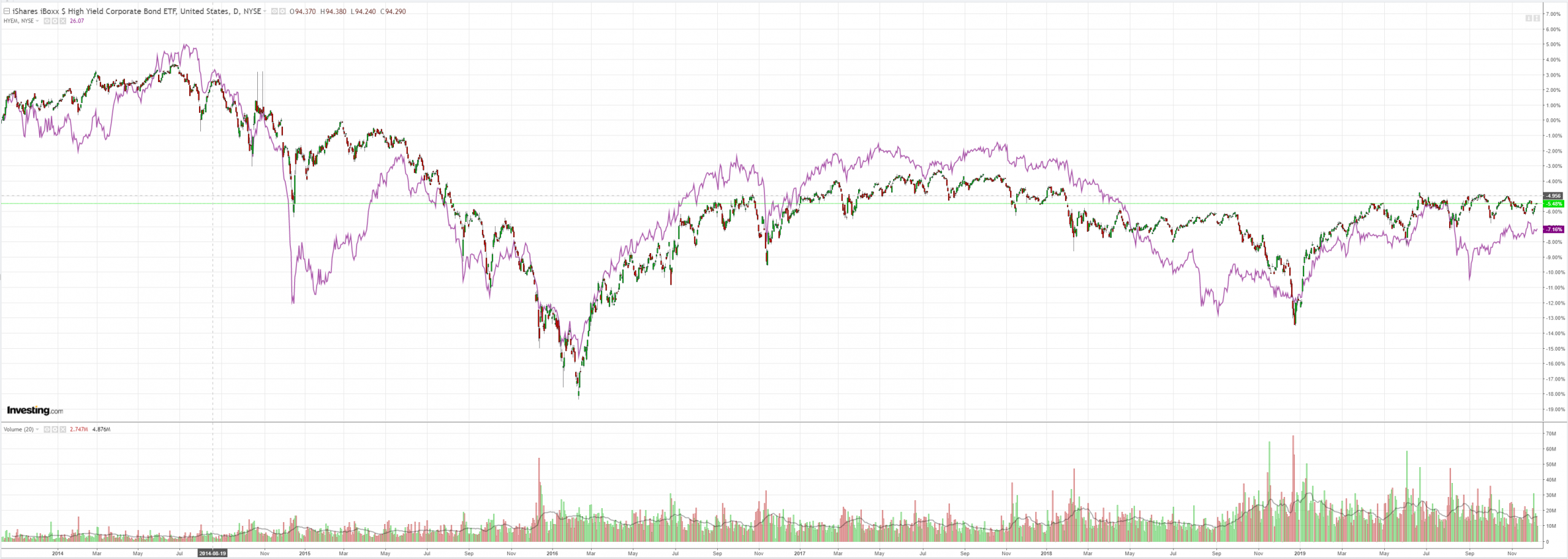

Junk is stable:

