During the peak of the last housing cycle in 2017, MB coined the phrase “shrinkflation” to describe the peculiar situation whereby housing prices rise strongly alongside crashing sales volumes.

Australia’s housing market is experiencing another round of shrinkflation with dwelling values surging at the same time as turnover remains anaemic.

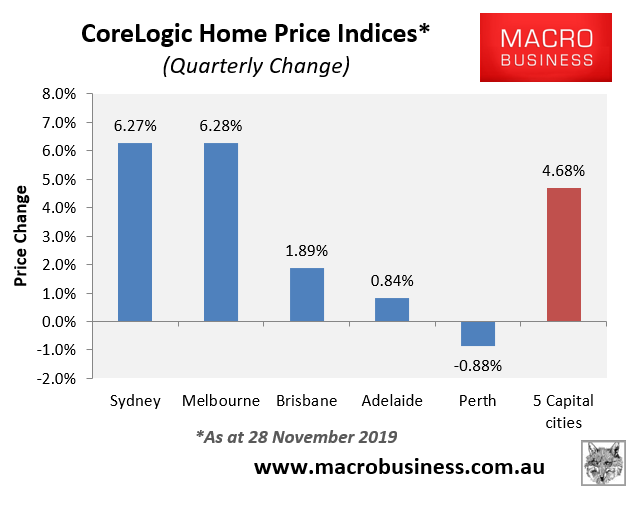

A new report from CoreLogic tells the tale, with far fewer homes for sale this spring despite the massive lift in values and buyer interest:

Advertisement