With many of Australia’s capital city housing markets posting a gain in values over the past three months, a recovery trend is looking increasingly entrenched… but how long will it take for residential property values to reach a new record high if the current rate of growth continues?

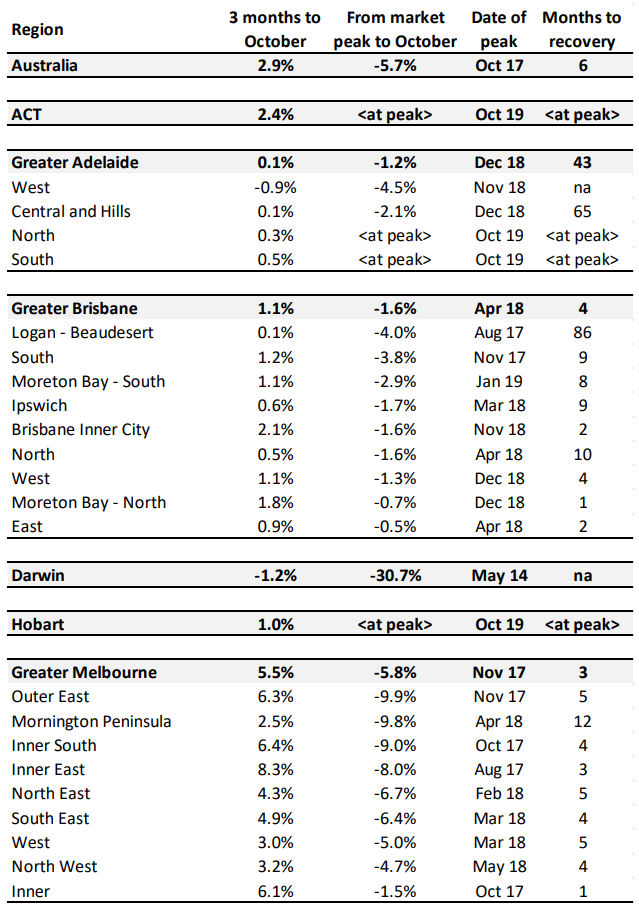

If housing values continue to rise at the same rate recorded over the past three months, national dwelling values could reach a new record high in six months time. Based on CoreLogic’s Home Value Index, national dwelling values remained 5.7% below their peak at the end of October. With values rising by 2.9% over the past three months (averaging a rise of just under 1% per month), it would take approximately 6 months for housing values to return to their historic high.

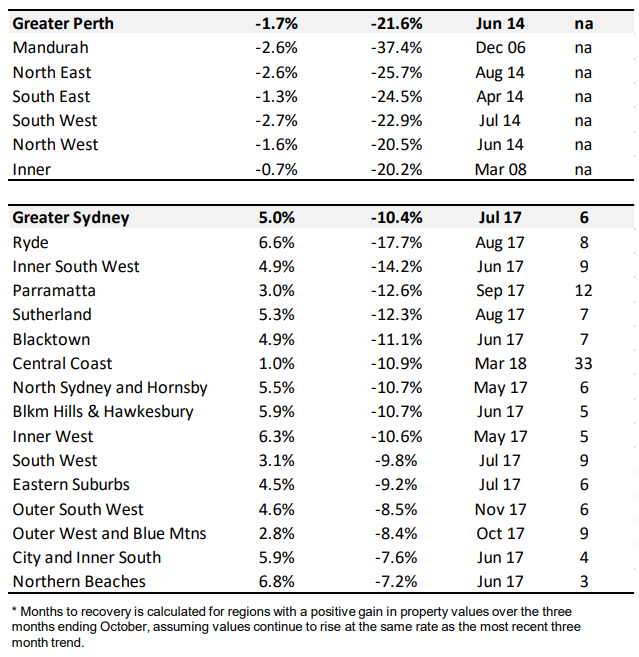

Most of Australia’s capital cities have recorded a rise in dwelling values over the past three months, with the only exceptions being Perth and Darwin, where values have been trending lower since mid-2014. While values continue to reduce, housing affordability is continuing to improve and buying opportunities are becoming more plentiful.

The same can’t be said of Hobart and Canberra which are the two capitals where housing values are already at new record highs. Hobart values recorded only a mild correction of 1.3% from peak to trough, with the market reaching a new record high in October 2019. Similarly, Canberra housing values recorded a peak to trough decline of only 1.5% during the downturn, and moved through a new record high in September this year.

Across the remaining capital cities, Melbourne is on track to stage a full recovery the earliest. If the current run rate of growth continues, Melbourne’s housing market will recover in January. During the correction, Melbourne housing values fell by 11.1% from peak to trough and remained 5.8% below their peak in October. Dwelling values across Melbourne’s Inner precinct were only 1.5% below their peak in October, and this subregion is on track set a new valuation benchmark by the end of November; the earliest of any of Melbourne’s sub-regions. Despite the earlier recovery period across the Inner precinct of Melbourne, the prestigious Inner East is recording the fastest rate of growth, with values up 8.3% over the past three months and on track for a recovery within three months.

Brisbane is showing the next fastest recovery time frame; not because values are rising rapidly, but mostly because the correction in values across Brisbane was quite shallow (down 2.9% from peak to trough). The past three months of gains (+1.1% or 0.4% per month) has put Brisbane housing values on a path to recover within the next 4 months.

Sydney’s housing market is on track to post a recovery within six months, or around April next year if the current pace of growth continues. Housing values are trending higher rapidly, up 5.0% over the past three months, however the correction was more substantial across Sydney, with housing values falling by 14.9% from peak to trough. Sydney dwelling values remained 10.4% below their 2017 peak at the end of last month.

The recovery trajectory in Adelaide is looking more drawn out, with values rising at the quarterly rate of only 0.1%. Although housing values are down only 1.2% since peaking, such a sluggish rate of appreciation is likely to see a prolonged recovery phase. Despite what looks to be a long recovery period, two of Adelaide’s sub-regions have already reached new record housing values. Both the North and South of Adelaide posted a new record high for housing values in October this year.

A recovery in the housing market should help to provide some support for Australian economic conditions, boosting household wealth which will potentially lead to improved confidence and a greater willingness from households to spend, while also supporting the residential building and development sector where dwelling approvals have tanked.

On the flipside, for non-home owners, a recovery in housing values implies the affordability dividends provided by the recent housing downturn are now a thing of the past. With housing values rising rapidly in some areas, we could see less first home buyer participation in the market as affordability pressures start to dampen activity across this important sector of the market.