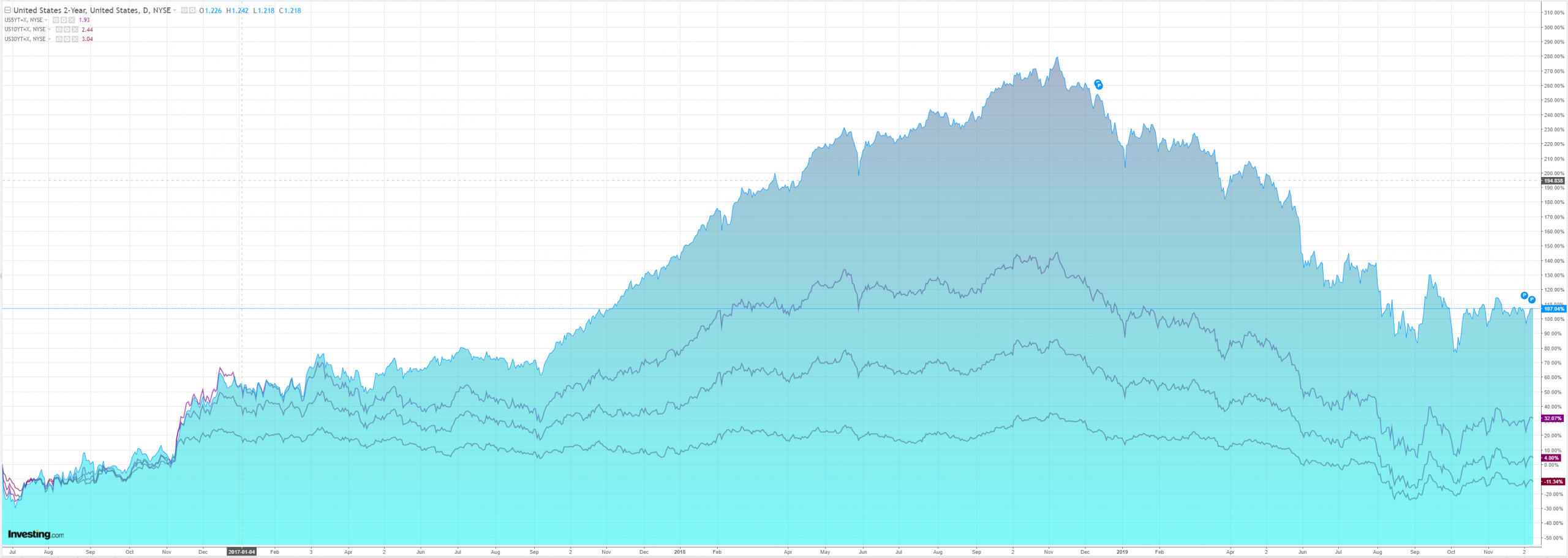

All bonds were bid:

Stocks faded:

Westpac has the wrap:

Event Wrap

German Oct. trade balance rose to +EUR21.5bn (est. +EUR19.3bn, prior +EUR21.2bn), exports up 1.2%m/m (imports flat).

Canadian housing data was slightly disappointing, Nov. housing starts at 201k annualised (est. 215k) and Oct. housing permits down 1.5%m/m (est. +2.8%m/m, prior revised to -5.9% from -6.5%).

Both the Mexican President and US Democratic House officials stated that the USMCA (US-Mexico-Canada) is very close to a trade agreement.

Event Outlook

Australia: RBA Governor Lowe speaks at the AusPayNet Summit, Sydney, 9:05am. The speech will be followed by media Q&A. RBA Assistant Governor (Financial System) Bullock participates on a panel at the AusPayNet Summit, Sydney, 1:45pm. Nov NAB business survey last showed conditions and confidence both below average. Of key interest in this month’s release is if there is any Black Friday related boost to retail conditions.

China: Nov CPI and PPI data are released.

Europe: Dec ZEW survey of expectations bounced off lows to -1 in Nov but remains at an overall below average level.

US: Nov NFIB small business optimism is anticipated to remain at an optimistic level of 103.1.

There was little to report on trade war rumours, which is all that matters these days, so markets drifted. There is some wrap up data to look at, though, which gives us a nice taste of what we can expect for 2020.

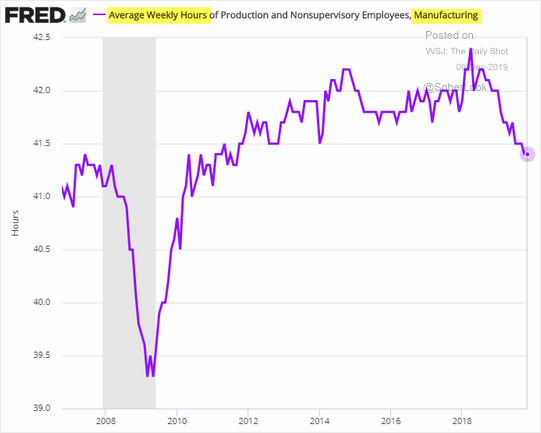

The strong US jobs market is first up. We can expect a softening as the global industrial recession takes its toll. But amid widespread skills shortages it appears cuts in hours are more likely than job losses:

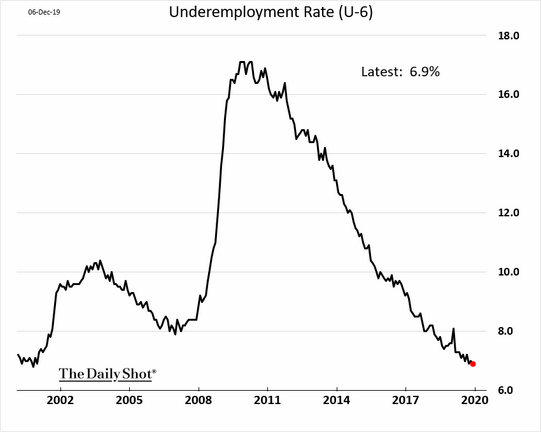

The underemployment rate is yet to register any pick up so that is probably ahead:

