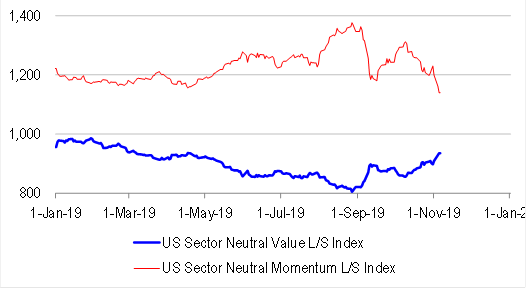

Value rotation continued in earnest overnight, with sector-neutral value factors adding 0.7%, while momentum factors detracted 1.9%, and low-beta factors lost 0.5%. The value index is back to its mid-April highs, while the momentum index is now materially down year-to-date, having experienced stellar performance through the middle of the year. The reversal of fortunes in factor land has been dramatic.

In fixed income, US 10-year bonds sold off further by 8bps to 1.86%, and the yield curve steepened. Bond market investors were further spooked by reports that US President Trump is considering lifting existing tariffs for the purposes of achieving phase I of the trade deal with China. But beyond the newsflow, we are witnessing an extraordinary re-positioning away from long duration assets among commodity trading accounts (CTAs).

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.