The mixed session from overnight markets has seen an equally mixed result here across Asia as tensions in Hong Kong remain high, while tech stocks and a softer Yen are lifting risk appetites only in Japan. The USD continues to firm against most of the majors, in particular Kiwi as traders await tomorrow mornings RBNZ meeting that could result in another rate cut.

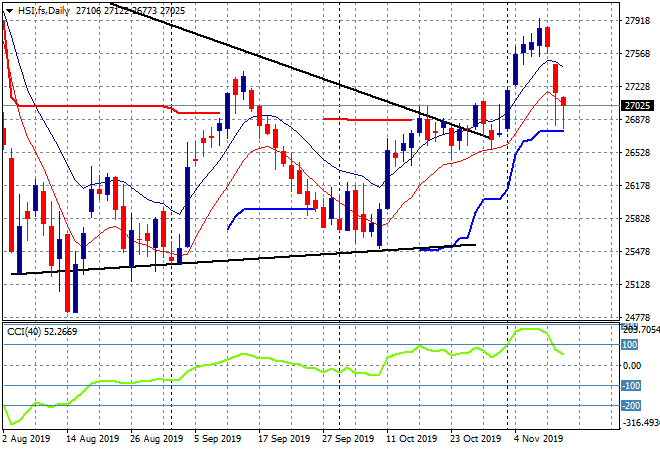

Chinese stocks have trying to rally after the previous wipeout with the Shanghai Composite holding on to a meagre 0.1% gain into the close, still just above 2900 points while the Hang Seng Index is bouncing back after a poor session, up 0.3% to 27025 points staving off a new daily low. Note how price is just bouncing off of trailing ATR support which equates to the previous support/resistance zone that was cleared before this blowoff rally started

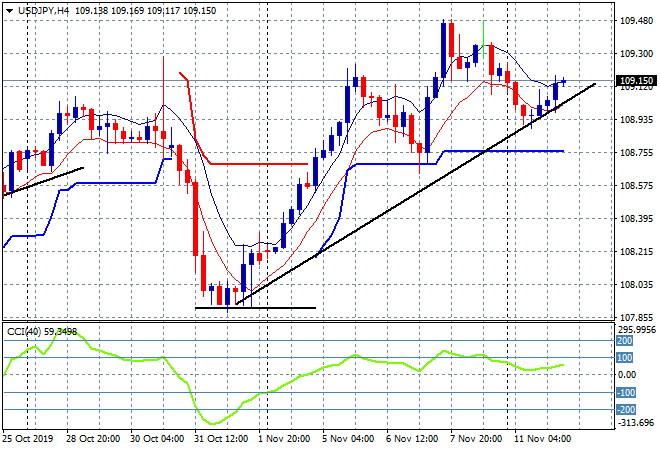

Japanese share markets are doing well enough however with the Nikkei 225 firming to close 0.8% higher to 23520 points. This is due to steady Yen selling after a small retracement by the previously well overbought USDJPY pair to just below the 109 handle as momentum kicks up again and the trendline from the late October low remains intact:

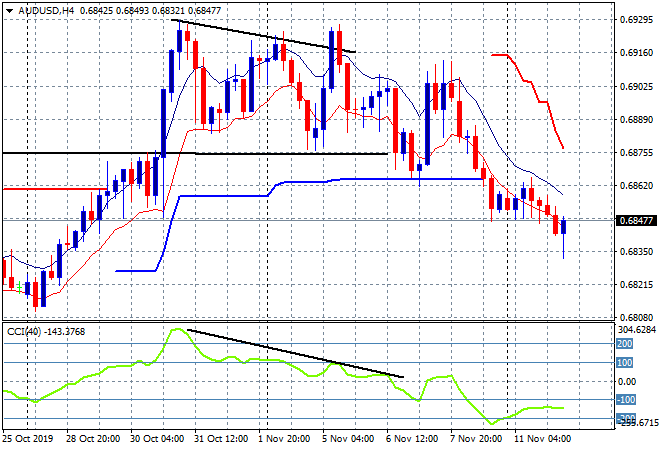

The ASX200 slipped to take back half of the previous gains, down 0.3% to 6752 points, lead by WBC which dropped nearly 4% in the session, dragging the other banks with it. The lower Aussie dollar hasn’t helped this time, with the Pacific Peso struggling to get any traction as it remains under pressure near the mid 68’s:

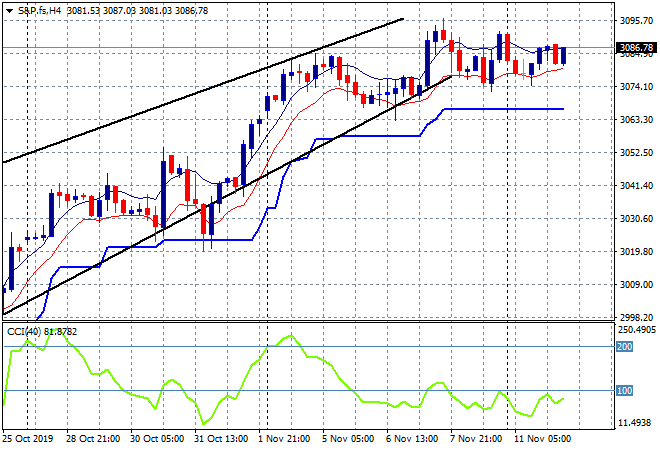

Both S&P and Eurostoxx futures are firming slightly with the S&P500 four hourly chart showing price holding on well above trailing ATR support, but not yet making a new session high since Thursday last week as momentum remains poised:

The economic calendar continues to be Euro-centric with the latest Euro-wide ZEW survey to watch out for.