Economic growth has slowed in Australia and elevated spare capacity means that the economy would benefit from more stimulus.

The RBA is approaching the lower bound, the Commonwealth Budget is in balance and net debt is low as a share of GDP-the case for an easing in fiscal policy grows stronger by the day.

Given the big lift in public demand over the past few years against the backdrop of weak growth in household disposable income and a material lift in the tax-to-income ratio, we believe the simplest, most efficient and most equitable way to boost aggregate demand from here is via personal income tax cuts.

Overview:

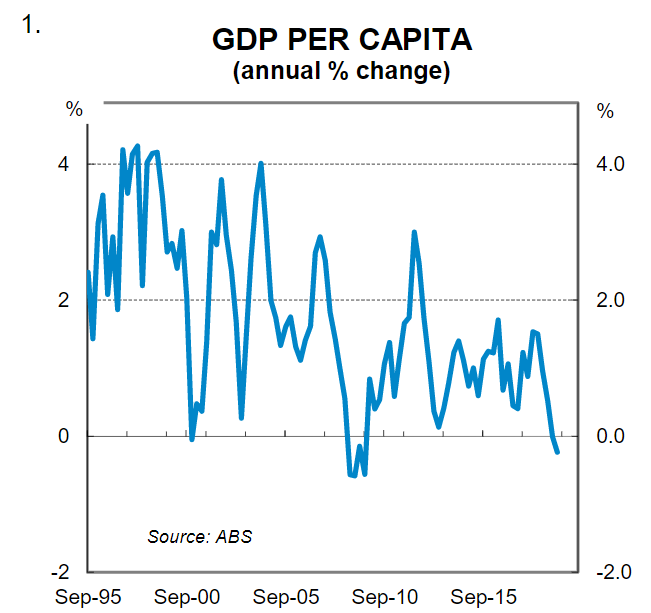

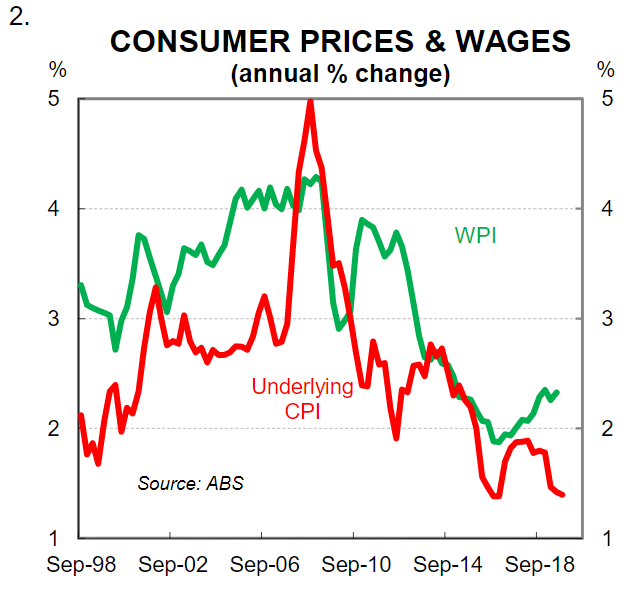

Growth in taxes paid by households is running well ahead of income at a time when economic growth is below potential and there is a plenty of spare capacity in the economy. Take out population growth and the Australian economy has not grown over the past year(chart 1).The by-product of an economy that is operating below its potential is weak wages growth and below-target inflation (chart 2).Indeed underlying inflation has been below the RBA’s target for 15 consecutive quarters.

It’s not all bad news, however, as the unemployment rate remains low in a historic context and there are still parts of the economy that are performing well. But it’s clear that the Australian economy would benefit in the short run from more stimulus and in the long run from some reforms aimed at boosting productivity. In this paper we focus on the former.

