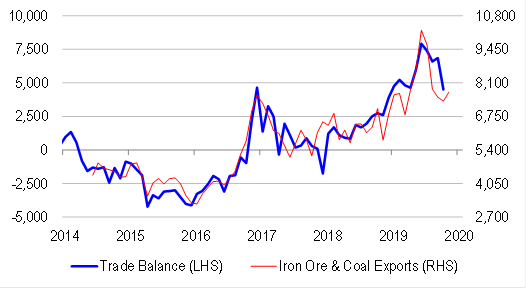

Trade data came in below expectations. The surplus declined to $4.5 billion in October from a downwardly-revised $6.8 billion. Interestingly, the decline in the trade balance, and downward revisions to prior months’ data, have brought the official data back to be much more in line with unofficial indicators such as the value of resources exports. Previously, it looked as though the trade balance was materially overshooting.

Timing of the trade decline could not be worse. We have already seen bank credit growth slow to a crawl. And beneath the radar, we have also seen the Federal government re-start its austerity program. The Federal budget balance has swung sharply from deficit to surplus in early 4Q, just as we were about to celebrate the outsized contribution of government consumption to 3Q GDP growth …

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.