Dr Bob Birrell and David McCloskey have released a an excellent report, entitled Australia’s ‘Jobs and growth’ strategy: pathway to a low productivity economy, which argues that surging low-skilled migration is undermining wage growth and creating a low-productivity economy.

Below are key extracts:

Attempts to kick start growth in the Australian economy have so far met with lacklustre results. Wage growth is weak and stimulus measures such as the recent tax cut have barely had an impact. Our main concern is to explore why monetary policy has so far not worked. The central hypothesis is that an important factor has been the rapid growth in Australia’s labour supply. As we will see, this is a core component of the Coalition government’s ‘jobs and growth’ strategy…

When addressing the House of Representatives Economics Committee in August 2019, the governor, Phillip Lowe, made a revealing statement.

He admitted that monetary policy was not working and that this was because Australia’s labour supply was expanding faster than the RBA had projected. This, he acknowledged, meant that that employers have not had to compete harder for workers and thus had not had to increase wages.

Lowe said that the cause of this strong labour supply was an upward movement in labour market participation. He admitted that the RBA had not predicted this. Lowe said that the bank had expected lower interest rates to generate increased consumer spending. This would in turn have led to increased competition for labour which would lift wages. But the higher rate of labour-market participation had undermined this expectation.

Lowe’s statement is consistent with our hypothesis about the importance of growth in the supply of labour. However, Lowe had nothing to say about the main source of labour force growth, that is high rates of net overseas migration to Australia (NOM). We think he did not mention this because to do so would have challenged the Coalition government’s (and the RBA’s) commitment to the ‘jobs and growth’ strategy.

‘Jobs and growth’ is a shorthand statement of the Coalition government’s economic strategy. It refers to the Coalition’s commitment to promoting high levels of job growth and continued economic growth. The strategy in part refers to the Coalition’s claims to being a good economic manager, via budget thrift, pro-business taxation and regulatory policy and a willingness to promote continued economic reform.

The strategy also includes a firm policy commitment to maintaining a high level of population growth, mainly deriving from NOM. As we show, this commitment is central to the ‘jobs and growth’ strategy but not openly stated for public consumption.

The Coalition and its advisors (including Treasury and the RBA) know that while this population policy prevails it will put a floor under Australia’s aggregate economic growth performance – in the process helping to sustain the narrative of Australia’s 28 years of unbroken economic growth.

To this end the Coalition has put in place migration policy settings which ensure NOM remains around the present level of 250,000 a year over the next two years. The NOM component will deliver population growth of around 1.0 per cent population growth a year, and will remain the main source of Australia’s current overall annual population growth of 1.6 per cent.

The recent reduction in the permanent program from 190,000 to 160,000 a year is window dressing. This cut is being more than made up by measures that allow temporary migration to continue to expand. The stock of migrants holding temporary entry visas in Australia has expanded from 1.8 million in June 2015 to 2.2 million in June 2019. Such is the effect of this expansion that Australia’s current migration program is best described as a low-skill, rather than a high-skill program.

This policy includes a widening range of subsidies to various industries, including the international education industry and the horticultural industry. It also includes migrant visas which prevent the recipients from working and living in metropolitan areas. In each case temporary migrants are allowed extra time in Australia’s labour market in return for enrolling in, working in or locating in these industries or locations. This practice is a de facto subsidy to regional areas…

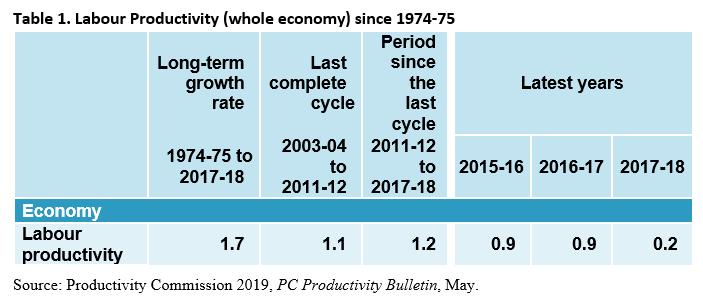

By 2017-18 and 2018-19, almost all of Australia’s increase in output of goods and services was attributable to extra hours worked. The contribution of labour productivity, defined as advances in output per hour worked was negligible (Table 1).

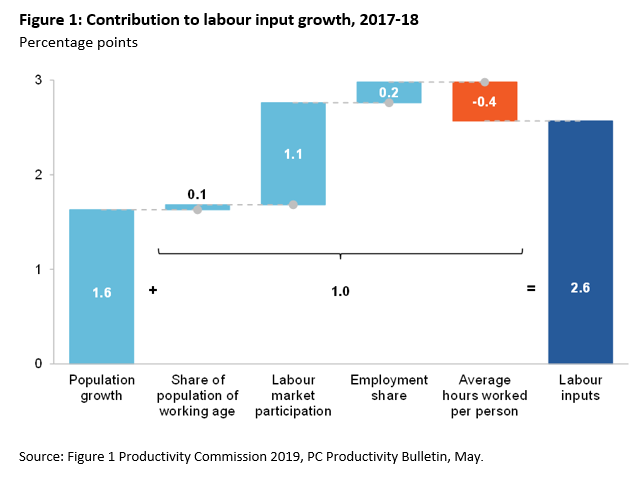

The chief source of extra hours worked was population growth, mainly deriving from NOM. However the rest reflected recent increases in labour market participation (and thus hours worked) amongst older persons and women (Figure 1).

On the expenditure side of the economy most of Australia’s growth in GDP was attributable to extra consumers, plus additional public expenditure and export revenue generated by Australia’s commodity industries.

At present, Australia’s economy is limping along courtesy of the population component of the ‘jobs and growth’ strategy.

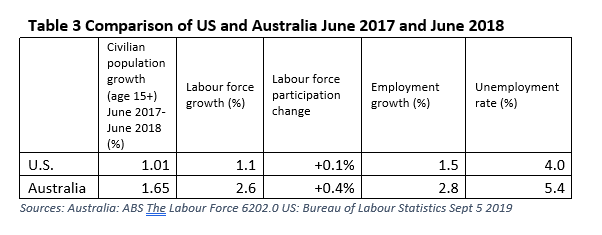

While Lowe did say that an increased supply of labour had depressed wages he did not refer to recent international experience, especially in the U.S. In that country (unlike Australia) growth in the demand for labour is exceeding that of labour supply. The result, as shown in Table 3, is that wage growth and inflation in the U.S. now exceed that of Australia, and the level of unemployment is well below Australia’s.

The RBA simply ignores the obvious labour market consequences of high NOM for labour market competition, especially that flowing from the influx of low-skill migrants on temporary visas. These consequences are evident across a wide range of the industries that rely on such labour.

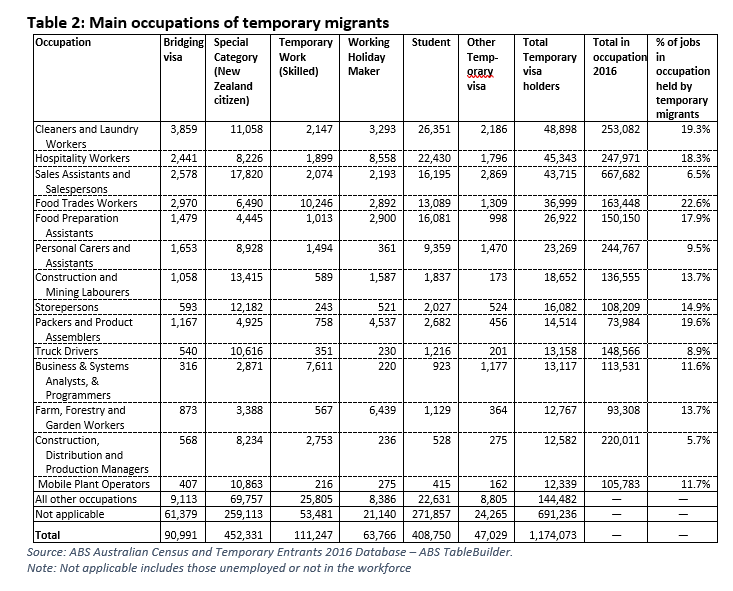

As Table 2 shows, migrants on temporary visas, including New Zealanders, are concentrated in industries which use low-skill workers. Here they create ferocious competition for domestic workers wanting jobs in these industries. This is why there are almost daily reports of employers paying workers below award rates. There is also strong competition for employment in many major professional labour markets.

While this labour supply abundance persists employer do not have to raise wage rates nor do they need to invest in labour saving equipment. If more output is required they can simply run existing equipment harder and/or take on more workers at existing wage rates.

From this perspective the ‘jobs and growth’ strategy is part of the problem rather than the solution.

The Australian economy is at a stalemate. With NOM a crucial part of the ‘jobs and growth’ strategy neither the Coalition nor its advisors can contemplate any reduction in immigration in order to make the labour market more competitive.

The likelihood is that the economy will limp along, deriving most of its growth from extra hours worked and propped up by additional government expenditure, more infrastructure investment and a boost to the housing industry via low interest rates.

All of these measure will deliver low gains in labour productivity. They mean that Australia will continue to move down a low productivity pathway…

The conclusion is that while the ‘jobs and growth’ strategy prevails Australia will be stuck on a low productivity pathway, dependent for its economic growth on continued increases in population.

The strategy is foolish. All it achieves is the addition of an ever larger, relatively unproductive, domestic burden on to Australia’s narrow commodity-based international economy.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.