1. The bulls are back…global recession concerns vanish and “Fear of Missing Out” prompts wave of optimism and jump in exposure to equities & cyclicals.

2. We say…easy part of rally over, tougher part of rally beginning…but rally it can as no “excess greed” (BofAML Bull & Bear Indicator @ 3.8), there is “excess liquidity” (and trade/fiscal easing), and corporate earnings set to accelerate.

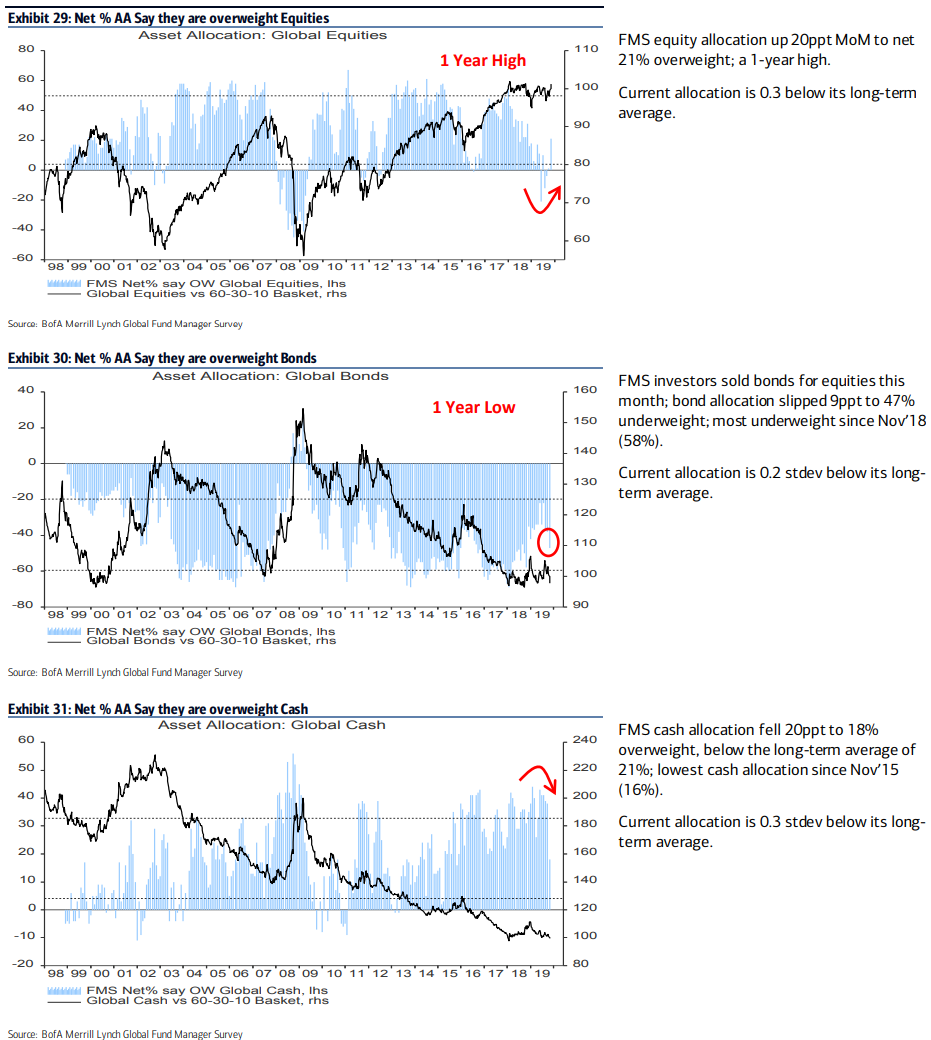

3. FMS cash levels slashed from 5.0% to 4.2% (biggest monthly drop in cash since Nov’16 Trump election); cash levels now lowest since Jun’13.

4. FMS global growth optimism surges by most in 20 years to 18-month high…implies global PMI to 53-55, global EPS to 3-5%; 1st time in a year investors want more companies to increase capex than reduce debt/improve balance sheet.

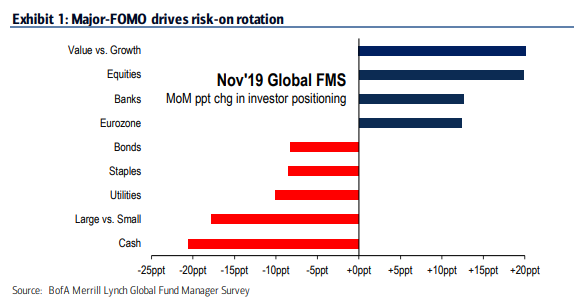

5. FMS expectations for steeper yield curve highest since Nov’16, US$ outlook weakest since Sept’07; investors raised S&P500 “peak” target from 3166 to 3246, and bought value/banks/Eurozone, sold cash/bonds/utilities/staples (Chart 1).

6. The bull surprise: investors still say “trade war” #1 tail risk…“trade truce” can boost exposure to stocks/cyclicals further (play via contrarian FMS bull trade “long energy-short REITs”)The bull surprise: investors still say “trade war” #1 tail risk…“trade truce” can boost exposure to stocks/cyclicals further (via contrarian FMS bull trade “long energy-short REITs”).

7. The bear surprises: 84% say Fed won’t raise rates before 2020 US election so hawkish Fed could unwind stubborn long positions in US tech/growth & Treasuries; 52% say stocks best performing asset class in 2020 (21% say commodities)…other bear surprise is stocks, PMIs, EPS all top very early next year.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.