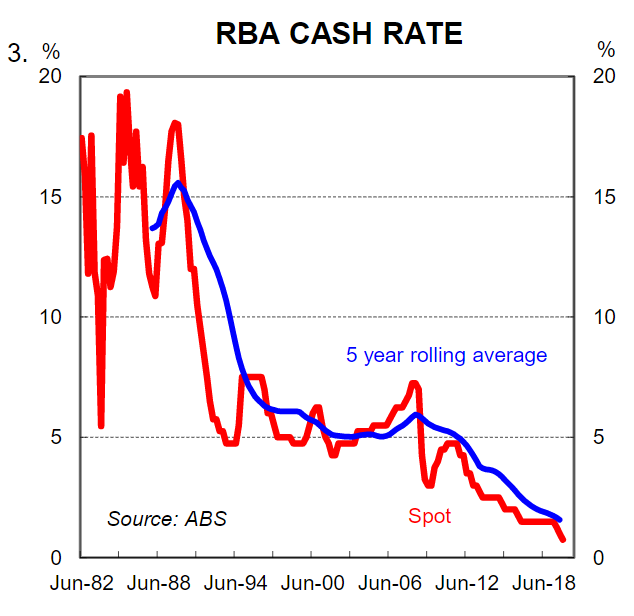

To date, the RBA has responded to the softening domestic economy in 2019 by delivering three 25bp interest rate cuts (chart 3). And more monetary policy easing is expected. Another 25bp cut to the cash rate is expected by us and financial markets(62% priced)which would take the policy rate to just 0.5% -most likely to be the level of the effective lower bound. This puts Australia in unchartered waters. Once the lower bound is reached it is not possible to further stimulate the economy via standard interest rate cuts. Any additional monetary policy stimulus would most likely take the form of Unconventional Monetary Policy (UMP): quantitative easing (i.e. asset purchase programmes), forward guidance and new central bank lending operations.

But UMP is only one option and comes with a number of potential negatives. There are a raft of other policy options available to stimulate aggregate demand. The other options generally fall under the umbrella of “fiscal policy” and include tax cuts, more infrastructure spending and more government recurrent expenditure. Monetary policy is already highly accommodative and we believe that at this point in the cycle there is both a need and desire for fiscal policy to play a greater role in boosting aggregate demand in the economy.

The old adage that a stich in time saves nine is very much applicable to policy changes that influence demand. The slowdown in both the global and domestic economies mean that there is merit in loosening fiscal policy sooner rather than later. There is a risk that fiscal stimulus is delayed and only deployed in the event of a further softening in the economy or an ‘emergency’. If that turns out to be the case, a greater fiscal stimulus will be required to boost demand to the desired level and the Government’s fiscal position will not be as strong as it is now (ie. a further softening in the domestic economy would hit the Government’s coffers).

In this note we discuss the merits of fiscal stimulus in the context of the current state of the Australian economy, the limitations of monetary policy and the objectives of the RBA.

What is the RBA trying to achieve?

The RBA’s mandate is to maintain price (currency) stability, full employment and the economic prosperity and welfare of the Australian people. To achieve this, the RBA has an inflation target (2%-3%pa over time). The primary way the RBA meets its inflation target is to maintain conditions in the money market so that the overnight cost of money is at or near an operating target decided by the RBA Board. This operating target is the official cash rate.

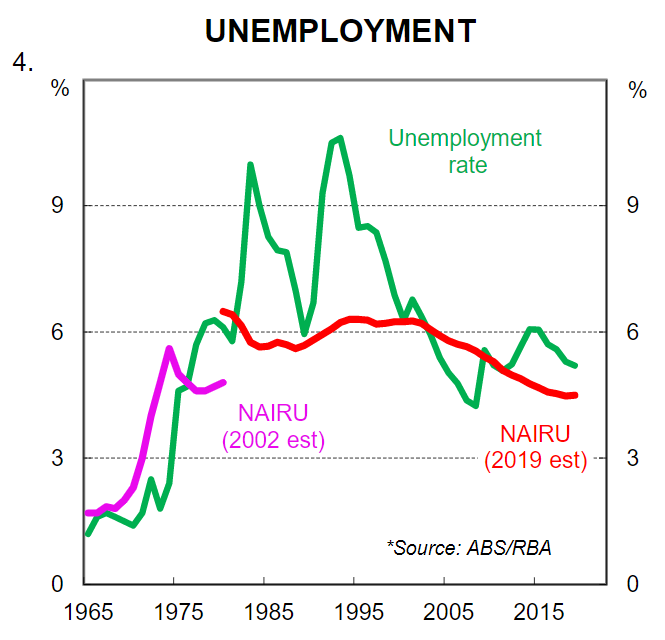

Earlier this year the RBA materially downwardly revised its estimate of the unemployment rate associated with full employment (otherwise known as the non-accelerating inflation rate of unemployment or simply the NAIRU).More specifically, the RBA downwardly revised its estimate of the NAIRU from 5% to 4½% (chart 4). Essentially the RBA believes that the unemployment rate will need to fall to 4½% if wages growth is going to lift in any material sense, which is a necessary condition for inflation to return to the 2-3% target band.

