China’s central government has issued new bond quotas for 2020 to some provincial-level governments early, as the state seeks to fund infrastructure construction in a bid to shore up a flagging economy.

Several financial officials in provincial-level governments told Caixin they have already received next year’s quotas of so-called special-purpose bonds from the finance ministry. Special-purpose bonds are designated for investment in infrastructure and public livelihood projects, and should be repaid from income generated by those projects, not from local budgets.

Bond selling by local governments has accelerated this year as the national economy faces downward pressure due to low demand and a trade war with the United States. Local governments almost used up their bond quotas for 2019 in the first nine months, and the State Council — China’s cabinet — has asked them to submit documents detailing how much debt they need to sell next year three months in advance.

Apart from bond selling, the State Council has decided to relax financing requirements for some infrastructure projects, cutting the minimum capital ratio requirement for ports and shipping infrastructure projects from 25% to 20% of the total investment.

However, infrastructure investment has not yet rebounded as expected. Government-driven infrastructure investment rose 4.2% year-on-year in the first 10 months of the year, down from 4.5% in the first nine months.

“This is a big decision, which means that the government is pretty worried about the downward pressure on the economy,” said Hua Changchun, analyst at Guotai Junan Securities.

“Currently speaking, the economy has not been effectively stabilized yet.”

Tang Jianwei, senior economist at Bank of Communications in Shanghai, said faster local government bond issuance could help underpin infrastructure investment, but he cautioned against any quick impact on the economy.

“Special bonds could help stabilize investment, but any impact may not be felt until the first quarter,” he said.

Advertisement

They should be. Real estate is still set to slow. And the deleveraging campaign casualties are mouting, at the FT:

Troubled banks have been able to secure only 20-40 per cent of the funds they have sought to raise in the interbank market for negotiable certificates of deposit, a vital source of funding for many smaller lenders, since the takeover of Baoshang Bank, according to research from UBS.

“They clearly have some liquidity issues,” said May Yan, UBS’s head of greater China financials equity research.

Some of China’s weakest banks have been forced to offer up the country’s highest yields on investment products, in a sign of desperation to raise funds.

Bank of Jinzhou, which received a partial bailout from ICBC in July, offers investors a 4.83 per cent return on wealth management products it sells, the highest rate in the country, according to data compiled by Rong360, an online financial services group.

Bank of Dandong, which was hit by US sanctions for links to North Korea in 2017, will pay 4.43 per cent on wealth management products.

Bank of Dalian, which has been bailed out twice since 2015, offers up 4.29 per cent on investment products, putting it among the top 10 highest offerings on bank investment products.

“This means investors do not fully trust the government interventions,” said Alicia García-Herrero, chief Asia-Pacific economist at Natixis. “The market is saying there are serious doubts about these banks.”

Wiping out your profitability is no way to stabilise a bank. Previously via WSJ:

Advertisement

Over the weekend, China’s Harbin Bank said it was now under government control. That comes months after Chinese authorities seized control of another small lender, Baoshang Bank, and state institutions took stakes in a third, Bank of Jinzhou. Bank runs have erupted elsewhere. Several other lenders have yet to file 2018 annual reports, in another sign that the problems are more widespread. Here’s how China’s banking system works—and what’s going wrong.

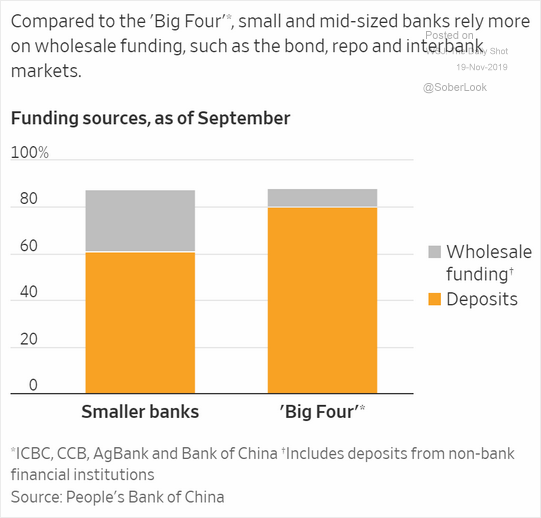

China’s banks come in various flavors. There are a handful of giants, and a few more medium-size banks that can also operate nationally. Below that lies a bigger cohort of city commercial banks, and more than a thousand tiny rural commercial lenders. Both city and rural banks have their roots in local credit unions, and tend to have limited geographic reach. Cracks are emerging at some small and midsize banks after years of rapid growth

Compared to the ‘Big Four’*, small and mid-sized banks rely more on wholesale funding, such as the bond,repo and interbank markets.

…smaller banks lent liberally to local governments and businesses, and bad debts are rising as China’s economy sputters. Poor governance probably created problems at some banks, too, such as Hengfeng Bank. In late 2017, the official Xinhua News Agency, citing a company statement, said Hengfeng Chairman Cai Guohua was being investigated for “alleged serious violation of discipline and law.”

There may be reassuring noises coming from regulators but seizing busted banks every few weeks is hardly that. Nor is this, also last week at CNBC:

China’s central bank unexpectedly trimmed a closely watched lending rate on Monday, the first such cut in more than four years and a signal to markets that policymakers are ready to act to prop up slowing growth.

The People’s Bank of China (PBOC) said on its website that it was lowering the seven-day reverse repurchase rate to 2.50% from 2.55%.

The move cheered China’s bond market and comes just two weeks after the PBOC cut the borrowing cost on its medium-term lending facility (MLF), used by banks for longer-dated funding needs, by the same margin.

Both cuts raise the likelihood that the PBOC will trim its new benchmark loan prime rate (LPR), off of which many lenders base their mortgage rates, this week in a bid to free up funds to credit-starved parts of the economy.

Analysts say the unexpected cut on Monday also shows the central bank is keen to ease investor worries that higher retail inflation would prevent it from delivering fresh stimulus.

Advertisement

Easing interbank funding is to support little banks. They are worried.

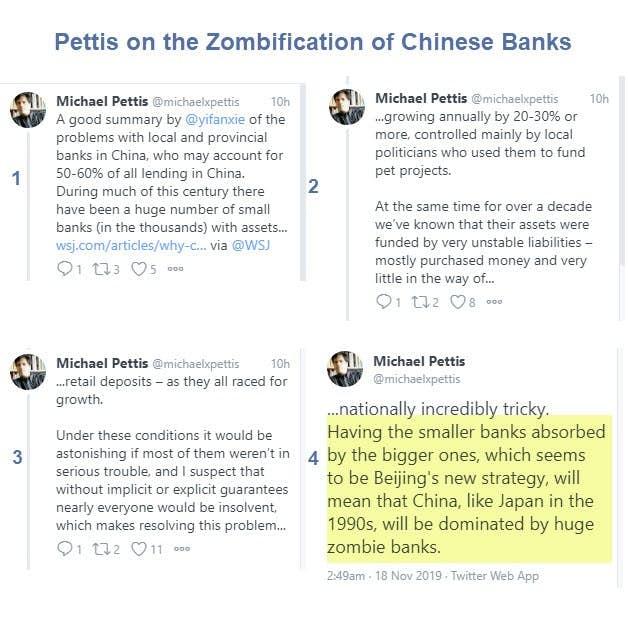

There is no crisis here yet. But the lower growth goes the worse this problem will get. The drover’s dog knows that the kind of credit growth these banks pursued is chock full of ponzi-borrowers and as growth slows so it becomes more difficult for diminishing cash flows to support over-leverage. The same old story. Via Michael Pettis:

Advertisement

In the long run the bankruptcies are good for the Chinese economy as it will lift capital productivity and incomes. But first it is the unmistakable signal that growth has seen its peaks and, as the bad loans come due, it will only keep falling.

In short, expect it to get much worse over the next five years. Maybe sooner!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.