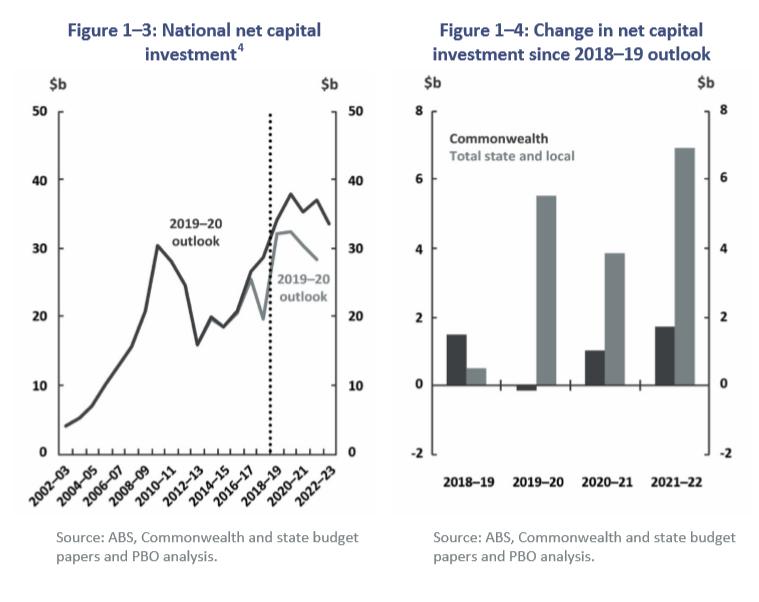

The Parliamentary Budget Office (PBO) has forecast that Australia’s net infrastructure investment will peak at $38 billion in 2019-20, before falling over the next three years. This is primarily due to expectations that the net debt of the state governments will blow out to around $156 billion by 2022, which would constitute the states’ highest share of public debt in two decades:

The level of national net infrastructure investment, as measured by net capital investment, is at record levels and higher than those during the post-GFC stimulus. Infrastructure investment has been revised up by a total of $20.9 billion for the period 2018–19 to 2021–22, largely due to an upward revision in state and local net capital investment of $16.8 billion (Figures 1–3, 1–4). Net investment in infrastructure is projected to peak at $37.9 billion in 2019–20. As a share of GDP, national net capital investment is projected to reach levels just below those recorded during the GFC stimulus period.

The substantial increase in state net capital investment is largely driven by New South Wales and Victoria, whose net capital investment for the period has been revised upwards by $7.8 billion and $6.5 billion respectively. These increases reflect significant investment in public transport, roads, health and education…

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.