In order to achieve full employment the RBA has cut the cash rate by 25bpsthree times so far in 2019 (from 1.5% to 0.75%). As stated in the October Board Minutes, “members judged that lower interest rates would help reduce spare capacity in the economy by supporting employment and income growth and providing greater confidence that inflation would be consistent with the medium-term target”. Put simply, the RBA is trying to stimulate demand in the economy by lowering the cost of money. The desire is to see a higher rate of growth in household consumption and business investment, which would in turn lead to a lift in employment growth and a decline in the unemployment rate.

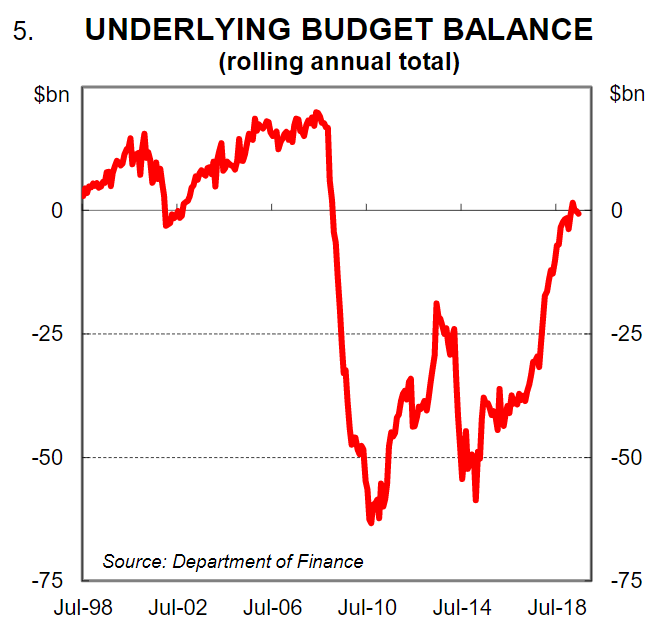

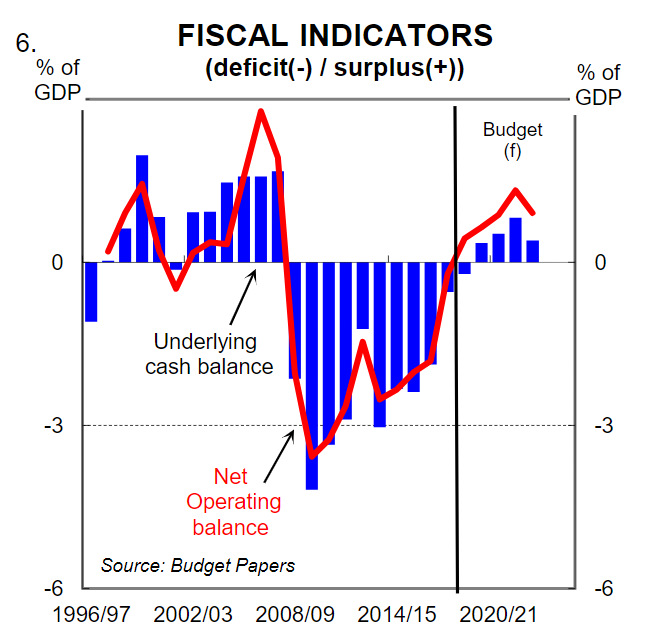

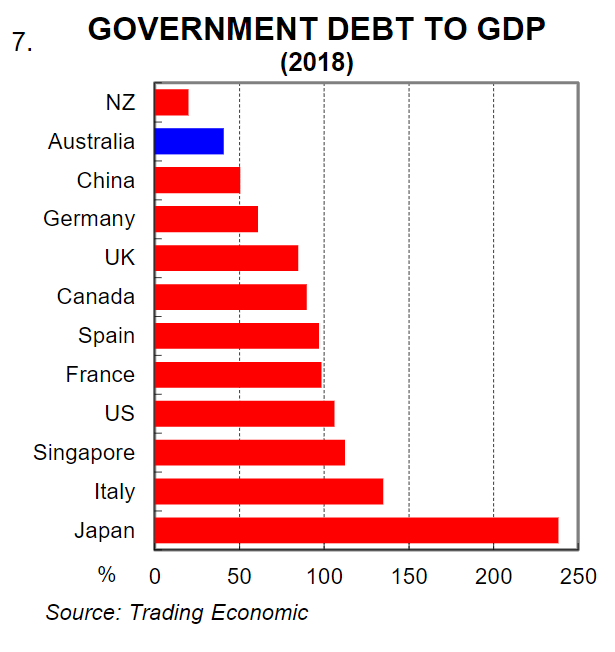

In our view, however, the interest rate cuts in isolation are not going to be enough to generate a sufficient lift in demand to see the unemployment rate fall to 4½%. As such, there is a growing risk that in an attempt to meet their objective, the RBA could resort to UMP if a conventional fiscal policy easing is not deployed. The jury is still out on the effectiveness of UMP. And there can be unintended consequences; which include potentially greater risks to financial stability as asset prices are artificially pushed up. In contrast, conventional fiscal policy has a proven track record of successfully influencing aggregate demand. Given Australia’s strong fiscal position, Triple-A credit rating and relatively low share of government debt to GDP, the case to ease fiscal policy rather than resort to unconventional monetary policy is strong (charts 5, 6 & 7).

The role of fiscal policy

Fiscal policy is essentially changing government spending (recurrent and investment) and taxation to influence aggregate demand.The stance of fiscal policy is deemed “contractionary” or “expansionary” by looking at the direction and size of the expected change in the budget balance. At present, the stance of fiscal policy adopted in the Federal budget is contractionary. Growth in taxation is greater than growth in expenditure, which is why the deficit has shrunk and the budget is now essentially balanced.

Whilst it is true that public spending has risen as a share of the economy and tax rebates totalling around $A7½ billion have been delivered to the household sector in2019/20, overall growth in revenue has been stronger than growth in expenditure. Shrinking the Commonwealth Budget deficit in this manner in pursuit of a surplus effectively sucks money out of the economy resulting in a contractionary impact on aggregate demand.

The stance of fiscal policy, however, does not need to stay contractionary. The purse strings can be loosened to provide support to the economy and complement monetary policy. There are essentially three options: (i) cut taxes (personal and/or business); (ii) increase recurrent expenditure; and (iii) increase public investment. To us, the recent trends in household disposable income, the tax-to-income ratio and government expenditure mean that the case for personal income tax cuts is stronger than the case for a further lift in recurrent expenditure and investment.

Why personal income tax cuts?

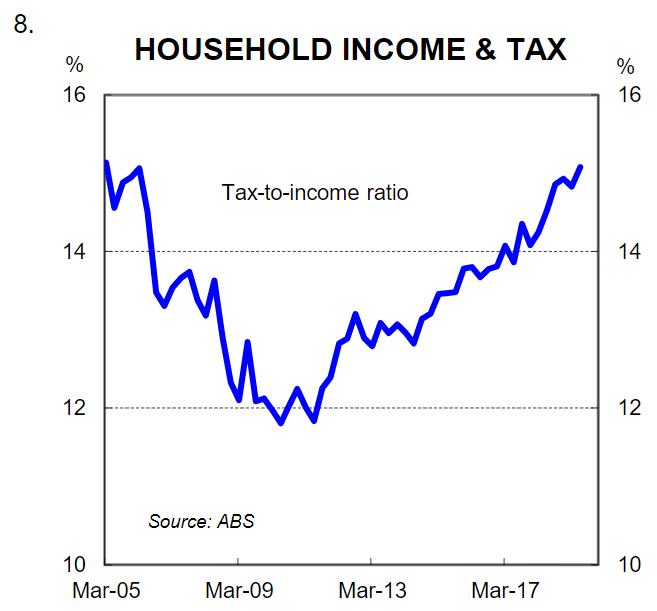

Australian workers haven’t had a tax cut in any material sense for years. Bracket creep means that workers are handing over an increasing proportion of their salaries each year to the tax office. As a result, the tax-to-income ratio has been on a solid uptrend over the past five years (chart 8). This has been weighing on growth in household disposable income and on the capacity for households to spend.

