Weekend news of a possible resolution or movement of some kind in the US/China trade talks although the IMF is right to say this might be just domestic politics posturing as one country tries to stabilise internal struggle while the other tries to kick out a corrupt autocrat. Does it matter which? Gold fell again today as the USD continues to grow stronger, while Bitcoin revisited a monthly low, falling well below $7000.

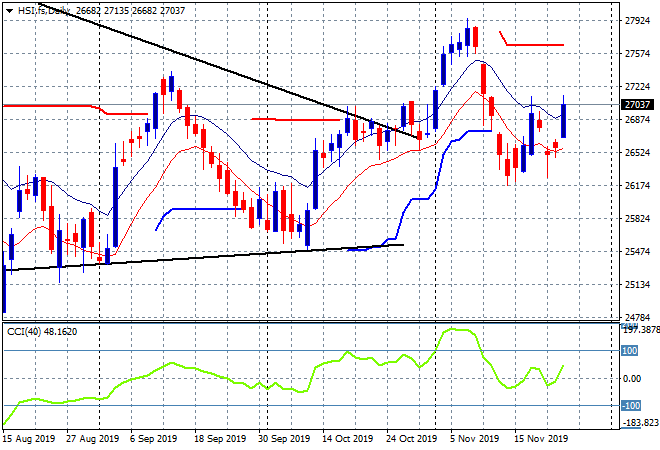

Chinese stocks are having a much better start to the week than anticipated, with the Shanghai Composite taking back its Friday losses to be up nearly 0.7% and back above the 2900 points resistance level. The Hang Seng Index is doing twice better due to the pro-democracy voting result from the weekend, launching 1.5% higher at 27028 points. This puts price but above previous trailing ATR support and test the resistance zone at 27000 proper, setting up for a potential breakout from here:

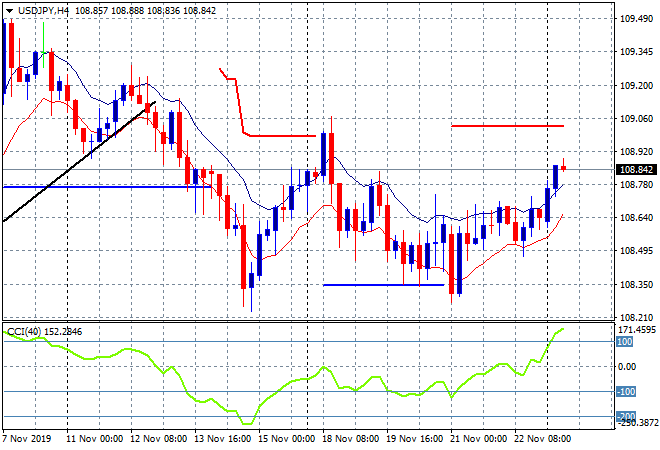

Japanese share markets also had a strong push, helped by a much weaker Yen with Nikkei 225 closing 0.7% higher to 23292 points, as it builds above daily support levels at 23000 points. The USDJPY pair gapped higher on the Monday morning open and then advanced further, making a significant breakout on the four hourly chart above the high moving average, now ready to tackle the 69 handle:

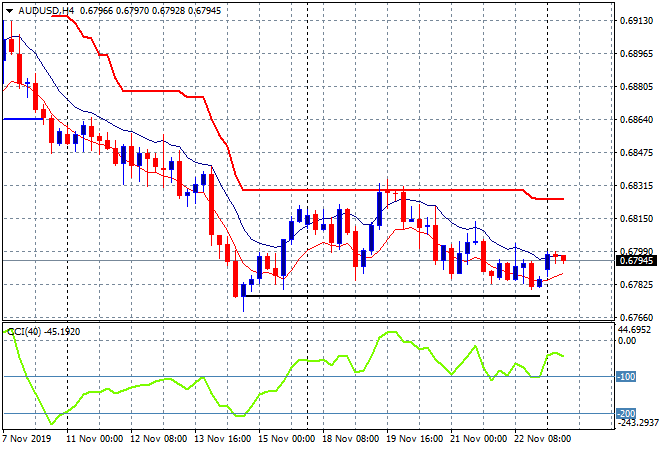

The ASX200 is the relative laggard, up only 0.3% to advance further past the 6700 points barrier, despite the banking sector concerns as Westpac lost ground again. The Aussie dollar gapped a little higher on the open but was unable to crack the 68 handle and is slowly melting from there as the City opens, where I still expect a test of last week’s extreme low at the 67.70 level:

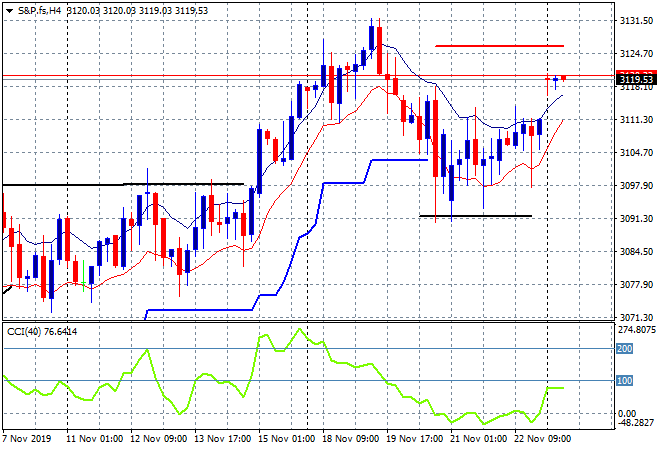

Both S&P and Eurostoxx futures have gapped higher, up at least 0.7% with the S&P500 four hourly chart showing price no longer anchored at the previous trailing ATR support level at 3100 points and ready to tackle the previous daily and record high of early last week at 3130 points:

The economic calendar is relatively quiet tonight with the German IFO survey and some US Treasury auctions to watch out for.