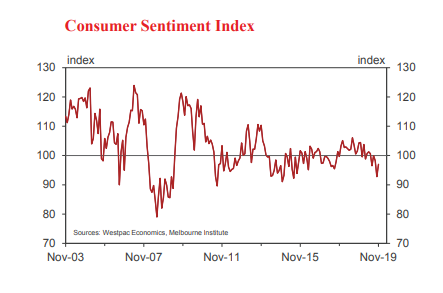

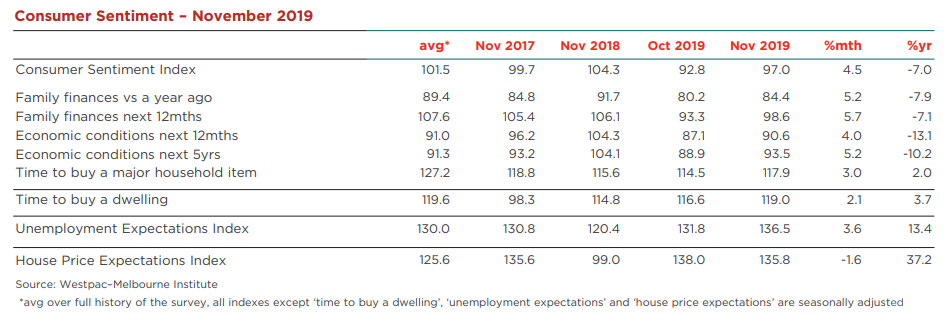

The Westpac-Melbourne Institute Index of Consumer Sentiment rose 4.5% to 97.0 in November from 92.8 in October.

This rise in the Index follows a sharp 5.5% fall in October. The pattern of confidence falling in response to a rate cut and recovering when the RBA remains on hold repeats what we saw earlier in the year when the Index fell by 4.1% following the July cash rate cut only to recover 3.6% in August, when the RBA left rates unchanged.

This result continues to support the general view that consumers are somewhat unnerved by the announcement of low rates and media controversy around the banks’ responses.

Note that looking through month to month volatility the Index has fallen by around 4% since the RBA started cutting the cash rate in June and has been below the 100 level, indicating pessimists outnumber optimists, for four of the last five months.

Other factors would have boosted Consumer Sentiment since the last survey. Markets have generally lifted, the ASX up 3.2% over the last month, boosted by a more positive tone around the global economy. The key here will be whether the US and China are able to reach a successful agreement around the trade disputes since markets are now likely to be already pricing in a satisfactory outcome to the current discussions.

Consumer spirits may also have been lifted by the extensive coverage given, during last week’s survey period, to the possibility of the Commonwealth Government bringing forward the personal income tax cuts legislated for July 2022, to July 2020.

All index components recorded a rise in November.

Consumer views on the economy improved but continue to show a more pronounced weakening in recent months. The ‘economy, next 5 years’ sub-index rose 5.2% in November and the ‘economy, next 12 months’ sub-index rose 4% but both retraced only part of last month’s declines (–9.1% and –6% respectively) and are down sharply on a year ago (–10.2% and –13.1% respectively).

Assessments of family finances have been more resilient over the last two months and slightly firmer overall. The ‘finances vs a year ago’ sub-index rose 5.2% in November and the ‘finances, next 12 months’ sub-index rose 5.7% – both flat to up slightly on September. That said, the gains remain disappointing given interest rate cuts, the $7.7bn in personal income tax relief rolled out since July and the turnaround in housing markets from price declines to robust price gains. Indeed, both sub-indexes remain at weak levels well below long run averages – a pattern that has been a persistent feature for several years now.

Consumer attitudes towards spending look to be downbeat heading into the all-important Christmas sales period. The ‘time to buy a major household item’ sub-index rose 3% in the November month but is still 4% below its August level. At 117.9, the sub-index is well below its long run average of 127, suggesting consumers will be keeping a tight rein on discretionary spending.

A restrained attitude towards spending is also evident in responses to our annual question on Christmas spending plans. One in three Australians are planning to spend less on gifts than they did last year, with a further 54% expecting to spend about the same. Just 11% of consumers are planning to spend more this year. The mix is almost identical to last year’s survey and suggests we are heading for another lacklustre Christmas spend.

The Westpac-Melbourne Institute Unemployment Expectations Index rose 3.6% to 136.5 in November, up 13.4% on this time last year and the highest reading since June 2017 (recall that higher readings indicate that more consumers expect unemployment to rise in the year ahead). The readings are consistent with a slowdown in jobs growth and steady increases in unemployment and underemployment rates over the year ahead.

Housing-related sentiment was relatively stable in November, views on time to buy improving slightly but price expectations showing signs of consolidating after the very strong gains in previous months.

The ‘time to buy a dwelling’ index rose 2.1% in November to 119, holding around its long run average of 120. Buyer sentiment continues to soften in NSW and Victoria where the resurgence in prices already looks to be squeezing affordability. Buyer sentiment remains relatively well supported in Queensland, WA and SA.

The Westpac-Melbourne Institute Index of House Price Expectations Index dipped 1.6% in November, the first decline since May but following a 54% surge between May and October. While consumer price expectations continued to strengthen in NSW (+7.3%) they cooled sharply in Queensland (–11.9%) and Victoria (–6.4%).

The Reserve Bank Board next meets on December 3. Westpac expects that the Bank will hold rates steady at that meeting. Recent publications from the Bank indicate that it is prepared to take more time to assess the impact of the three cuts we have already seen. However, the Board retains a clear easing bias and we expect it to act on this bias next February with a further 25bp rate cut.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.