By Chris Becker

US all the way on Friday night with Treasuries, the USD Index and Wall Street all advancing in tandem on the back of (spurious) claims by Trump that the US/China trade talks are advancing well – even though he later contradicted that in a Fox news rant. In Europe, new ECB President Lagarde made her first speech which gave European stocks a slight boost, even though the series of EU and UK flash PMIs disappointed as Brexit concerns continue to weigh.

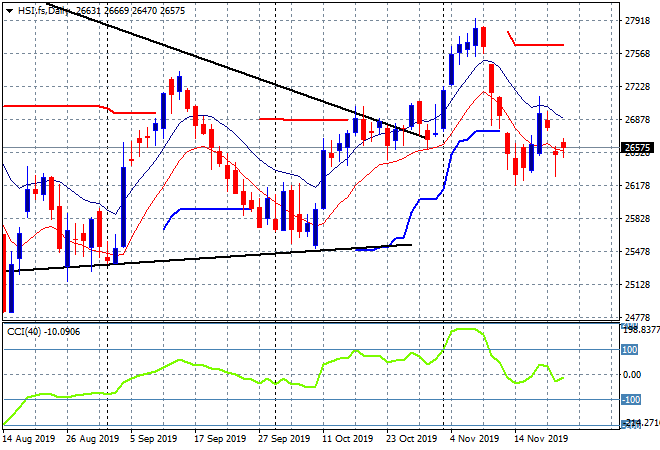

Looking at the action on Asian markets on Friday, where Chinese stocks really struggled, with the Shanghai Composite down nearly 0.7% to close well below 2900 points at 2886 after struggling all week to get back above that key level. In contrast, the Hang Seng Index found a modicum of buying support, closing nearly 0.5% higher to 26595 points. Price is still anchored below former trailing ATR support and the resistance zone at 27000 points so there’s nothing to get excited about here until price breaches the high moving average: