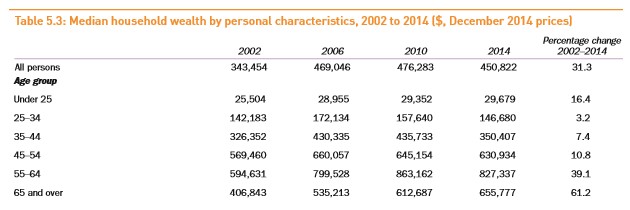

Although older Australians have captured an increasing share of Australia’s wealth:

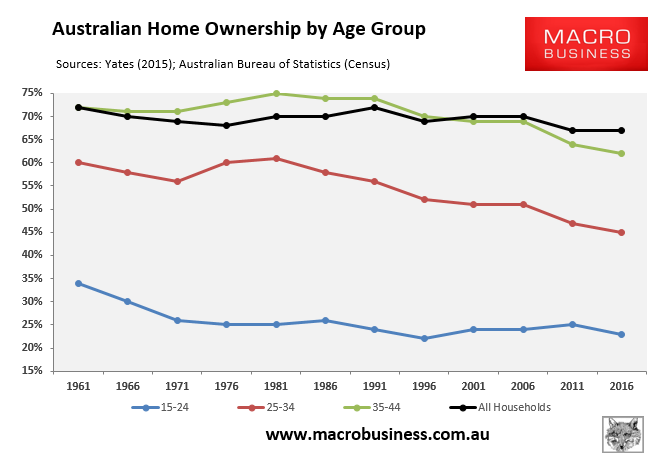

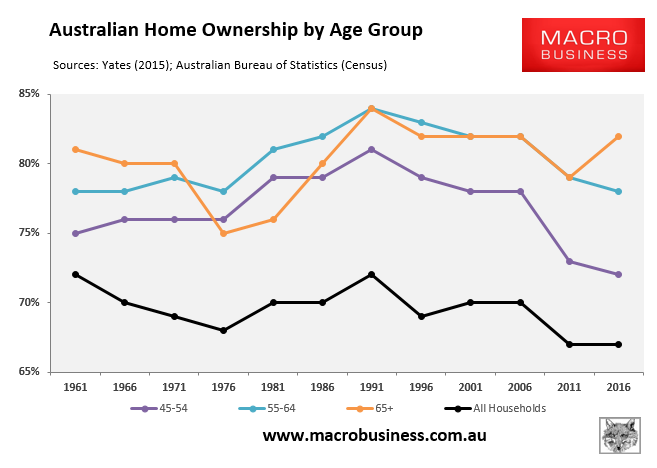

Largely because they have increased their home ownership rates over the past 55 years at the same time as home values have skyrocketed:

Advertisement

Although older Australians have captured an increasing share of Australia’s wealth:

Largely because they have increased their home ownership rates over the past 55 years at the same time as home values have skyrocketed:

The full text of this article is available to MacroBusiness subscribers