The Federal Government has implicitly recognised this and personal income tax cuts were a centre piece of the 2018/19 Budget. Unfortunately, however, the material tax cuts, which have been legislated and are structural, don’t kick in until 2022/23 and 2024/25.These later phases of the tax changes involve reducing the 32.5% marginal rate to 30%, removing the 37% threshold and increasing the 45% threshold. The tax cuts are estimated by the Federal Treasury to “cost” the Budget $A235bnover 10 years.

The cost to the Budget, however, may not nearly be as large. The Australian Treasury used a static tax model to estimate the cost of the tax cuts. But a static model assumes no change in consumer behaviour as a result of tax cuts. That is, it does not take into account any of the impacts that tax cuts would have on household disposable income, consumption or the incentive to work more. Put simply, none of the economic benefits of tax cuts are captured. In contrast, analysis by the Centre for Independent Studies indicates that applying a dynamic model to the tax cuts produces a cost to the Budget of $A145bn over 10 years which is $A95bn less than the Treasury estimate. The Budget could therefore comfortably absorb pulling the tax cuts forward to begin in 2020/21 (ie. 1 July 2020) and the benefit to households and the economy would be immediate.

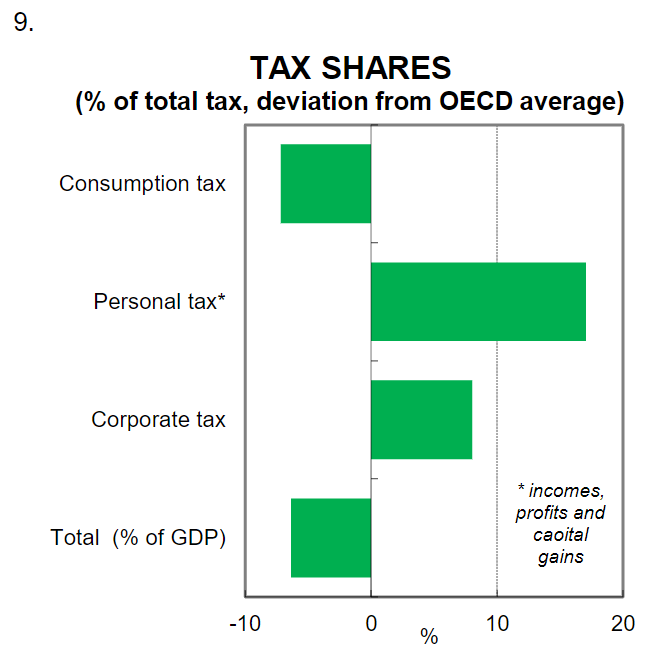

An international comparison also supports the case for personal income tax cuts. Relative to the OECD average, Australian tax collections are significantly “overweight” personal income tax and “underweight” consumption taxes (chart 9). This means that workers in Australia are shouldering a disproportionate tax burden relative to most other comparable nations. And that burden is being magnified each year through bracket creep. Business tax cuts are also a policy option. But basic economic theory suggests that investment generally follows demand. In other words, private investment is responsive to demand rather than supply creating demand. Therefore given consumer demand is weak, the objective should be to boost household expenditure to which businesses are likely to respond by lifting investment.

Why not more Government consumption expenditure?