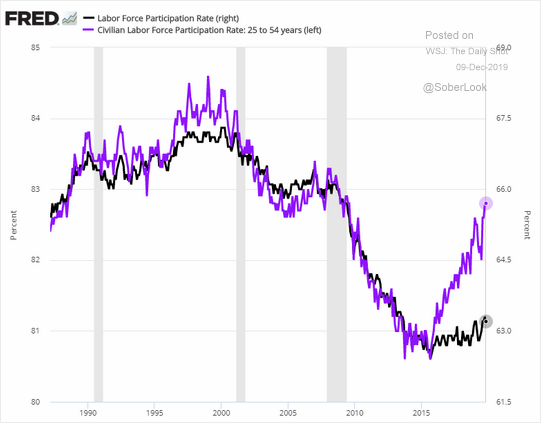

As the participation finally jumps back to life:

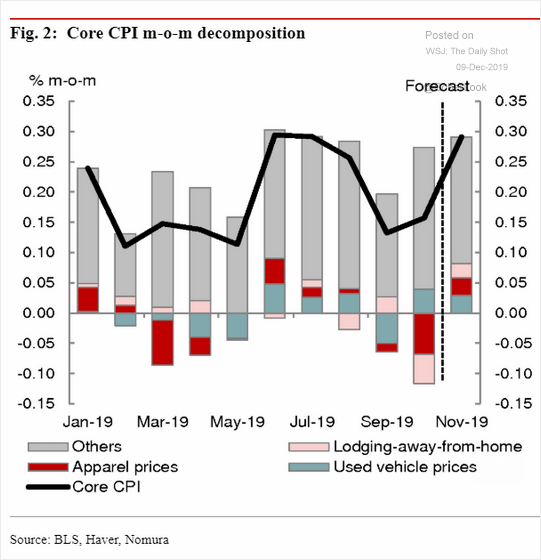

There are still some inflationary pressures thanks to tarrifs:

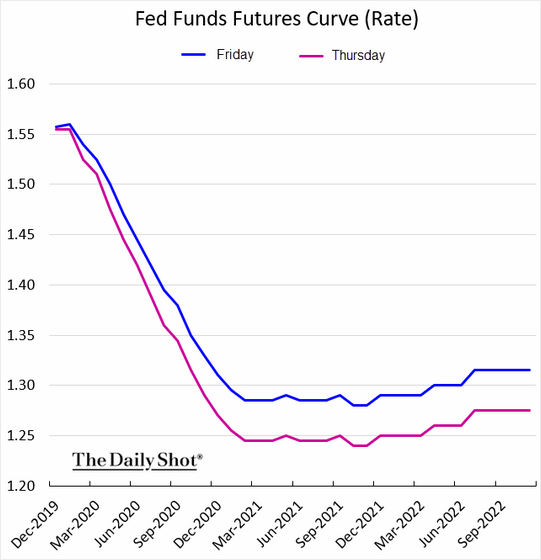

But futures only have one more rate cut priced:

If there are no further political disturbances, the Fed holding is now the base. US housing is rising nicely and the consumer stable with decent wages growth. But that is a big “if”.

