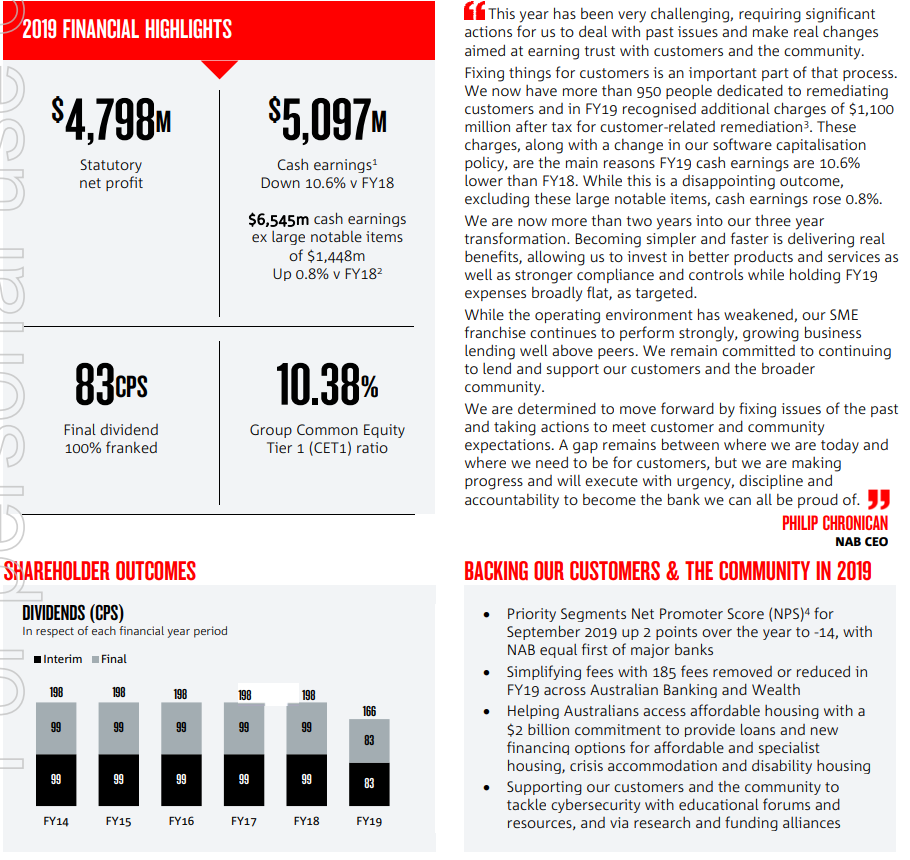

NAB just posted another banking profits shocker with earnings crushed and the divvy slashed:

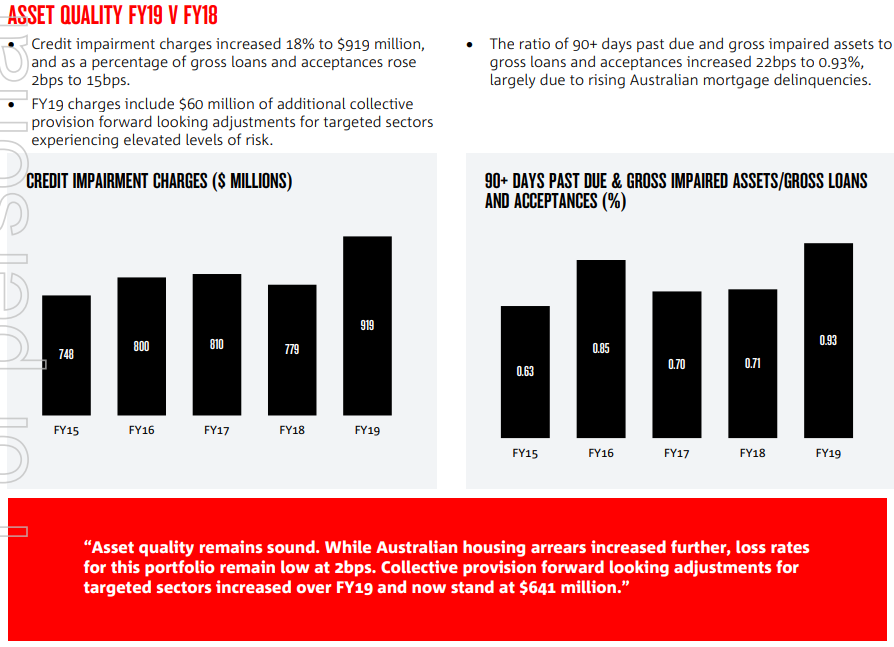

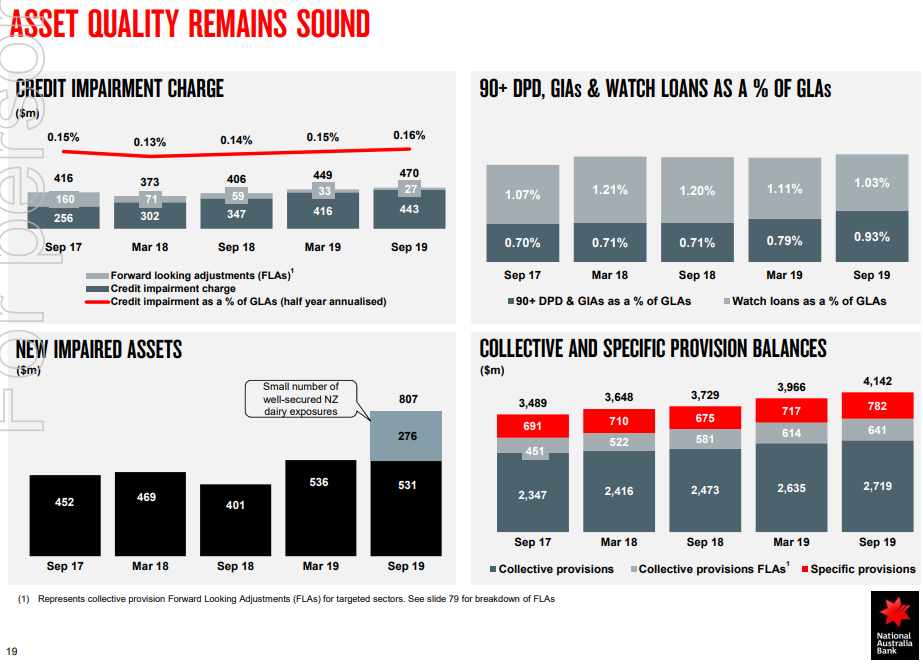

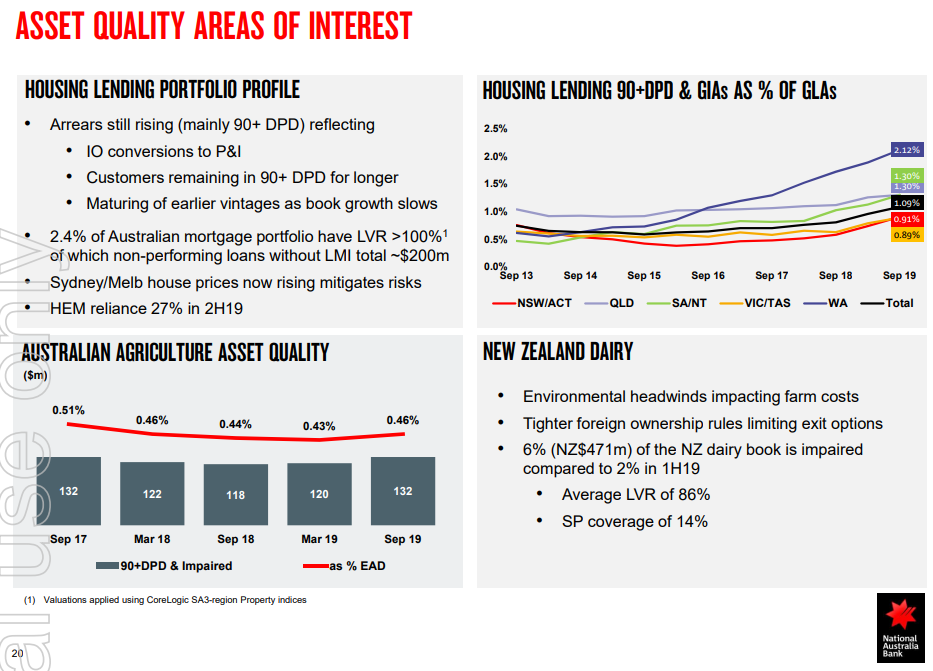

Asset quality is still deteriorating low off a low base:

Advertisement

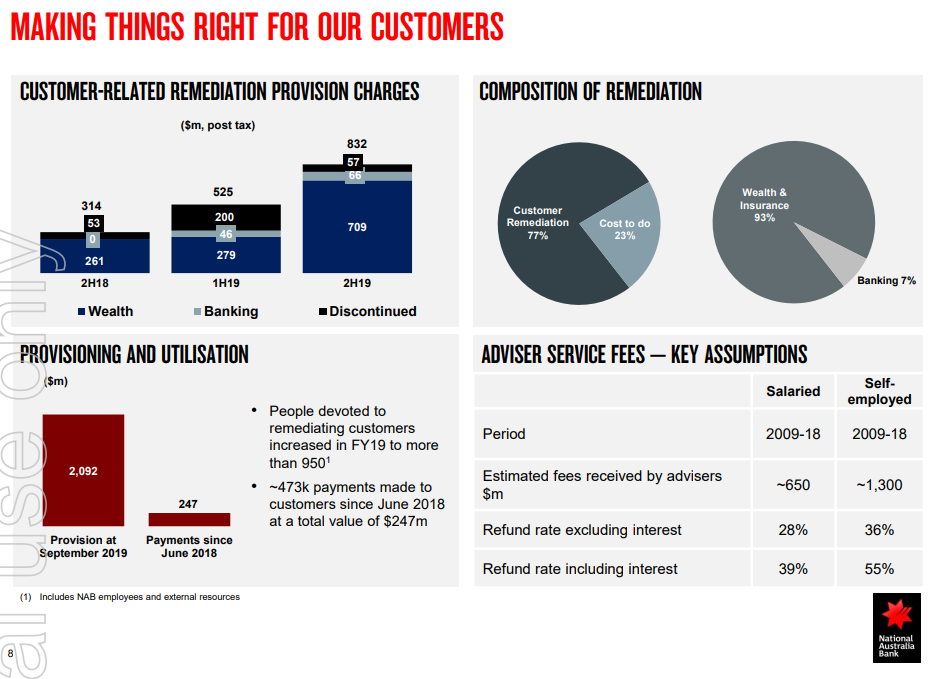

Remediation bills are huge and ongoing:

NAB just posted another banking profits shocker with earnings crushed and the divvy slashed:

Asset quality is still deteriorating low off a low base:

Remediation bills are huge and ongoing:

The full text of this article is available to MacroBusiness subscribers