As I analysed the recent MYEFO projections, one thing stood out:

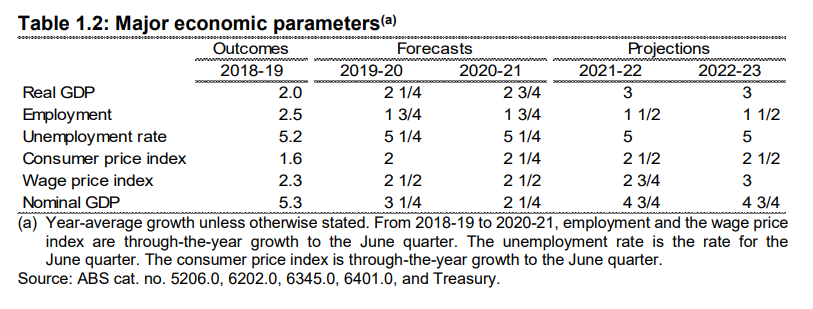

Here’s the economic outlook:

GDP for this year might be OK but it’s odds-on too bullish. But 2020/21 is deluded and so are the outer years.

It is tradition to forecast Futureboom! to bailout today’s stupidity. But it doesn’t ususally accompany a forecast commodities bust which Treasury has started to factor in. The coming term of trade shock slams nominal growth below GDP in 2020/21. Yet, magically, wage growth and inflation are going to accelerate as that happens.

Good one. I guess Treasury was on holiday from 2011/15.

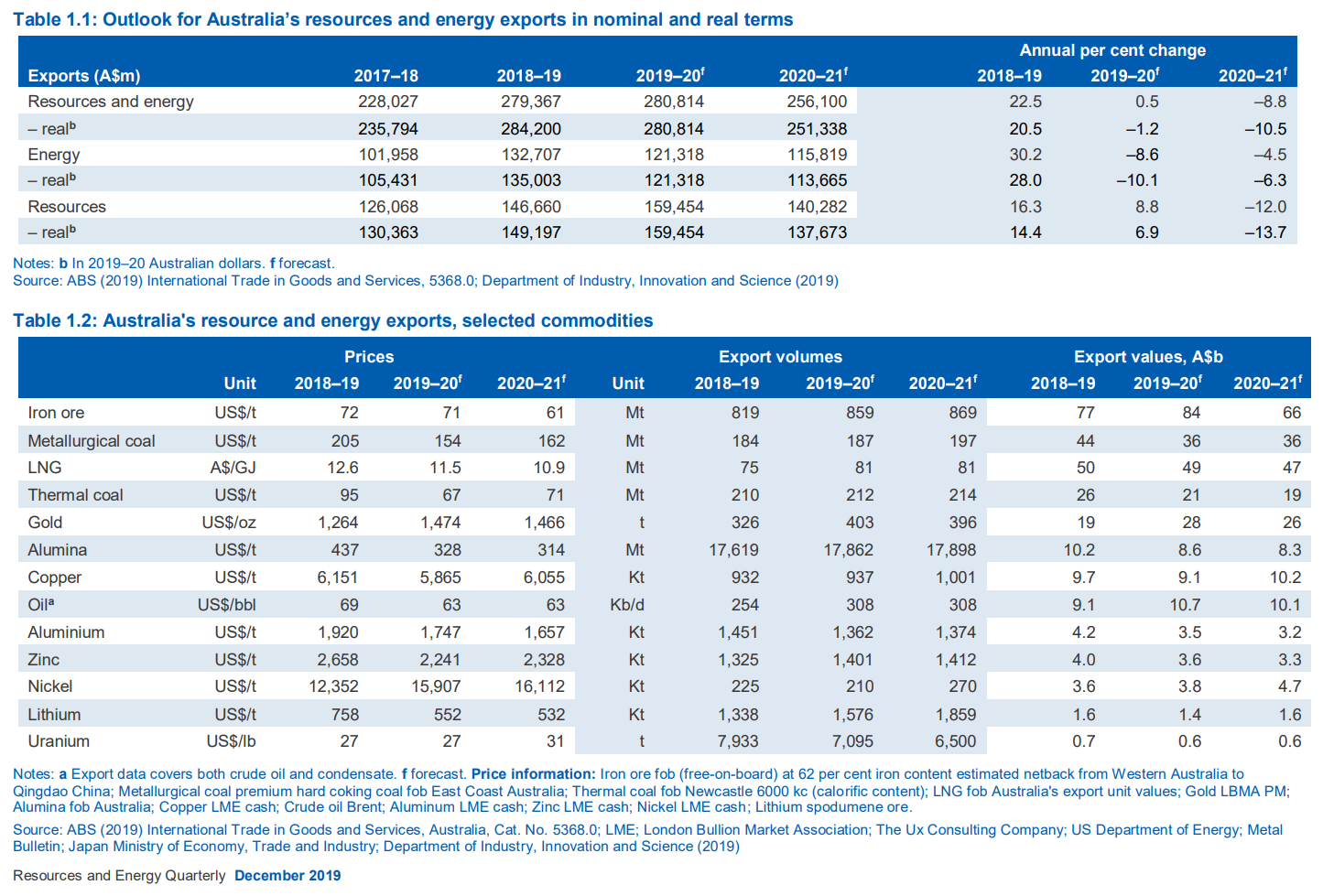

But the Office of the Chief Economist wasn’t. In its updated outlook today it dares to go much closer to the truth. It also forecasts a commodities bust for 2020/21 as China keeps slowing and the supply side normalises for iron ore and coking coal:

Advertisement

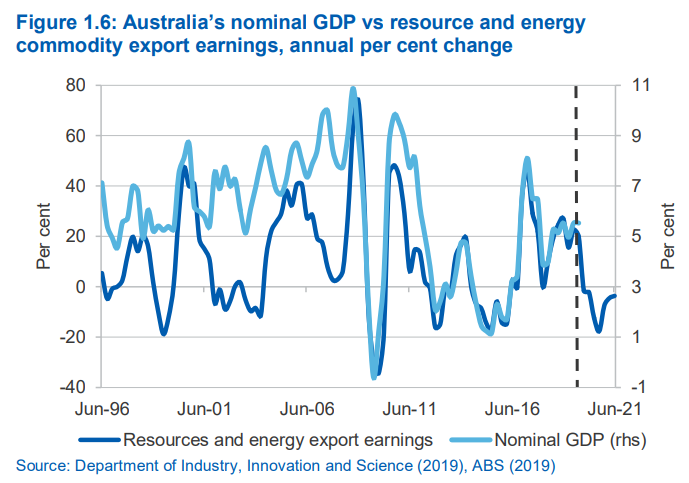

But it understands what this will do the economy much better. To wit, cratering nominal growth:

In actuality, the MYEFO commodites outlook is more bearish than that of Industry. But while MYEFO also projects nominal growth of 2.25%, allowing it to at least pretend, not very well, that wages growth will accelerate.

Advertisement

Industry has done a more credible assessment given the very close relatonship between the terms of trade and nominal growth in recent years and concluded 1% is likely.

That will result in a wages wipeout in 2020/21 as national income dries up, with bugger all recovery to boot in the years following.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.