Via Damien Boey at Credit Suisse:

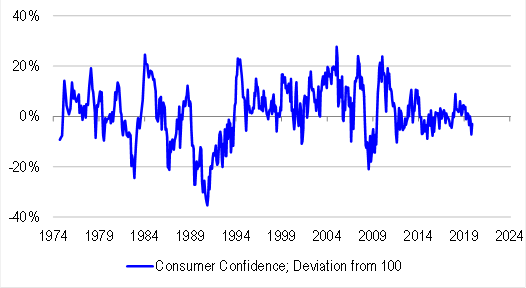

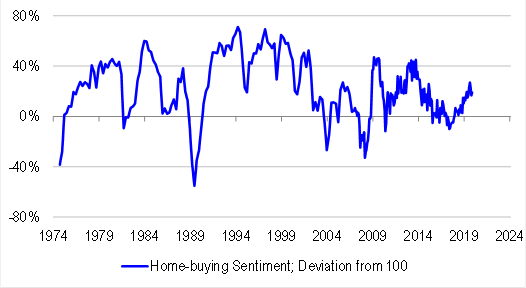

The Westpac consumer confidence report for November registered more improvement. After 3 rate cuts, tax cuts, the announcement of first home-buying incentives, and credit easing, consumer confidence was looking particularly dire by October, falling well below neutral levels. It looked very much like consumers were responding to the bad news behind easing measures, rather than the stimulus itself. But in November, consumer confidence recovered to 97 from 92.8 – still below neutral levels, but considerably less so. Home-buying sentiment also improved to 119 from 116.6.