CoreLogic has released an interesting report showing that despite cratering mortgage rates and the recent steep housing correction, Sydney and Melbourne housing affordability is still worse than a decade ago:

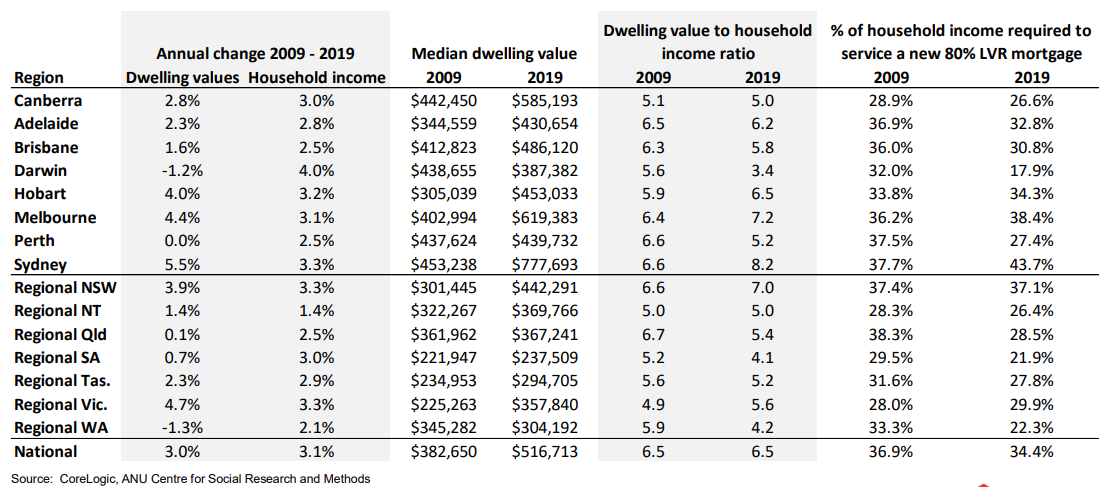

The decade ending in June 2019 has seen the national median dwelling value rise from $382,650 to $516,710, an annual increase of 3.0%. At the same time, household incomes (according to estimates from the ANU Centre for Social Research and Methods) have risen at the annual pace of 3.1%, up from $59,020 per annum in 2009 to $79,872 in 2019. Over the same period, average mortgage rates (according to RBA statistics) fell from 5.1% in 2009 to 4.1% in June this year. The wash up from these movements is that housing affordability, based on the ratio of dwelling values to household incomes, is broadly unchanged across Australia and households are generally dedicating less of their income towards servicing a new mortgage.

Nationally, the ratio of dwelling values to household incomes has varied over the past decade, moving through a low of 6.1 in late 2012 to a recent high of 7.0 in early 2018. In June 2019 the ratio was recorded at 6.5 which is equivalent to where it was in 2009. A ratio of 6.5 simply means the typical Australian household is spending 6.5 times their gross annual household income in order to purchase the typical dwelling…

While most areas have seen housing values become more affordable relative to incomes, some areas have seen affordability worsen. Sydney, Melbourne and Hobart have seen housing values rise at a faster rate than household incomes which has eroded affordability. The typical Sydney household is now spending 8.2 times their gross annual household income in order to purchase the median value dwelling, up from 6.6 ten years ago. Melbourne households are spending 7.2 times their annual income (up from 6.4 in 2009) and Hobart households are spending 6.5 times (up from 5.9)…

It’s a similar story with mortgage serviceability. Despite mortgage rates falling to the lowest level since at least the 1950’s, households in Sydney, Melbourne and Hobart are generally dedicating a larger proportion of their incomes towards servicing a new mortgage than they were in 2009. Based on the proportion of household income required to service a new 80% LVR mortgage, Sydney households are dedicating 43.7% of their gross annual household income on mortgage repayments compared with 37.7% ten years ago. When mortgage rates were around 9% in early 2008, Sydney households were dedicating a much larger 54.2% to service a mortgage. Melbourne households are dedicating 38.4% on average to service a new 80% LVR mortgage (up from 36.2% in 2009) and Hobart households spend an average of 34.3% of their income on a new mortgage (33.8% ten years ago)…

Although housing affordability has worsened relative to ten years ago in Sydney and Melbourne, the decline in home values together with a subtle rise in household incomes and lower mortgage rates has seen affordability and serviceability record a temporary improvement in these areas. Since June, dwelling values have surged higher while income growth has remained sluggish, implying that the improvement in housing affordability that has been delivered via a fall in home values is now being eroded.

Longer term strategies for improving housing affordability should include both supply and demand side considerations, as well as taxation reform. On the supply side, ensuring infrastructure programs, land release and town planning policies are keeping pace with population growth is important. On the demand side, population growth drives housing demand, as do stimulus measures such as first home buyer grants and tax concessions. Incentivising jobs growth and infrastructure improvements in more affordable areas would support a redirection of population growth into areas where housing prices are more achievable. Removing stamp duty would also help to improve housing affordability and housing mobility by lowering the transactional costs associated with purchasing a home.

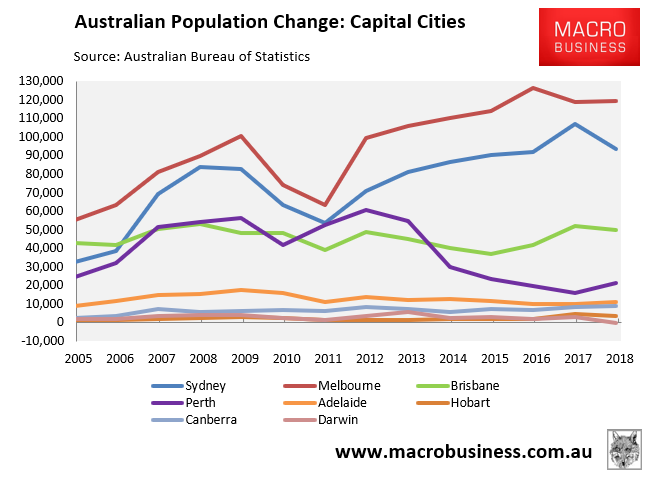

The reason for Sydney and Melbourne’s worsening of affordability relative to the rest of the nation is obvious. Over the past decade, population growth has boomed in these two markets, whereas it has moderated or remained flat elsewhere:

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.