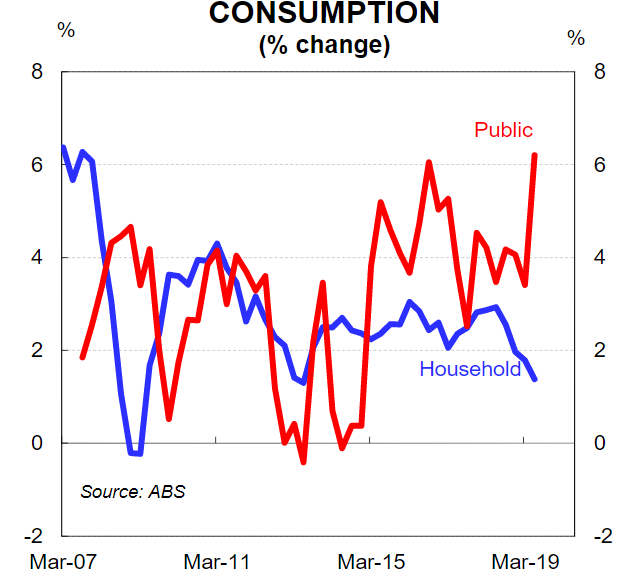

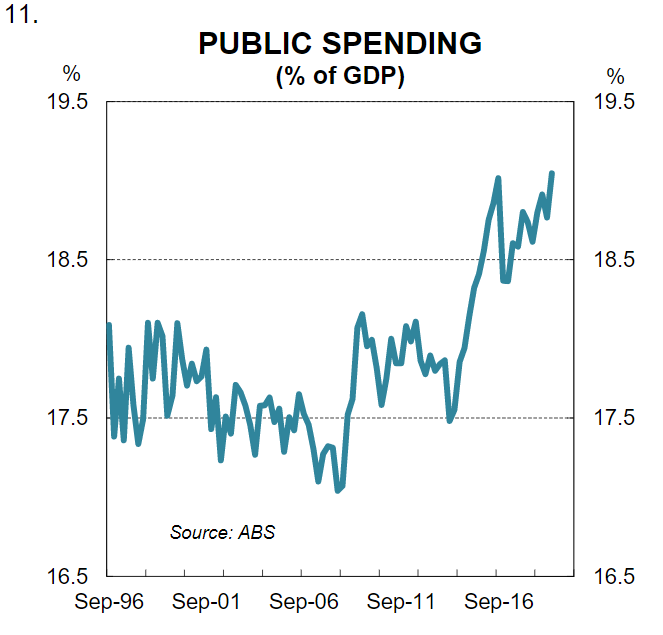

Fiscal policy can be eased through a lift in public recurrent expenditure. But total general government consumption1growth is already very strong. Indeed it has been significantly higher than household consumption growth over the past four years (chart 10). As a result, public consumption expenditure has risen materially as a share of GDP (chart 11).

Where has the money gone? The strong growth in public sector employment goes a big way to accounting for the growth in government consumption expenditure. Employment growth in the public sector has been phenomenal, particularly in government administration and safety employment. Against this backdrop, the economic case to ease fiscal policy via more government consumption spending rather than personal income tax cuts doesn’t stack up. Especially considering that the tax-to-income ratio has risen for four years.

What about more infrastructure spending?

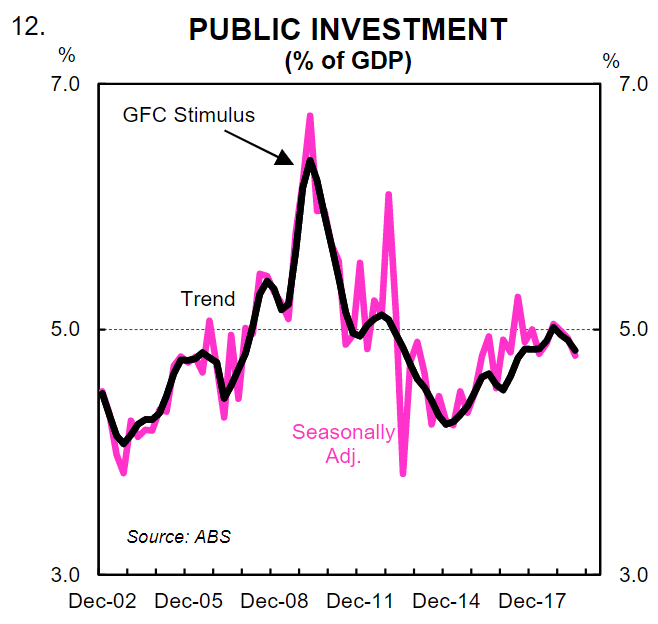

The benefits of good public infrastructure investment are clear. Sound investment boosts economic activity in the short run and living standards in the long run. Both State and Federal Governments recognise this and public investment has been ramped up significantly in Australia over the past four years (chart 12). And the pipeline of work to come is deep.

Whilst Infrastructure Australia has identified a range of infrastructure projects that make economic sense, it’s not that easy to simply mobilise and accelerate them without a significant cost. At a time when infrastructure investment is already running at turbo charged levels there is a risk that accelerating projects and commissioning new ones could see costs would blow out due to capacity constraints. There is also a risk of proceeding with newly “thought up” projects where the economic benefits are less obvious or there has not been careful and thorough due diligence. In that context, we would welcome a continued focus on delivering critical infrastructure projects to support the Australian economy now and into the future, but we are cautious on ramping up big infrastructure spending too quickly to stimulate demand. There is a case, however, in the short run to increase expenditure on smaller type projects, particularly maintenance. In any event, a further lift in public investment should not be a deterrent to bringing personal income tax cuts forward, particularly given bond yields sit at incredibly low levels (ie. the 10yr government bond yield is 1.3% and the 30yr is 1.65%).

