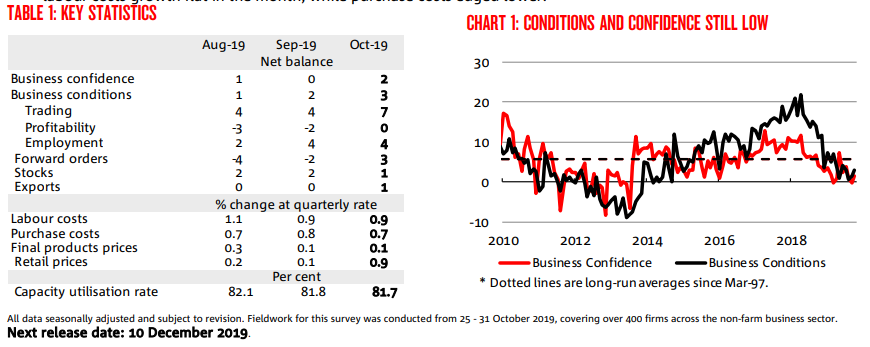

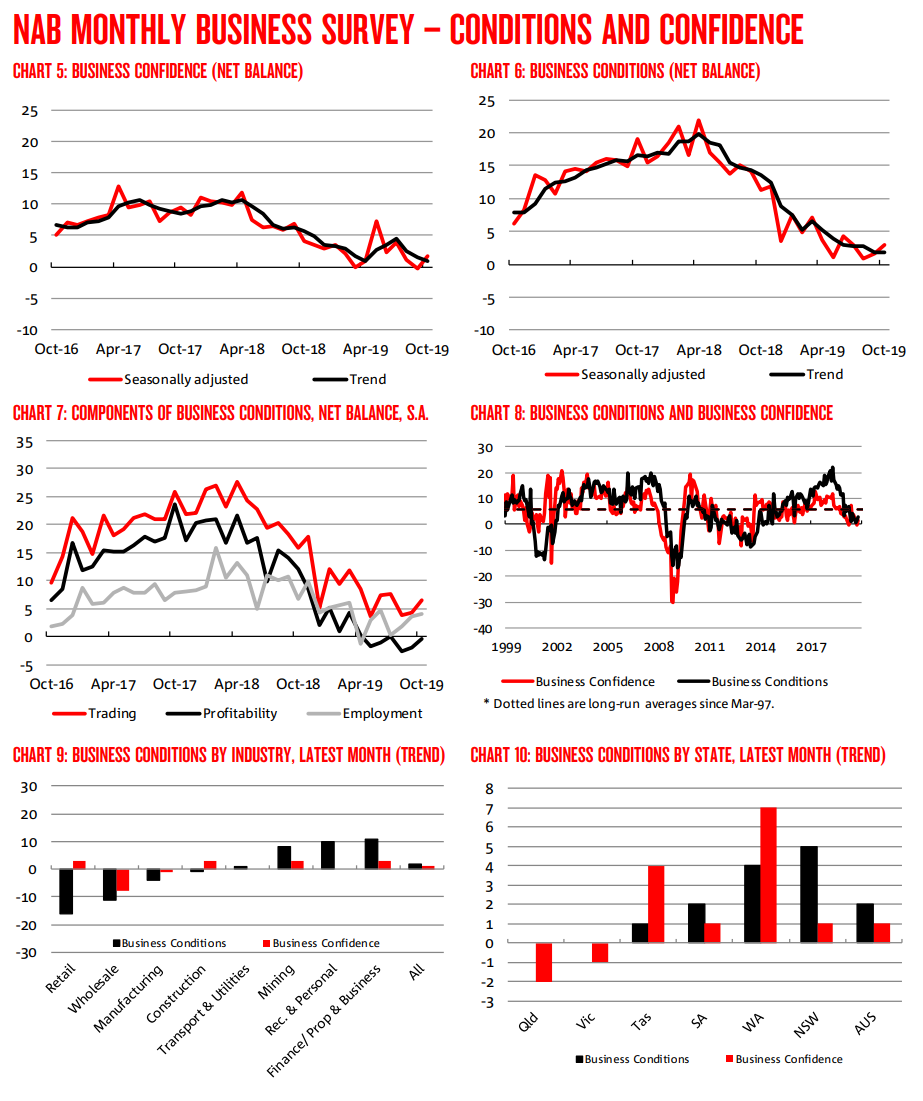

Key messages from the Survey: This month’s survey results continue to point to only modest outcomes in the business sector, though forward-looking indicators have improved slightly and may be pointing to a stabilisation in conditions. Conditions and confidence each saw a small improvement in the month with conditions edging up 1pt and confidence lifting 2pts – though both remain below average. The improvement in conditions was driven by an uptick in trading and profitability with the employment index flat. Ongoing reads of below-average trading conditions and profitability, will likely put at risk the continued strength in the employment component. In trend terms, the strength in mining appears to have faded over recent months, and the services sectors now see the best conditions. Retail and wholesale remain weakest. By state, NSW currently sees the best conditions while QLD and Vic are weakest. Inflationary pressure remains weak, with final products prices still growing at a low rate – notwithstanding a pick-up in retail price growth in the month and input price growth tracking at a higher pace. Overall, our read is that the survey continues to point to weak outcomes in the private sector, and that business’ own outlook is for more of the same. Acknowledging that the impact of recent rate cuts will take time to flow through the economy, it appears that the support provided by both fiscal and monetary policy this year has done little to offset the slowdown in the business sector.

Some kind of bottoming out is inevidence:

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.