Via Bill Evans at Westpac:

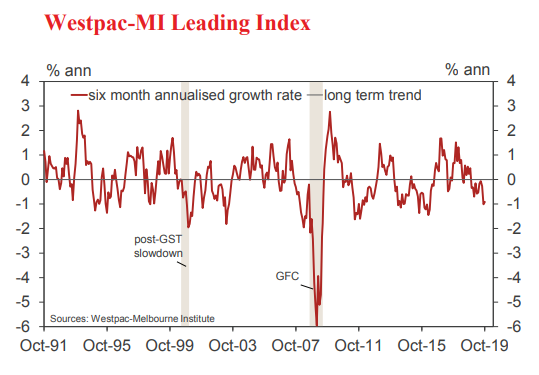

• The six month annualised growth rate in the Westpac– Melbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, lifted from –1.01% in September to –0.91% in October.

Despite a slight improvement in the month, the Leading Index growth rate remains materially below trend and continues to point to weak economic momentum carrying well into 2020.

This below trend “theme” for the Australian economy is consistent with Westpac’s current forecast for GDP growth in 2020 of 2.4%, compared to a trend growth rate of 2.75%.

The Reserve Bank has recently released its revised growth forecasts for 2019, 2020 and 2021. It has maintained its view that year on year growth in 2020 will return to trend, at 2.8%, for the first calendar year since 2016. The main differences between Westpac and the RBA are around the timing and extent of the recovery in residential dwelling investment and the outlook for business investment. We are broadly in agreement that another below trend year for household expenditure can be expected with the outlook particularly dependent on policy responses and the risks being to the downside.

The Leading Index growth rate has deteriorated over the last six months from –0.53% in May to –0.91% in October. The main components driving the 0.39ppt shift have been a sell-off in commodity prices (–0.43ppts); a more mixed performance on the Australian sharemarket (–0.20ppts); a deterioration in consumers’ unemployment expectations (–0.17ppts), in consumer expectations more generally (–0.10ppts); and a slowdown in monthly hours worked (–0.07ppts).

These negatives have been partially offset by a further improvement in the yield spread following the RBA’s October rate cut (+0.31ppts) and marginal improvements in US industrial production (+0.17ppts) and dwelling approvals (+0.11ppts).

The Reserve Bank Board next meets on December 3. Westpac expects the Board to hold the cash rate steady at that meeting. The minutes of the November Board meeting signalled that the Board continues to hold a clear easing bias while, for now, remaining in ‘monitor mode’.

We expect that by next February the Board will have received enough information on the impact of the three cuts we have seen since June to acknowledge the need to reduce the cash rate by a further 0.25%, maintain a clear easing bias and consider introducing unconventional policies.