Outside of Australia, stock markets here in Asia are bursting in hope and optimism, with new record highs from Wall Street overnight translating into big gains across the region. Japanese stocks were the highest, led by a big selloff in safe haven Yen, while today’s RBA meeting has translated into a big lift in Aussie dollar, now back above 69 cents against USD.

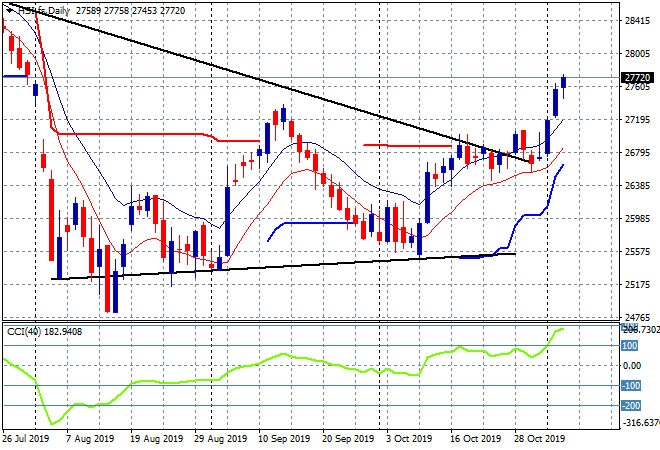

In mainland China, the Shanghai Composite has finally cracked the 3000 point level by lifting nearly 1% to 3005, while the Hang Seng Index is lagging but still performing well, up 0.7% to 27717 points going into the close. Having cleared the 27000 point level, and the weekly downtrend line last week, its plain sailing here:

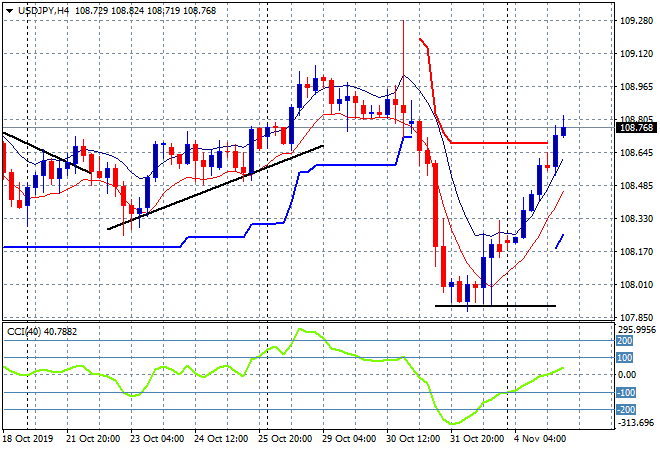

Japanese share markets reopened from their long weekend playing catchup and then some, with the Nikkei 225 leaping nearly 2% higher to close at 23299 points. This was mainly due to a surge in Yen selling, sending the USDJPY pair back to its mid point of control from last week before the NFP selloff, turning this swing play into a possible new trend as the 109 handle approaches:

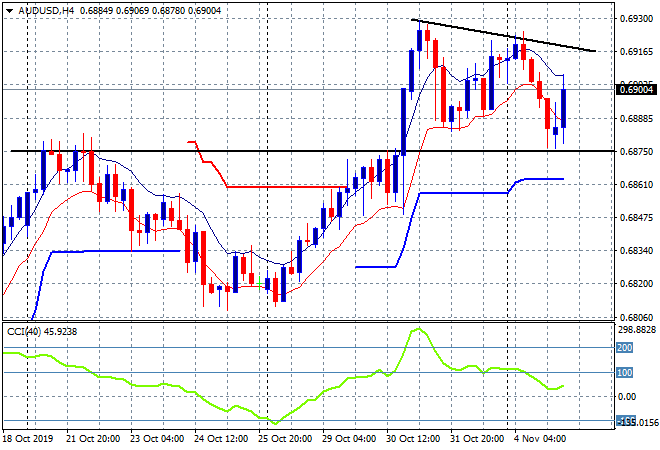

The ASX200 is the wet blanket, barely eking out any gains, by closing only 0.15% higher to just below 6700 points, as traders would rather put a punt on the ponies. The Aussie dollar lifted up to and just above the 69 handle on the latest but quiet hold from the RBA, bouncing off weekly support at the 68.75 level:

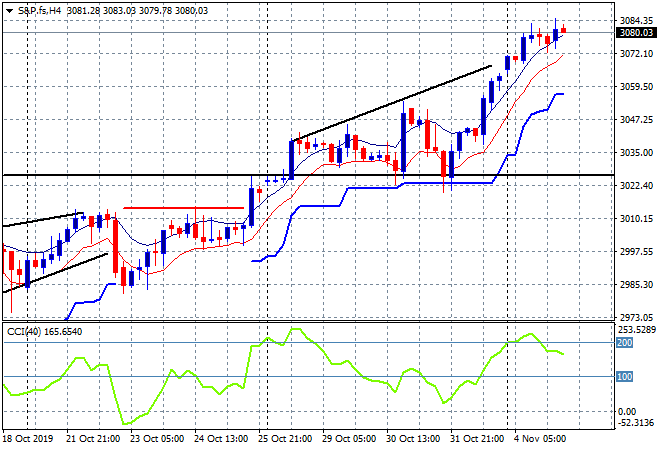

Both S&P and Eurostoxx futures are up slightly with the S&P500 four hourly chart still showing a stretched overshoot as the record highs pile up on each other, but I’m wary of another bearish rising wedge forming here, using ATR support as an uncle point would prove prudent:

The economic calendar tonight is relatively quiet, with the main focus being the September trade balance numbers for the US later in the session.