S&P Global Ratings has warned again on Australia’s record high household debt:

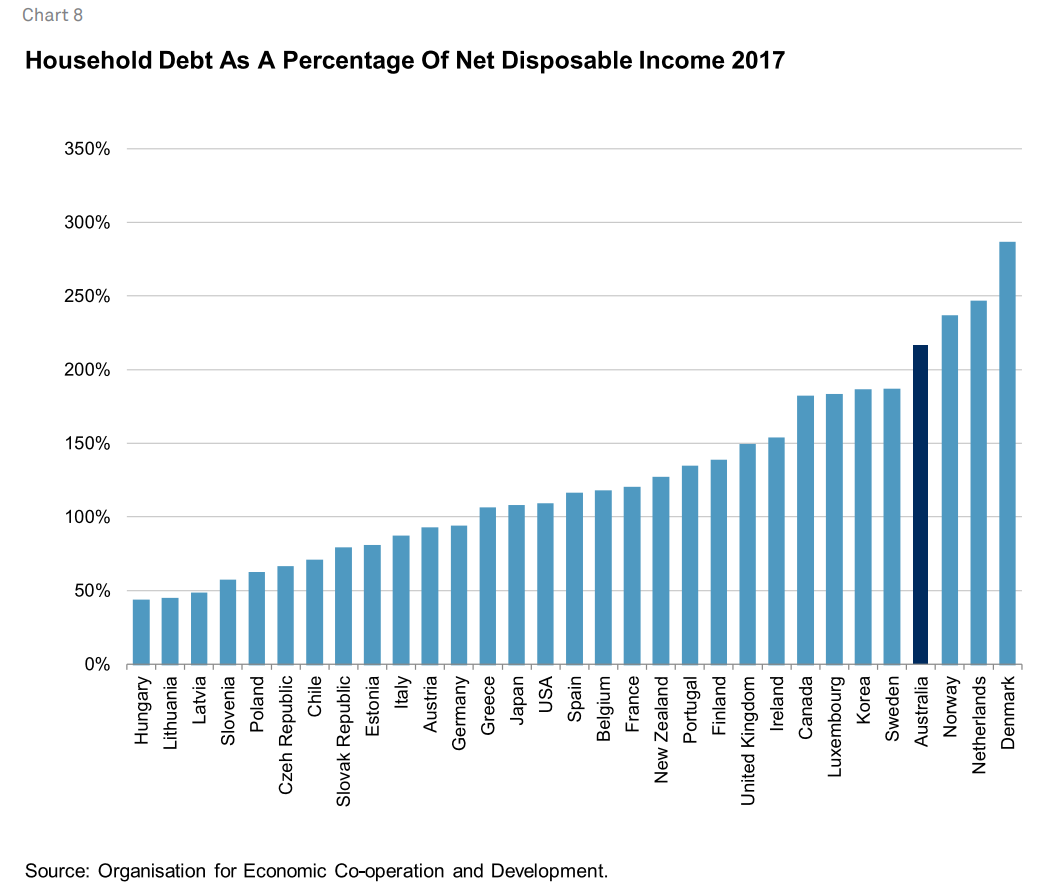

Household debt as a percentage of net household disposable income in Australia is high compared with many other Organization for Economic Cooperation and Development (OECD) countries (chart 8).

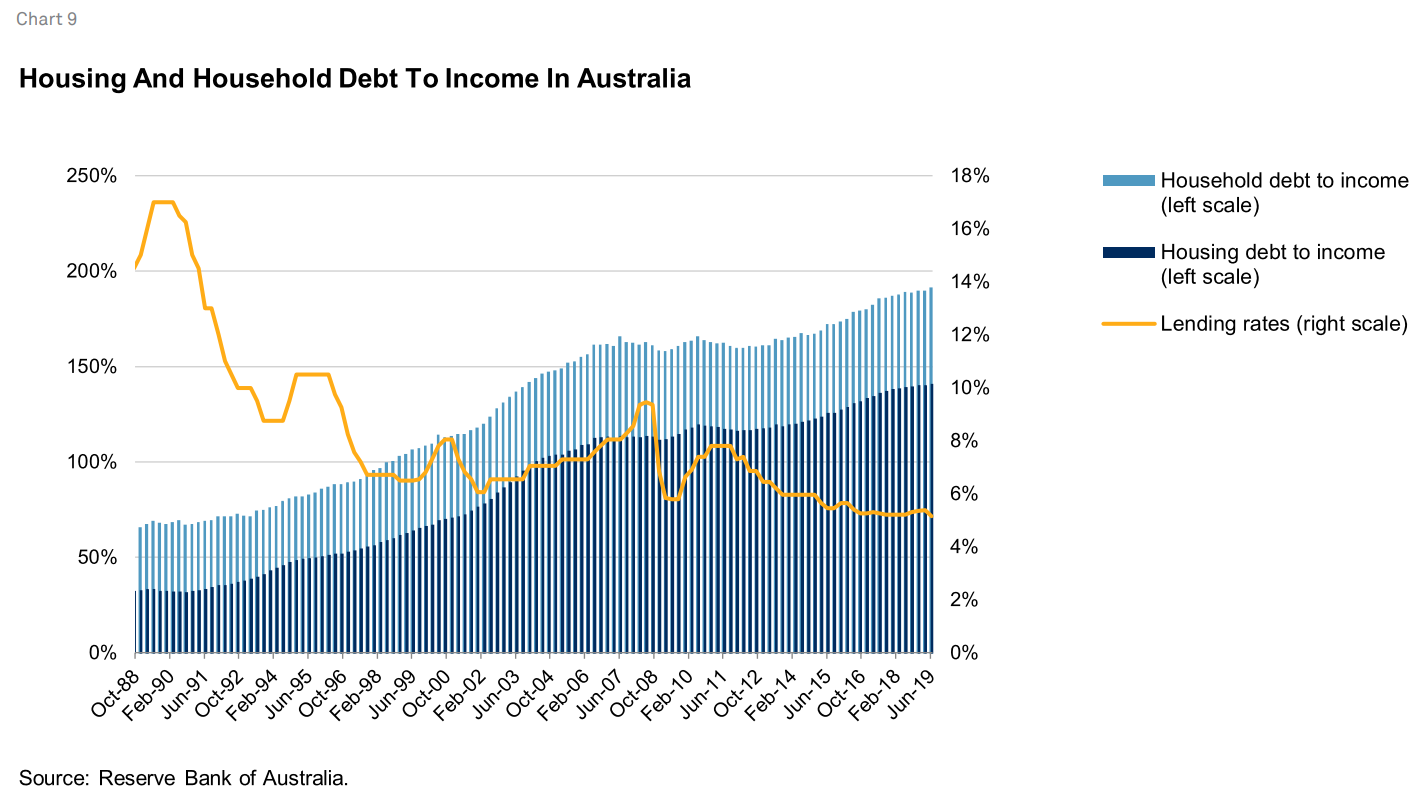

Australia’s household debt did not increase dramatically until interest rates and inflation reached low levels in the 1990s, improving consumer confidence (chart 9).

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.