Finally, the starting point is better

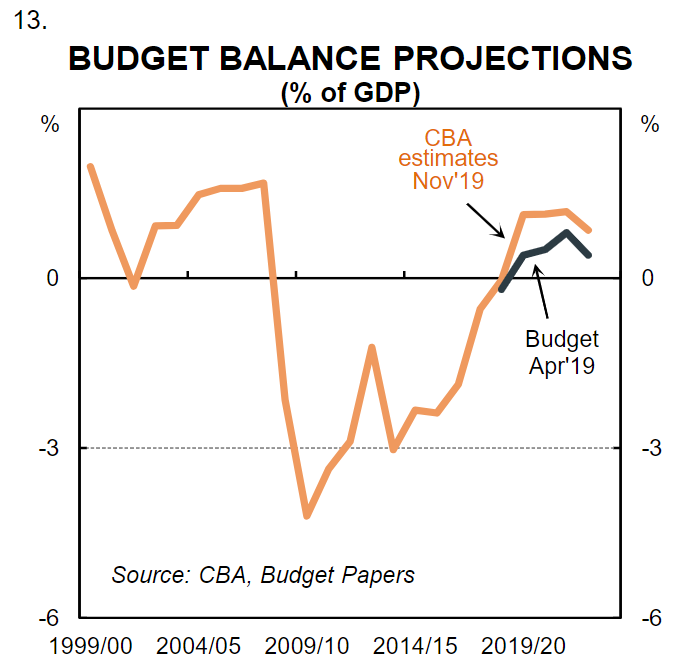

Our fiscal model suggests that the Commonwealth Budget is in a stronger position than was projected in the April 2019/20Budget. Based on the 2018/19 outcome (i.e. the starting point) and our profile for nominal GDP over the forward estimates period, we estimate that on a no-policy-change basis the Budget surplus will average 1.1% of GDP over the four years to2022/23 –compared with an average of 0.5% of GDP assumed in the Budget (chart 13). This means that even if the Government remains wedded to a surplus, there is still scope to boost household disposable income via tax cuts.

Summary

While economic growth remains below potential in Australia, the debate will continue to focus on what can be done to support aggregate demand. With conventional monetary policy close to being exhausted, we very much hope that attention is given to the other arms of policy that can be used to support the economy. In our view conventional fiscal policy should be deployed before UMP. The Budget is in balance and government net debt as a share of GDP is low. The case to bring the already legislated personal income forward is strong. It would give the household sector and the broader economy an immediate boost. And it would go a long way to helping the RBA achieve its objective of full employment, the economic prosperity and welfare of the people of Australia and inflation within the target band.

By concidence, Bill Evans at Westpac wrote a similar piece later this morning:

The recent Retail Sales Report for September has highlighted the state of demand in the Australian economy.

Real retail sales fell by 0.1% in the September quarter to be down by 0.2% over the year – the weakest result since 1991, when Australia was last in recession.

This Report is also consistent with the contraction in private domestic demand which we saw in the national accounts for the year to the June quarter.

That is despite consecutive rate cuts from the Reserve Bank in June and July and a $7.7 billion income tax cut for households (in the form of adjusting the tax offset, with a one-off lump sum payment) which started to become available from late in July.