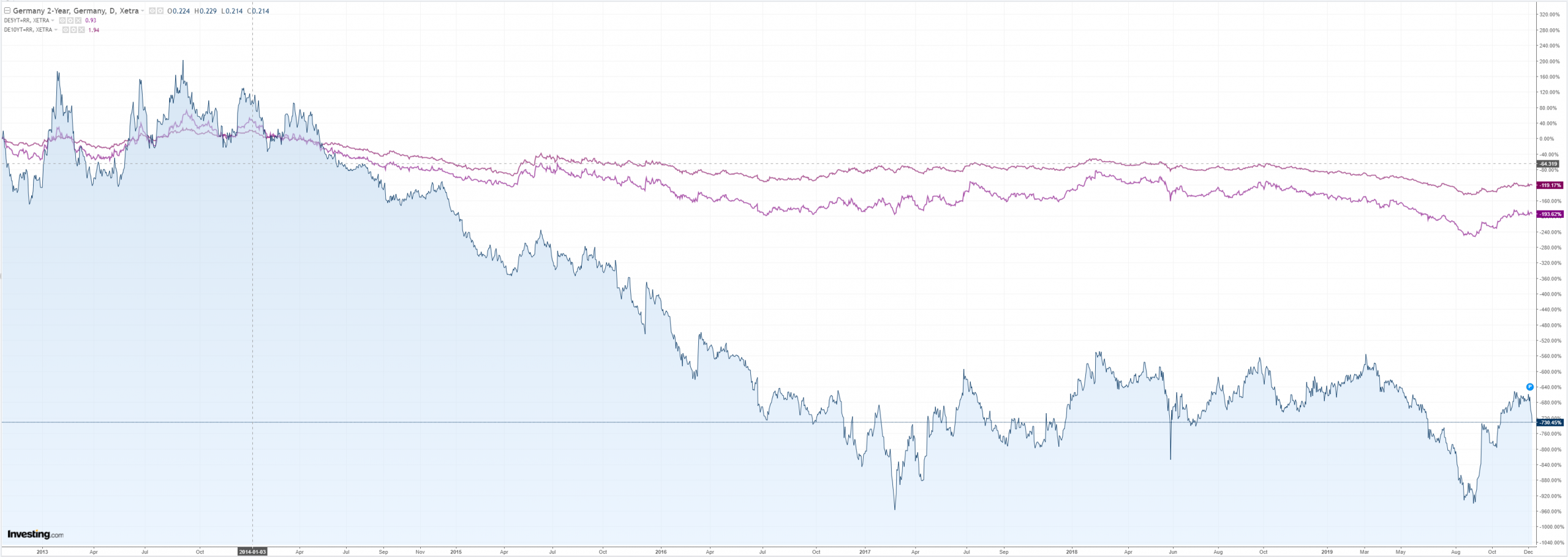

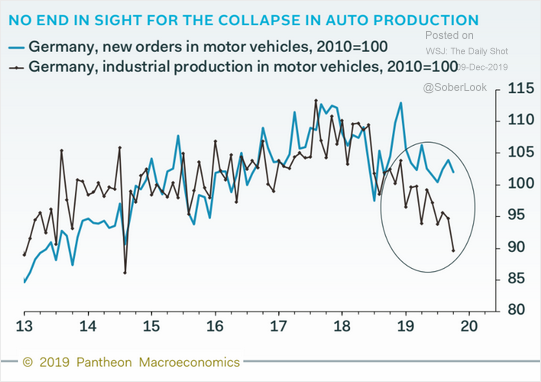

Against a steadily growing US at around 2%, Europe is destined to lag again. Germany is still struggling with the great car smash:

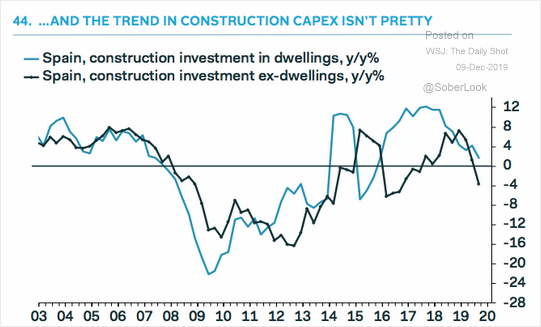

And wider Europe is fraying:

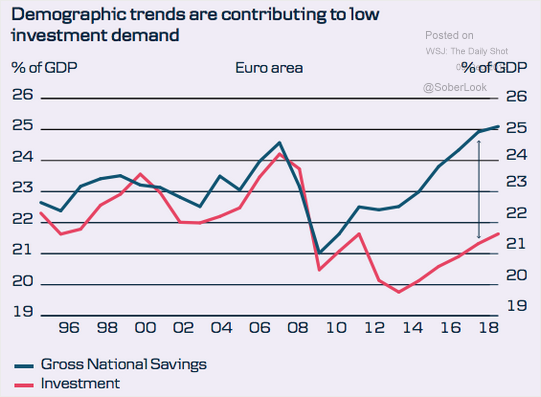

The entire continent is still over-saving:

Which is one reason for lackluster global growth. But Germany still appears to have little apetite for fiscal spending.

