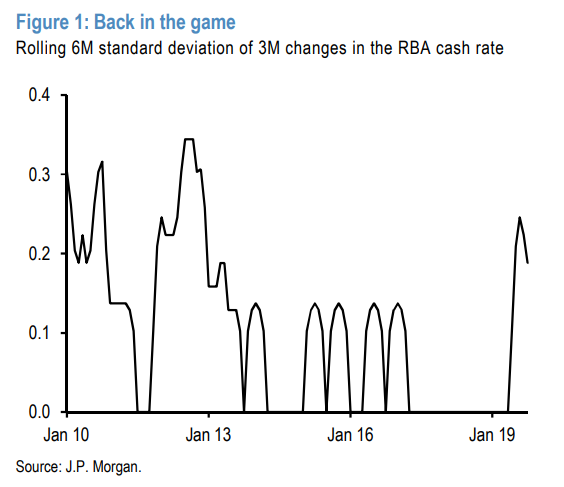

After a few years of policy stability, 2019 delivered plenty of surprises on the monetary policy front. First was the RBA’s volte-face in February, when the Governor declared that risks to Australian monetary policy had become two-sided. This was followed by consecutive 25bp rate cuts in June and July (the first time the RBA had delivered back-to-back easings since 2012), and then a further 25bp easing in October (the last time the RBA eased policy in the month of October was also 2012).

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.