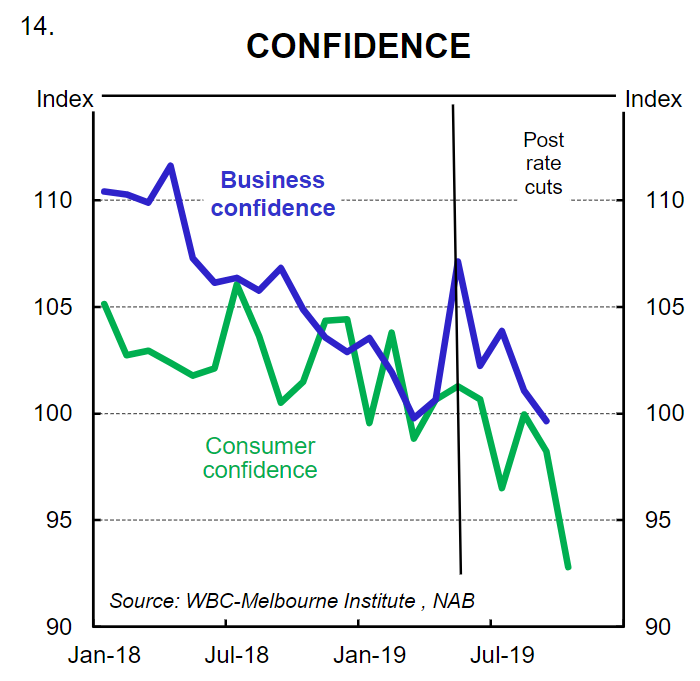

A notable headwind to household spending is the fragility of Consumer Confidence. The Westpac MI Index of Consumer Sentiment slumped by 4.1% in July to 96.5. A rebound in August

was short-lived. The latest print, for October, has the index down by 5.5% to a four year low of 92.5.

This weakness in Consumer Confidence is mirrored by weakness in Business Confidence and Conditions, which has extended throughout the September quarter, as evident in the NAB Survey.

We assess that the very low interest rates which the Reserve Bank has had to implement are now impacting confidence as consumers equate low interest rates with disturbing weakness in the economy.

The Reserve Bank has recognised that issue and is trying to balance the impact of lower rates on confidence with the benefits of lower rates through the traditional channels of lowering the AUD and boosting households’ disposable income.

A lift in spending through that second channel is being impacted by the confidence effect and the policies of some banks to adjust mortgage repayments with a lag – meaning that initially households pay down debt more rapidly rather than benefitting from improved cash flows.

We expect the RBA will persist with lower rates with one more cut to the cash rate next February. That decision may be represented as a package with additional stimulus taking the form of quantitative easing through a program of purchases of CGS; RMBS and other corporate securities and, possibly, long term funding for financial institutions.

It will be necessary to signal further stimulus through a program to maintain downward pressure on the AUD. With other central banks including the Federal Reserve; the ECB; the BOJ and the PBOC continuing to ease financial conditions the AUD will be at risk of unwelcome upward pressure if the RBA signals an end to its easing cycle.

Those monetary policies will reflect a difficult year in 2020 for the world economy as trade disputes, complemented by uncertainty around the US Presidential election, continue to impact investment and confidence.

However, as the RBA and other commentators have been highlighting, this need to boost demand also requires some support from fiscal policy.

Westpac acknowledges that there are supply constraints, particularly in Sydney and Melbourne, for new large infrastructure projects. Boosting productivity of existing infrastructure through repairs and maintenance should be considered by the authorities as well as bringing forward appropriate projects in the Commonwealth Government’s current infrastructure plans.

The Federal Government’s mid-year budget update to be released in December, the MYEFO, is also likely to include further commitments to drought relief and aged care.

We are less supportive of further business investment allowances which have been mooted for the 2020 Budget. The instant writeoff threshold has already been boosted to $30,000 and extended to companies with turnover of up to $50 million, covering 3.4 million businesses, employing around 7.7 million workers.

Business investment, particularly for big business, is being held back by concerns around the global economy; weak domestic demand and, in some cases, credit availability. Boosting investment allowances is unlikely to make a marked difference to investment given these ongoing constraints.

To boost demand, both household and business, it is better to accelerate the personal income tax cuts which the government has already legislated for July 2022.

Tax cuts which are designed to provide a short term boost to demand should be avoided. Australia’s political structure almost ensures that it is near impossible for governments to reverse tax cuts when the cyclical need has passed.

They can only be justified on structural grounds. The second stage of tax cuts which the government has legislated to begin in July 2022 should be brought forward. That decision would not compromise the structural validity of the cuts but would recognise that the Australian economy is in need of a boost to demand, from fiscal policy, much sooner than 2022.

We disagree with both. Households are determined to deleverage. More tax cuts will simply fall into this private surplus black hole and do little for economic activity. Even more so given the further out that the tax cuts go the more they are biased towards higher income brackets that will save it any windfall anyway.

Advertisement

Stimulus should be focussed upon infrastrcuture spending and income relief for lower income households via boosted Newstart to give the biggest bang for a buck in terms of domestic demand.

To be honest, we don’t get why the banks want tax cuts given they will only accelerate the runoff of their own mortgage back books!