It may improve a little but Europe will lag US growth and inflation with little prospect of an exit from extraordinary easing.

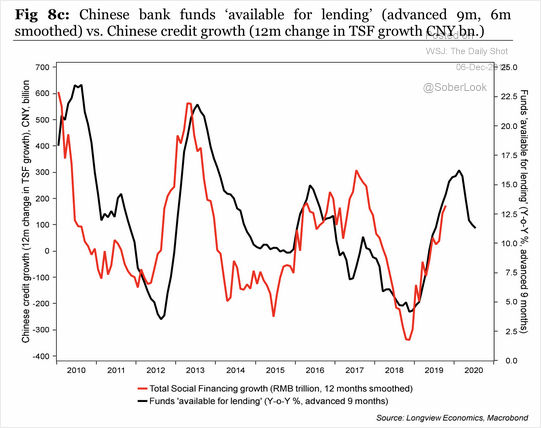

So, that favours the USD over EUR. In turn, that will keep the pressure on China and EMs via tight capital accounts. As the trade war manifests on multiple fronts, from tech to Hong Kong, I don’t expect any lift in the Chinese growth rate, either. Indeed, more slowing is baked in as more decoupling from the global supply chains transpires, and credit rolls over:

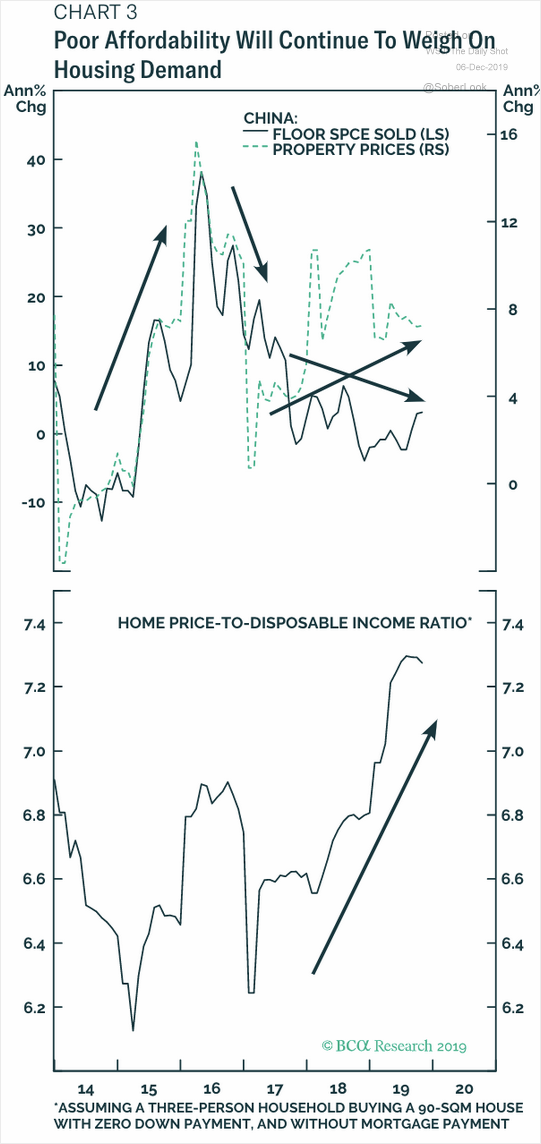

Plus the property market slows:

As major miners overcome this year’s accidents we can expect more supply to meet fading demand for iron ore and coal leading to material price falls.

In conclusion, US growth leadership is intact next year. Europe will recover only a little. China will keep decelerating. That says to me that the two major drivers of Australian dollar value will keep pushing the price down. Falling bulk commosity prices will land on an income strangled economy like a heat wave upon a desert. And the negative yield spread will widen as the RBA cuts twice more and embarks upon QE while central banks elsewhere pause.

Markets are still materially short the AUD so that is some downside protection but 65 cents is a comfortable base case for 2020.

And given all major possible shocks are China-related, most risk cases project it even lower.

———————————————

David Llewellyn-Smith is Chief Strategist at the MB fund and MB Super which is overweight international shares that will benefit from a falling Australian dollar.