DXY was down last night as EUR rose and CNY fell:

The Australain dollar was dumped anyway:

As gold fell:

And oil:

Plus metals:

And miners:

EM stocks flamed out:

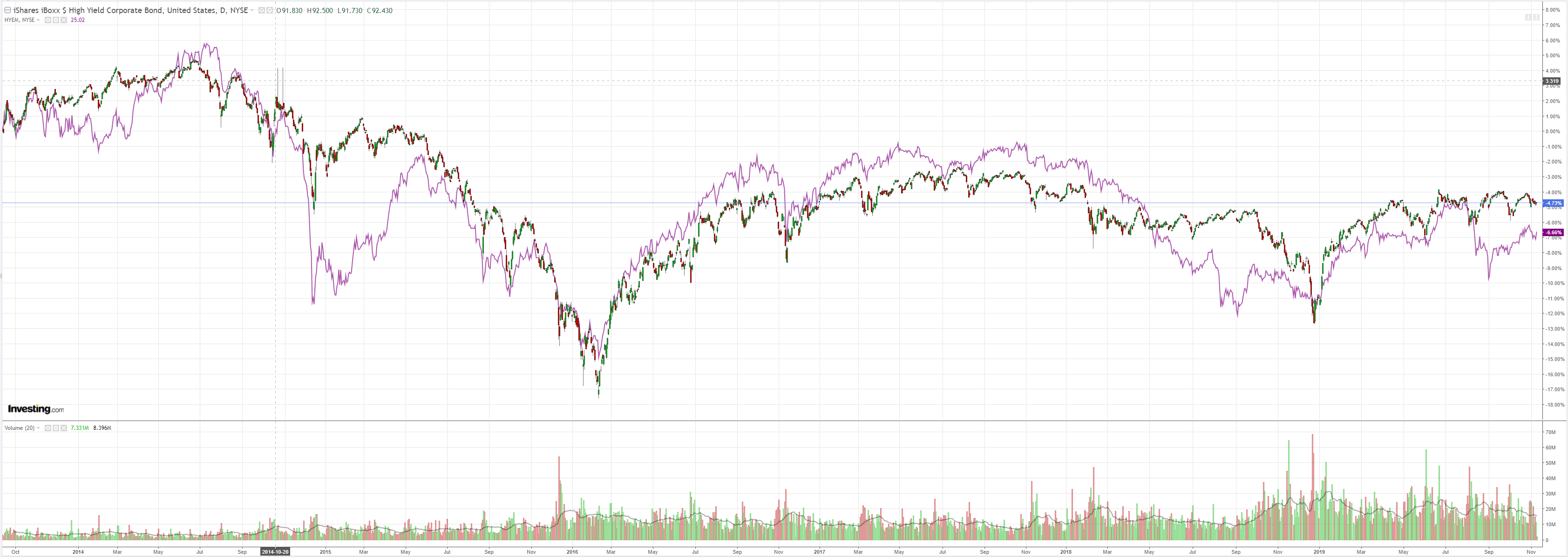

Junk fimed:

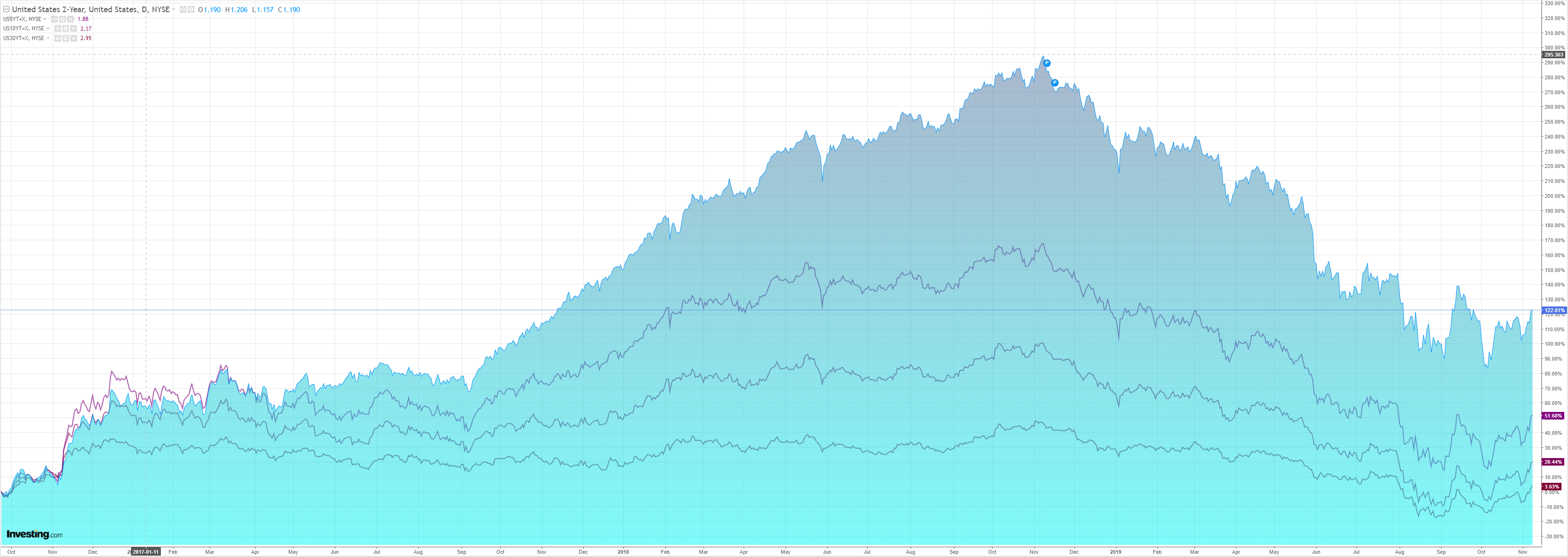

US yields eased:

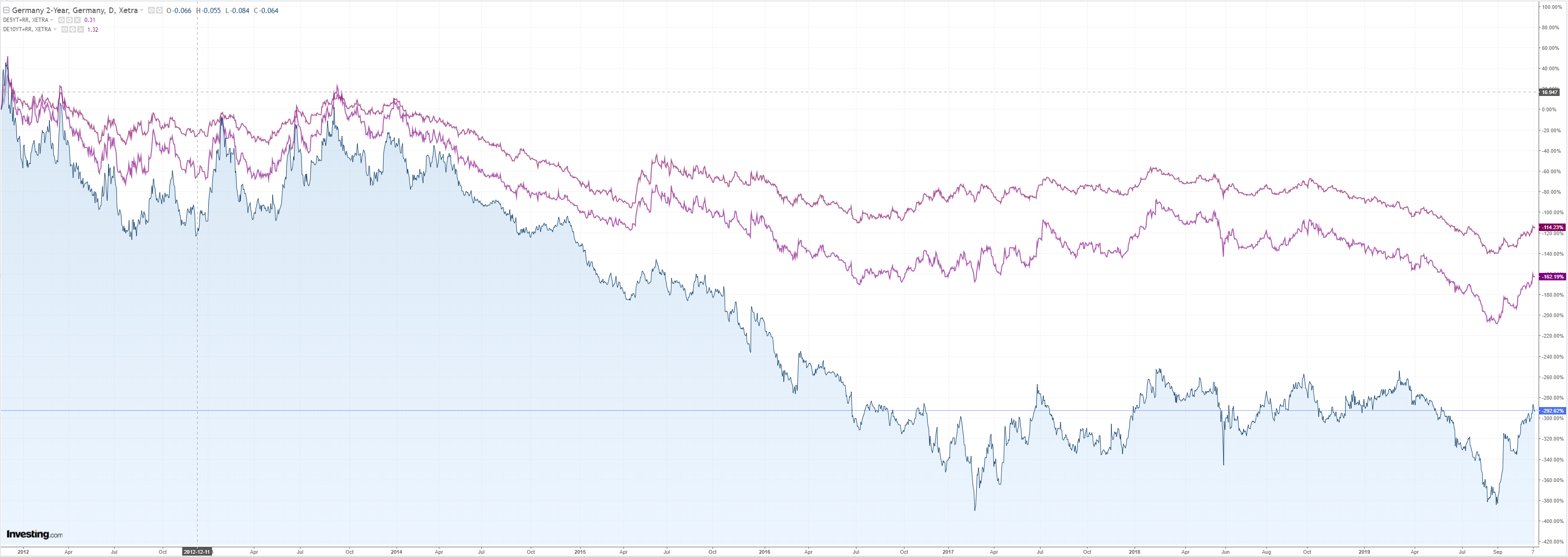

Bunds eased:

Aussie bonds were bought:

Stocks edged down:

Westpac has the wrap:

Event Wrap

Brexit Party leader Farage said that they would not stand in existing Conservative seats. Although this still means that votes may be split in marginal seats, the news reduced the market’s concerns over another dysfunctional minority or a hard-left Labour led coalition.

UK 3Q GDP at +0.3%q/q (est. +0.4%q/q) was slightly disappointing but avoided a technical recession. Most components were skewed to the downside though business investment was, surprisingly, not as weak as expected (-0.6%q/q, est. -1.1%q/q) and exports were firm (+5.2%q/q, est +2.9%). September production data was overall soft; GDP of -0.1%m/m meeting expectations, but industrial (-0.3%m/m, est. -0.1%m/m) and manufacturing (-0.4%m/m, est. -0.2%m/m) production soft. The trade deficit widened in Sep to –GBP3.36bn (est. –GBP2bn).

Event Outlook

NZ: The RBNZ’s 2yr-ahead inflation expectations survey fell from 2.01 to 1.86% in Q3. A material move in Q4 could influence the RBNZ’s OCR decision on Wed.

Australia: Oct NAB business survey last showed conditions at +2, a still soft level with no signs yet of a stimulus boost.

Europe: Nov ZEW survey of expectations is released.

UK: Sep ILO unemployment rate is expected to hold at 3.9%.

US: President Trump speaks at the Economic Club of New York. Fedspeak involves Clarida on “Monetary Policy, Price Stability, and Bond Yields” and Harker in New York.

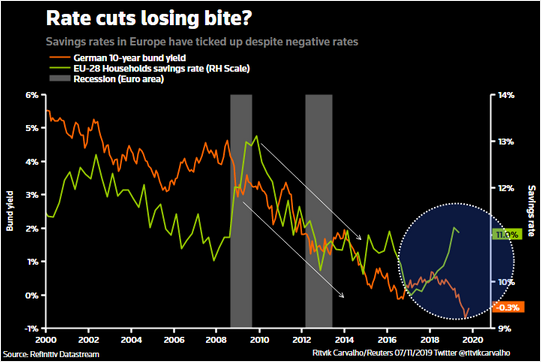

The data continues to support the status quo of a weak AUD. Europe cannot get off the canvas as the ECB pushes on a string:

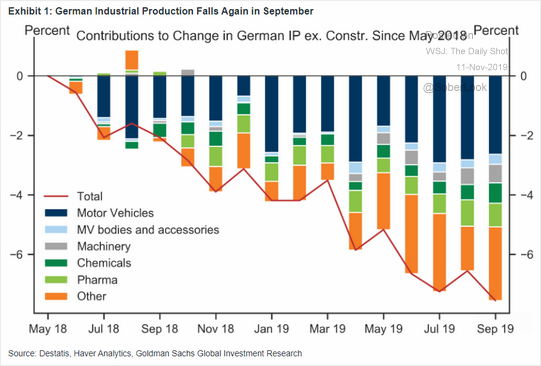

German industry is toast:

Like, universally:

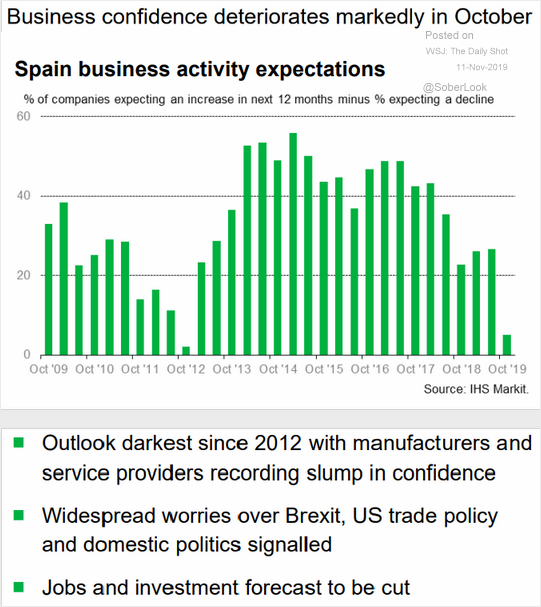

It is spreading to the periphery in Spain:

And Ireland:

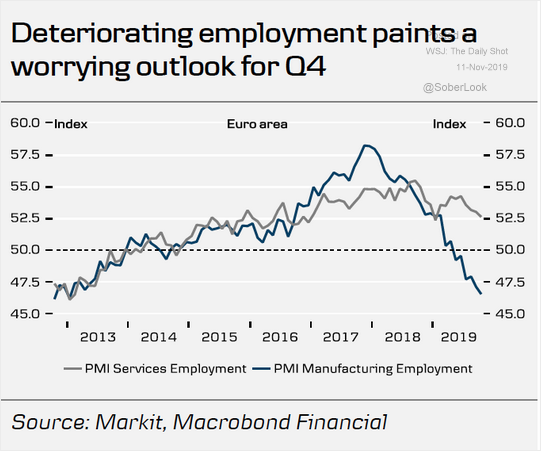

Jobs are next:

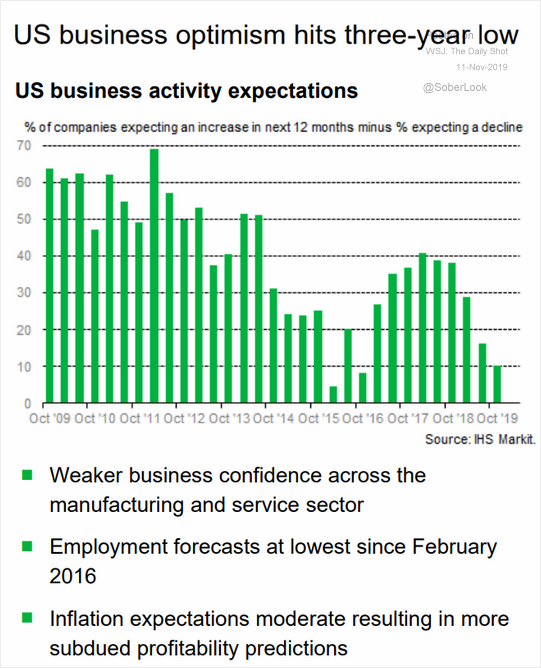

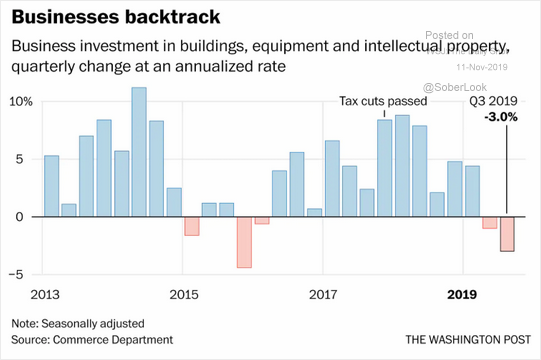

The US is also fading:

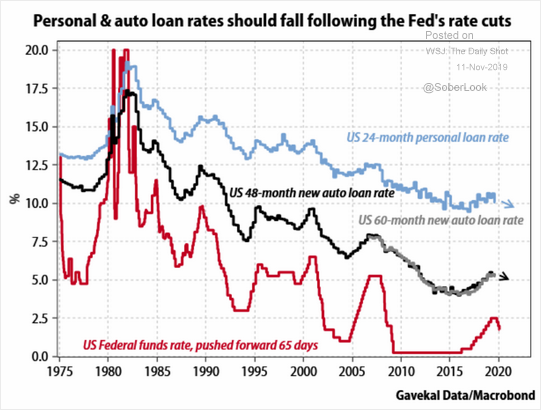

But it’s consumer is much better as wages rise:

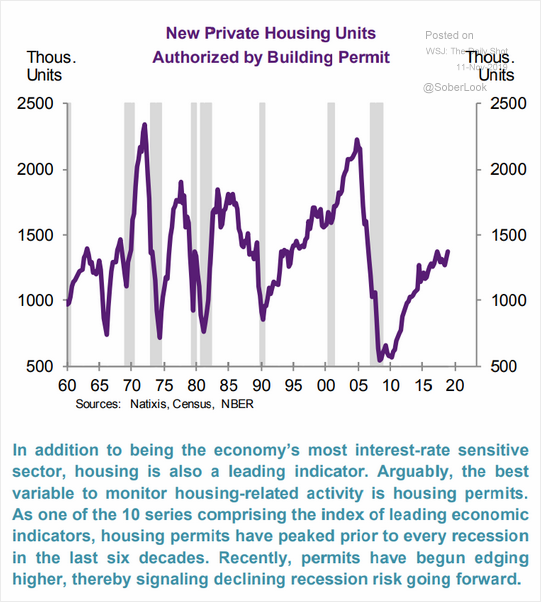

Along with the silver bullet of the housing maarket:

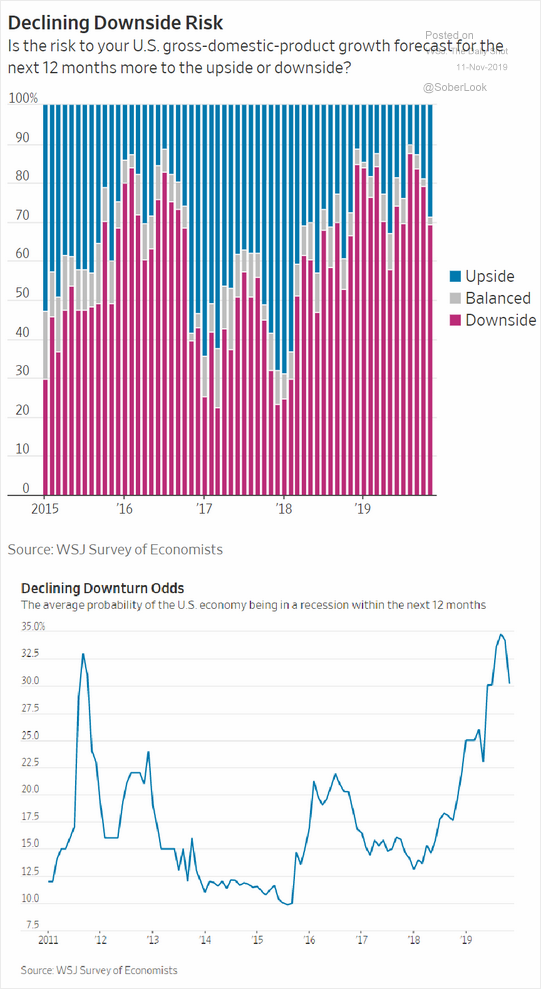

Recession fears are declining now:

It still favours the USD over EUR which is set up for an ongoing weak Australian dollar, exacerbated by general global weakness and a sagging China expressed in falling commodity prices.