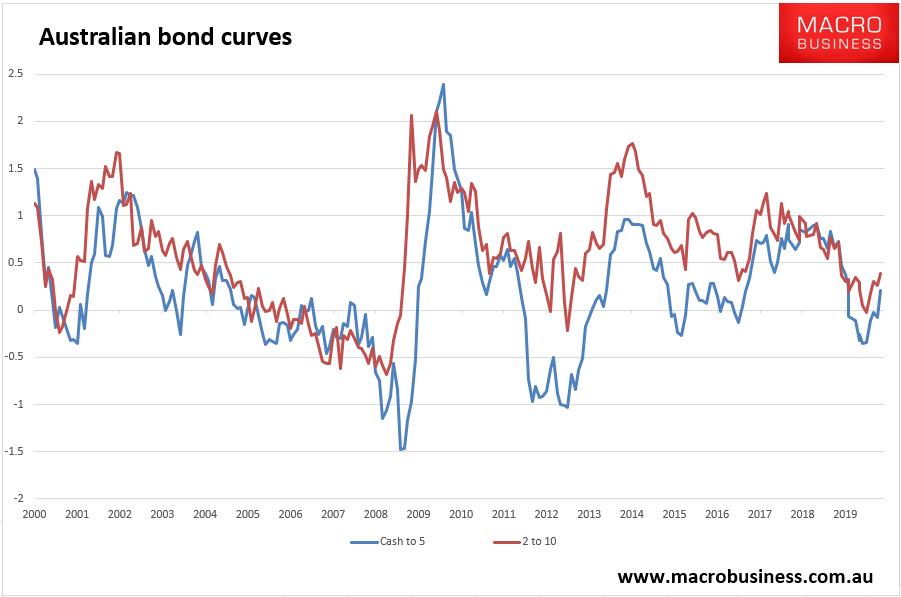

Because that’s how good the global and Australian recovery will be in 2020. Bonds have just about completed pricing the first rate hike:

This is largely being driven by global steepening as stocks run wild:

Advertisement

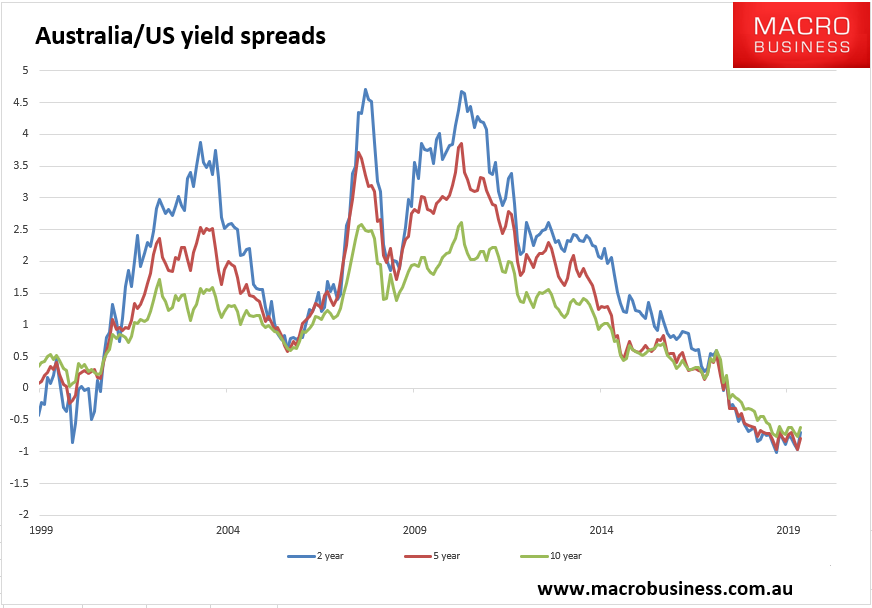

But is has also been the result of local bonds selling faster than US, narrowing the spread: