Another sea of red across Asian stock markets today following the same wave overnight on Wall Street, despite the Chinese trying to shore up optimism that trade talks won’t stumble and fall into the 2020 calendar year. Moody’s downgrade of the Australian state budgets weighed locally with the Australian dollar struggling to get back above 68 cents while the PBOC cut the Yuan substantially in its fix, sending offshore Yuan to a new weekly high above 7.04 against USD.

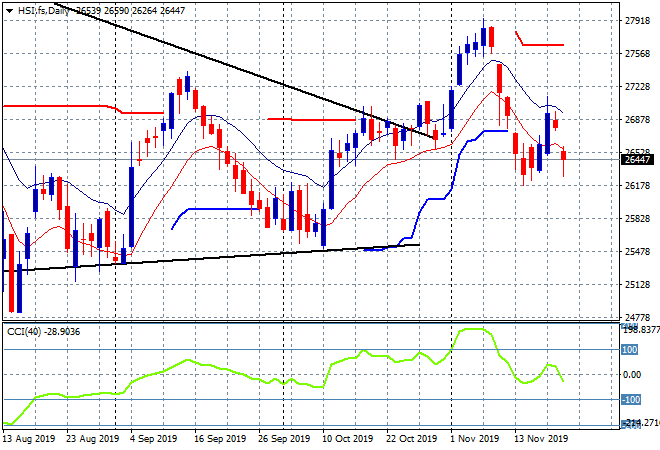

Chinese stocks are really struggling here, although on the mainland that Yuan cut saved some ground for the Shanghai Composite which only fell 0.25% to be just above 2900 points while the Hang Seng Index fell straight out of bed to match the previous daily lows, falling 1.6% to be at 26456 points. Price is rejecting former trailing ATR support and the resistance zone at 27000 points as momentum builds to the negative side:

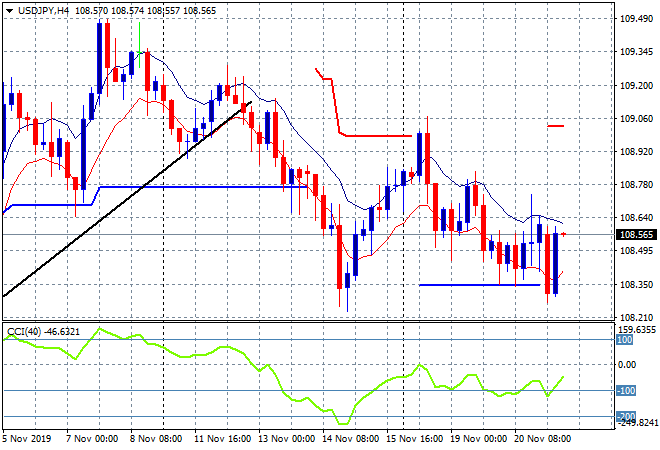

Japanese share markets were again swayed by the volatility in Yen both overnight and throughout the session as the Nikkei 225 lost ground and closed 0.5% lower to 23038 points, despite a late rally in the USDJPY pair. Yen buyers swapped their positions later in the session after breaking down to last week’s intrasession low in a potential sign that there maybe a bottom here after all:

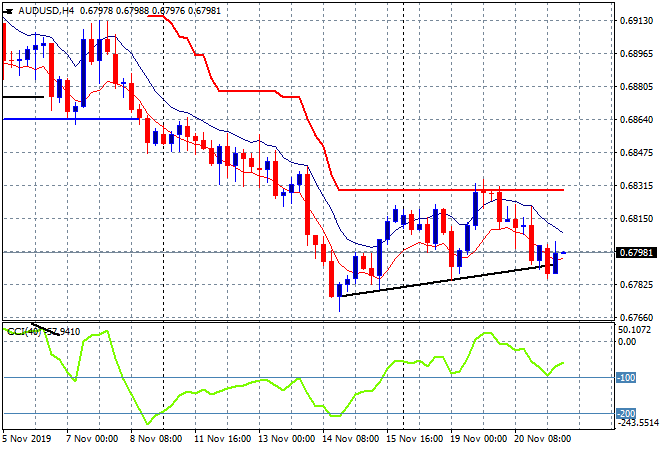

The ASX200 is now in full selling mode, losing another 0.7% to fall to 6672 points after recently breaking the medium term trendline on the daily chart. The Aussie dollar was relatively stable given the Moody’s downgrade, helped by some noise that Morgan Stanley is looking to buy more of the Pacific Peso. In the short term however, price looks like testing last week’s extreme low at the 67.70 level:

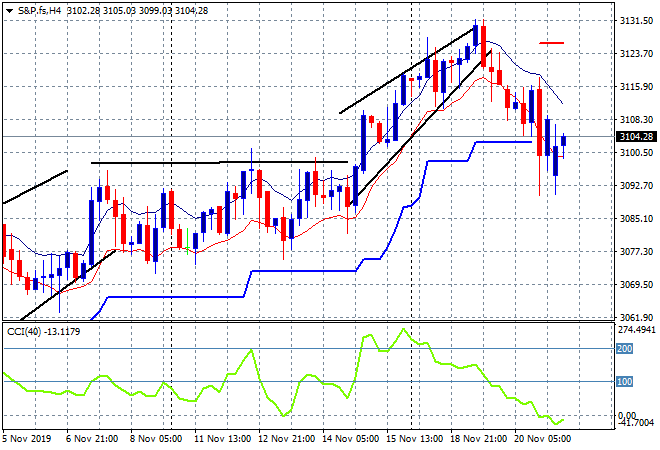

Both S&P and Eurostoxx futures are up slightly despite the lag in Asian shares with the S&P500 four hourly chart showing price anchored at the previous trailing ATR support level at 3100 points:

The economic calendar includes more ECB wonkery tonight, with the release of the OECD outlook, another official speech plus the releases of the October minutes. In the US its initial jobless claims night.