Suddenly, DXY is back and it’s bad as EUR sinks:

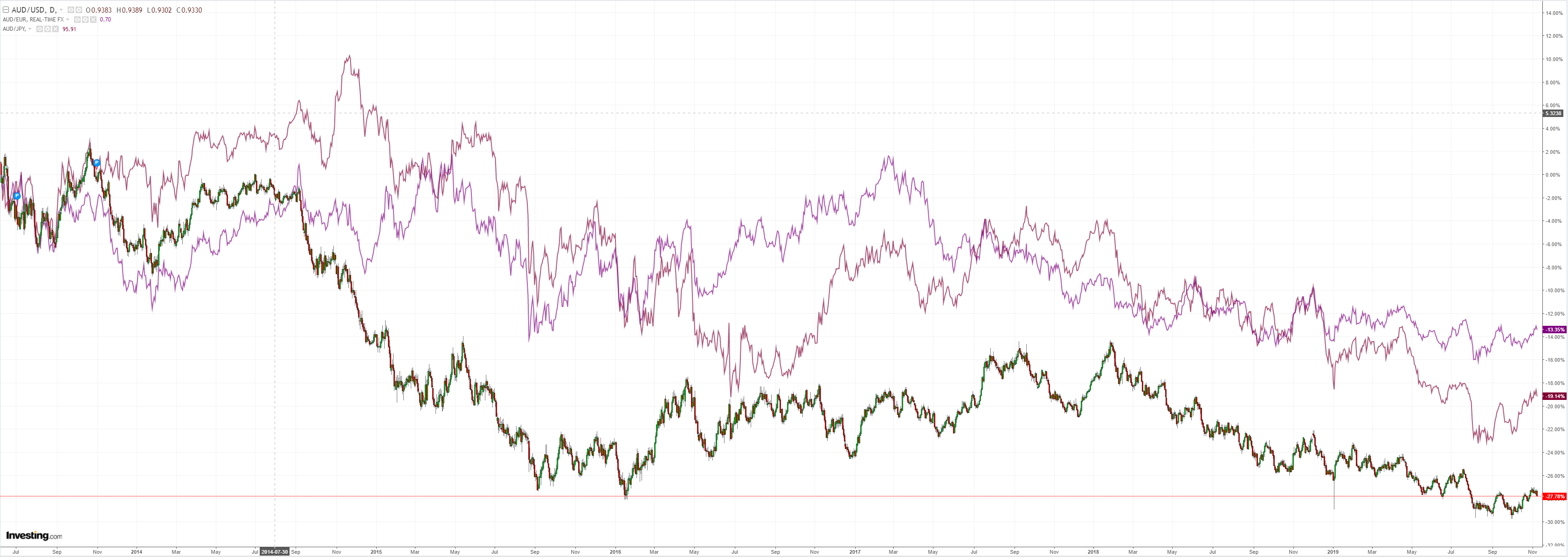

The Australian dollar fell sharply against DMs:

It was mixed agianst EMs:

Gold was bashed:

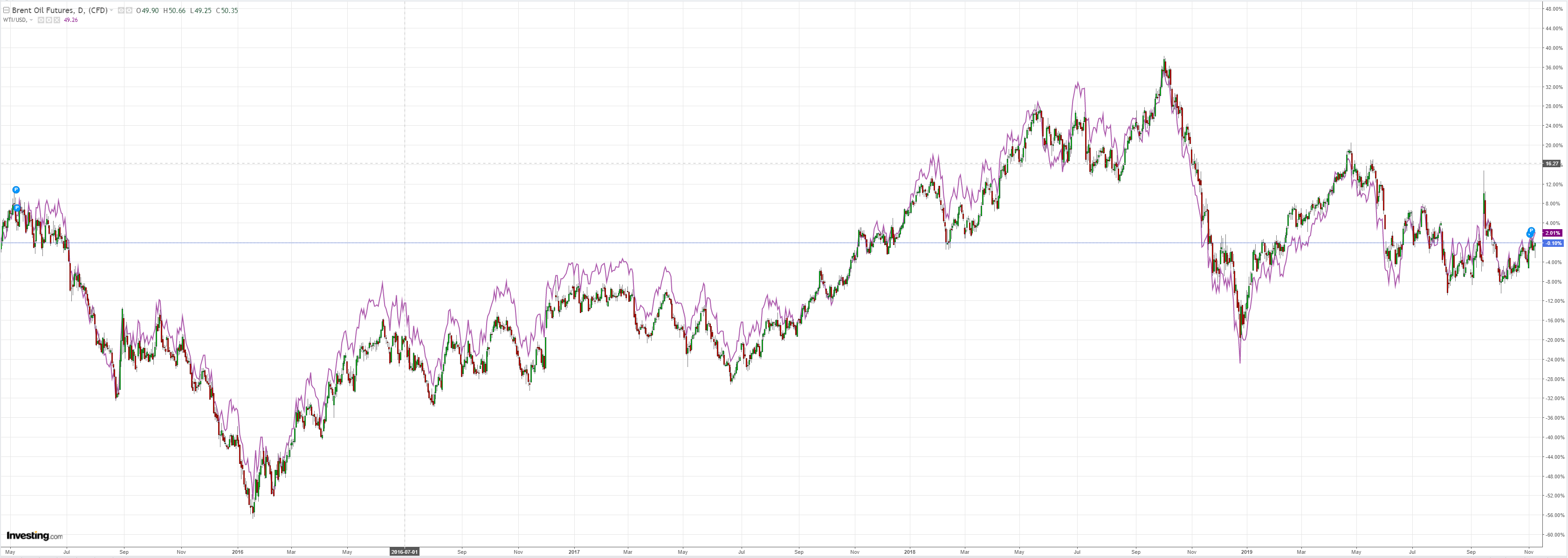

Oil lifted:

Metals fell:

Miners were clubbed:

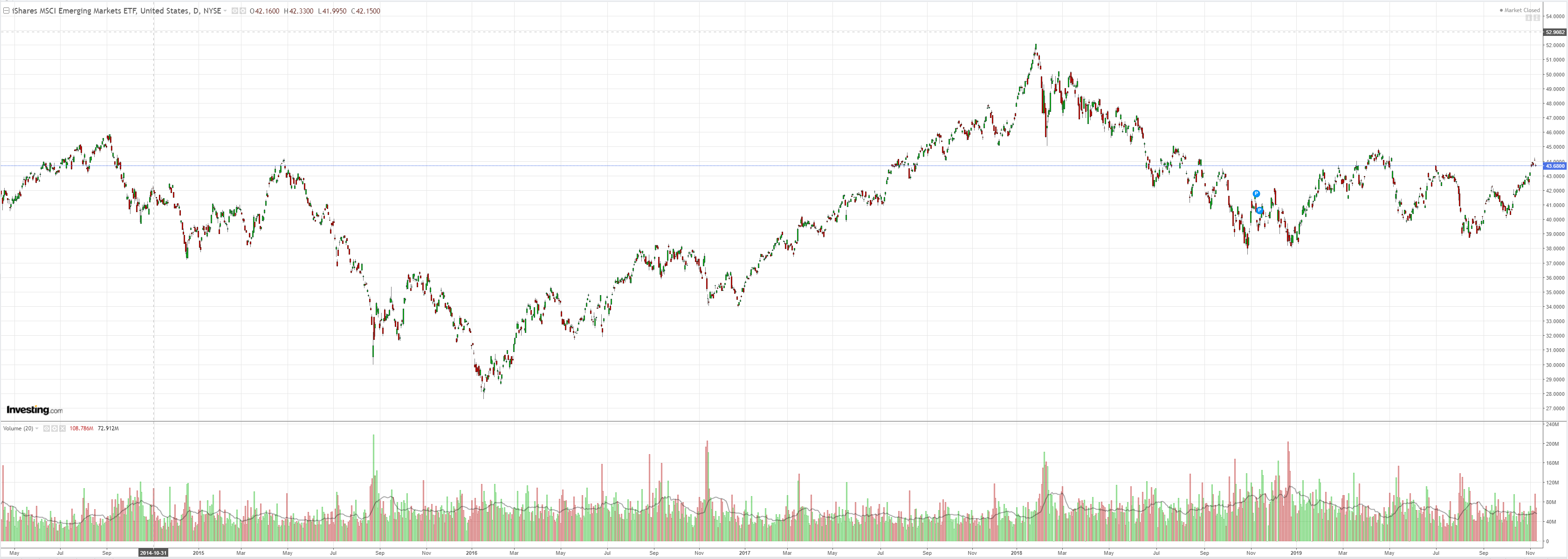

EM stocks flamed out:

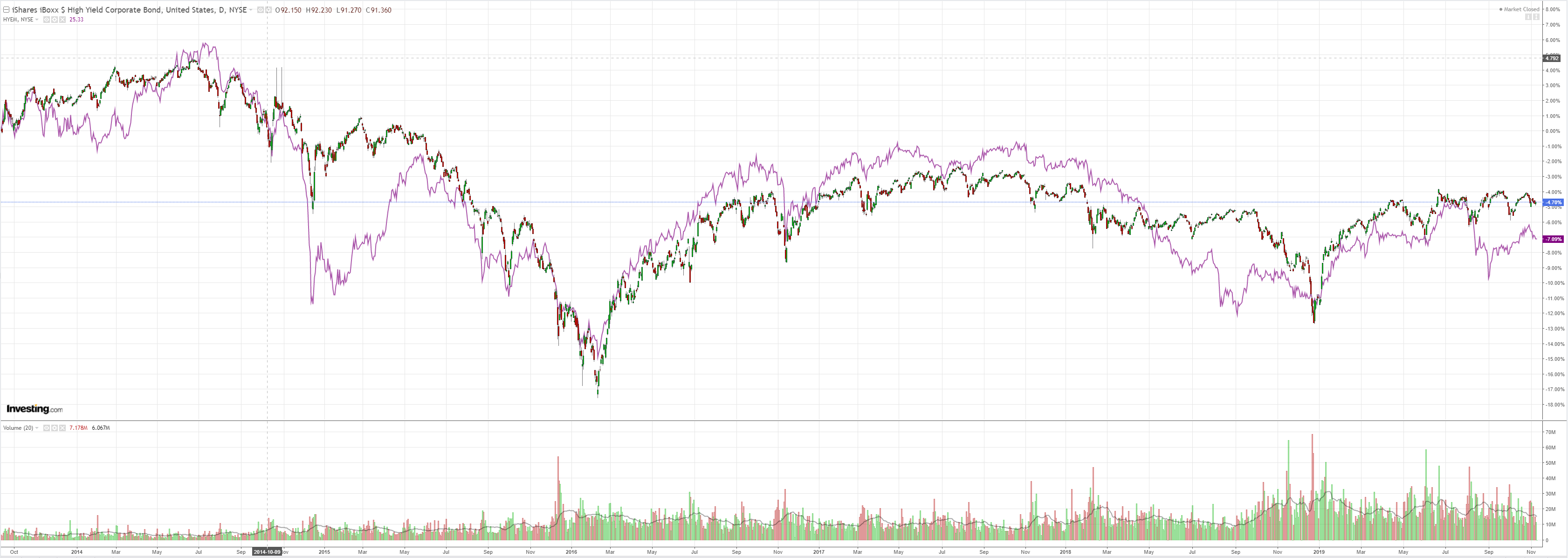

Junk was soft:

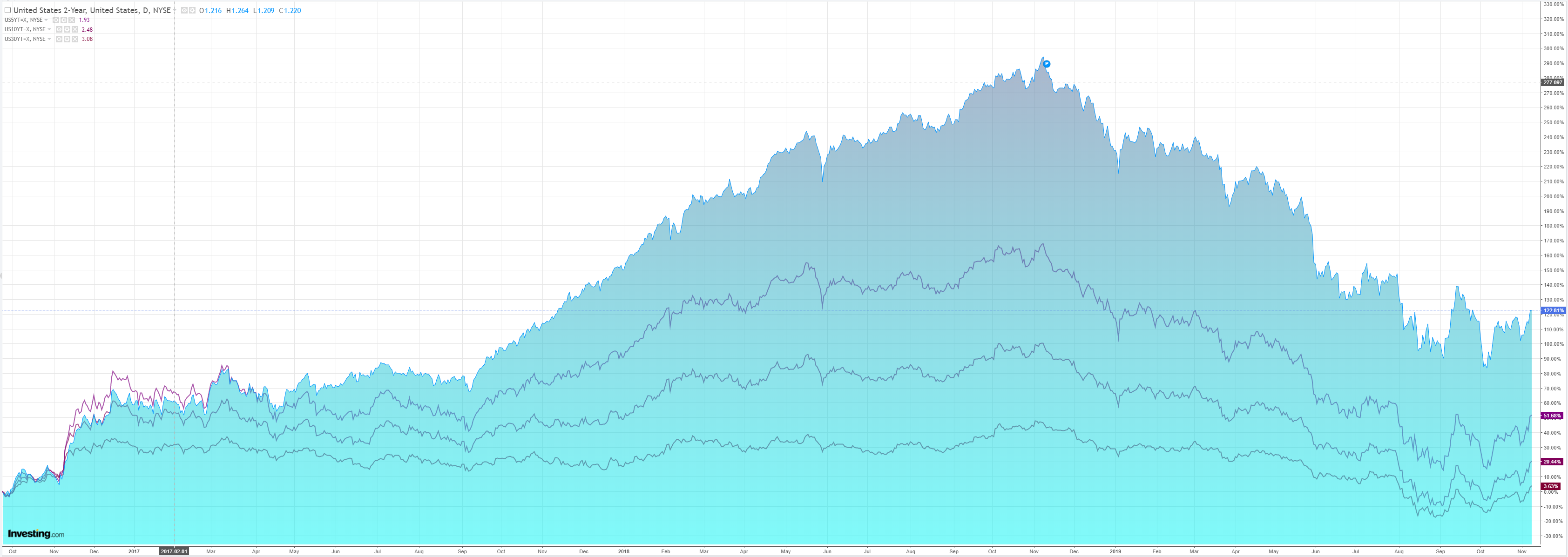

US yields edged up:

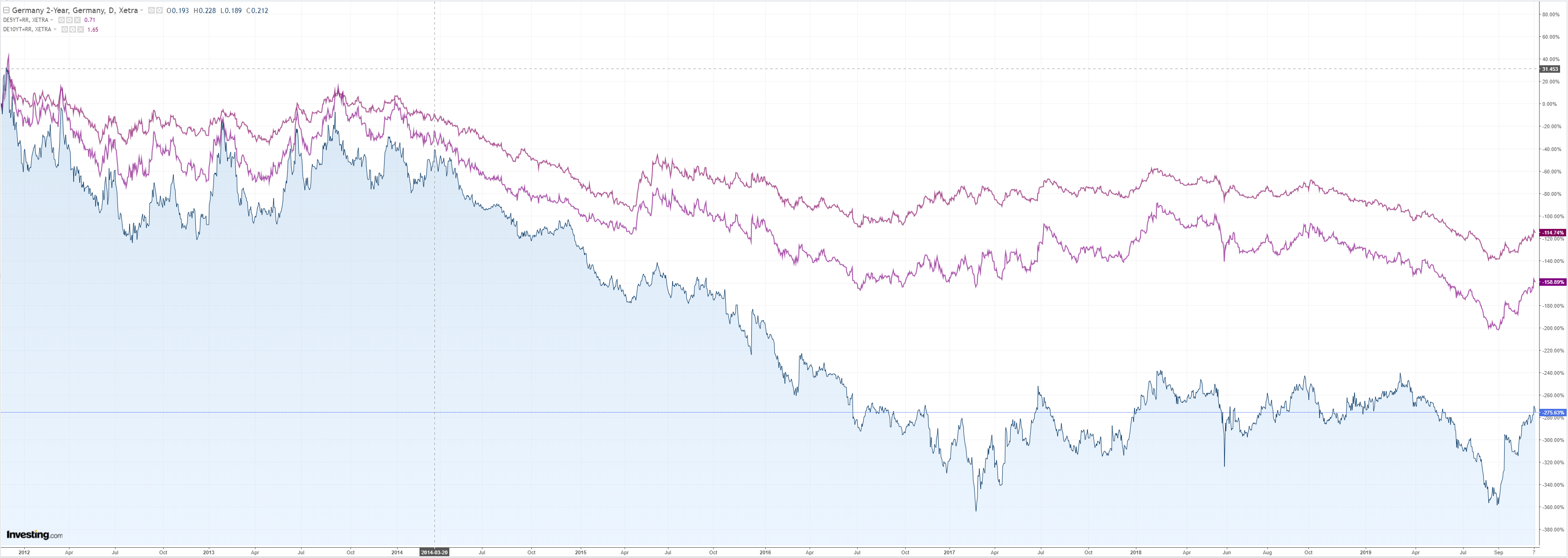

Bunds went the other way:

Aussie kept selling:

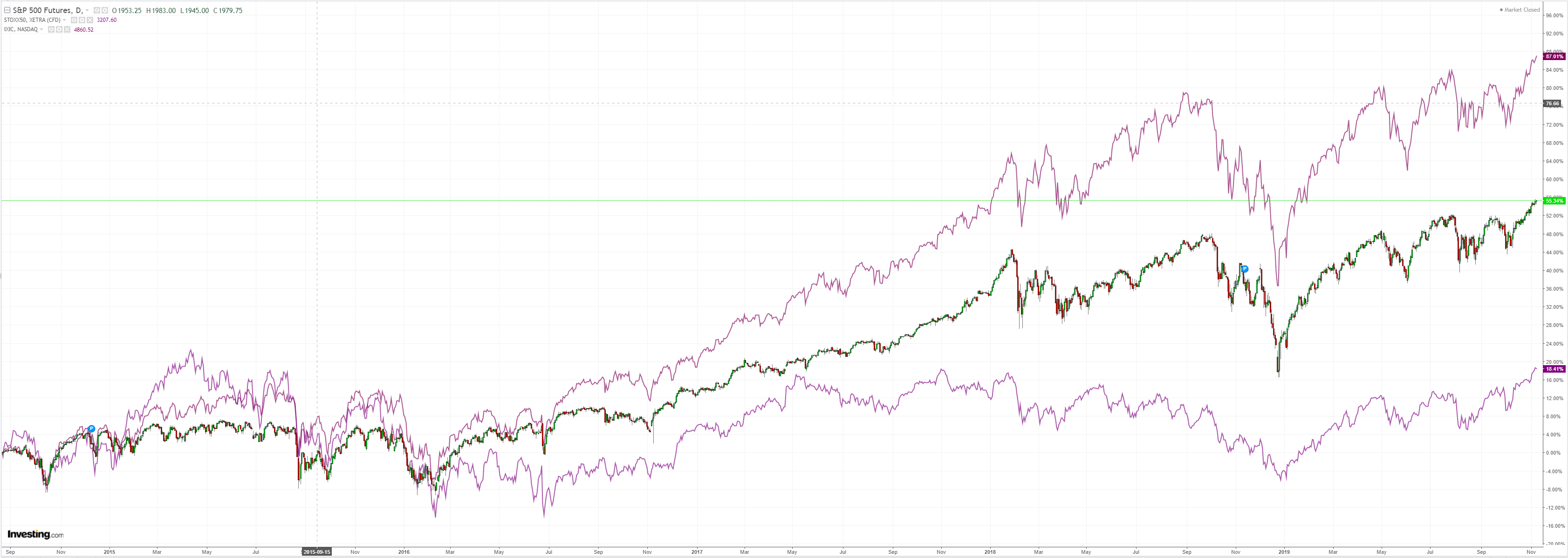

Stocks hit new highs:

El Trumpo upset the apple cart, as he does, via Bloomie:

President Donald Trump said trade talks with China are moving along “very nicely,” and said the leaders in Beijing wanted a deal “much more than I do.”

Trump also described as “incorrect” reports about how much the U.S. was ready to roll back tariffs on China.

“If we don’t make that right deal, we’re not going to make a deal,” Trump told reporters on Saturday as he prepared to board Air Force One for a trip to Alabama to watch a college football game. “A lot of positive things are happening.”

China does need a deal much more than the US so I’m not sure why Trump is so busy bending over for it.

Anyway, for now, we have an interesting divergence between bond yields selling off on perceived receding political risk, and relaunched QE, but forex still reacting more to fundamentals with the global economy far from out of ther woods. From Westpac:

Over the month, the AUD has lifted from USD 0.675 to a high of USD 0.698. This move has partly been the result of a weaker USD, and partly due to genuine strength in the AUD

The 3.4% move in the AUD against the USD can be largely explained by outright strength in the AUD and residual weakness in the USD. Over the period, the AUD Trade Weighted Index has lifted by 1.2% complemented by around a 1.5% fall in the USD Trade Weighted Index. This lift in the AUD has surprised us given last month, when the AUD was holding at USD 0.675, we had forecast the AUD at USD 0.67 by December.

There are two key reasons explaining the weakness in the USD and the strength in the AUD.

Firstly, markets are now embracing the view that the rate cut in October may be the RBA’s last cut in this cycle. Market pricing is currently giving only around a 40% chance of a cut in February and assessing the “resting” rate in the cycle at 0.6%. Following the October cut by the RBA, markets were pricing a follow up cut in November at a probability of around 50%; a December cut at 85% and a “resting” cash rate of 0.37%. While not embraced by market pricing, there was also liberal “talk” about the possibility of negative interest rates in Australia.

Westpac was never convinced of the November/December cuts, or the negative interest rate scenario, but has maintained its conviction that the RBA will cut the cash rate to 0.5% in February to establish the low in the cycle. The market’s confi dence around the RBA cash rate outlook appears to have been in response to recent comments from the RBA Governor around a “gentle turning point” and his conviction that growth in the Australian economy in 2020 will lift to around trend (after three consecutive years of being below trend).

However, we should not overlook the sentiment in the Governor’s Statement following the November Board decision, “The Board is prepared to ease monetary policy further, if needed”.

A key issue here is the concern the Board is likely to be harbouring around the recent “lift” in the AUD. As we have argued before, the AUD would (and perhaps already has) become vulnerable to unwelcome upward pressure if the RBA was seen to be on hold in this cycle – a cycle where the other major central banks – FOMC; ECB; BOJ and PBOC – are likely to continue easing policy through 2020.

The second key development has been a drift away from “risk-off ” sentiment globally to “risk on”. That drift has weakened the USD and boosted some currencies like the AUD.

I see two key drivers of this “risk-on” sentiment.

Firstly, there is considerable optimism around the achievement of a phase one trade deal between the US and China. That successful outcome is, at least to some extent, already priced into the market, particularly after Chinese Commerce Ministry spokesman Gao Feng’s comments which inferred a rolling back of tariff s on both sides could be part of phase one.

Reports on the exact detail of China’s demands have varied. But a deal could potentially require some or all of the tariff s imposed to date being removed. These include: the 15% tariff on $125bn of goods imposed on September 1; the 25% tariff imposed previously on $250bn of goods covering semi-conductors machinery, furniture, etc; and the tariff scheduled for December 15 on around $150bn of mainly consumer goods. Pricing in such an apparent capitulation by the

US President seems a risky position for the market, particularly if there is still no progress on intelectual property protections and other key issues for the US.

Secondly, markets are convinced that the FOMC will be on hold in December, with the low point in the rate cycle being 1.36% in December 2020. Westpac has revised its US view to accept that the FOMC will be reluctant to move in December. The line “[the] Committee will continue to monitor the implications of incoming information for the economic outlook as it assesses the appropriate path of the target range for the federal funds rate” from the October statement clearly signals a pause to monitor momentum, at least in the near term.

However, we continue to believe that there will be three more FOMC cuts in this cycle (versus market pricing of around one) as the US economy slows through 2020 to a pace below the potential rate of around 1.8%. Recognition of a resumption of rate cuts from the FOMC will highlight the uncertainties around global growth and act as a headwind for the AUD in 2020.

With these observations in mind we are still comfortable with our call for the AUD to reach USD 0.66 through the first half of 2020.

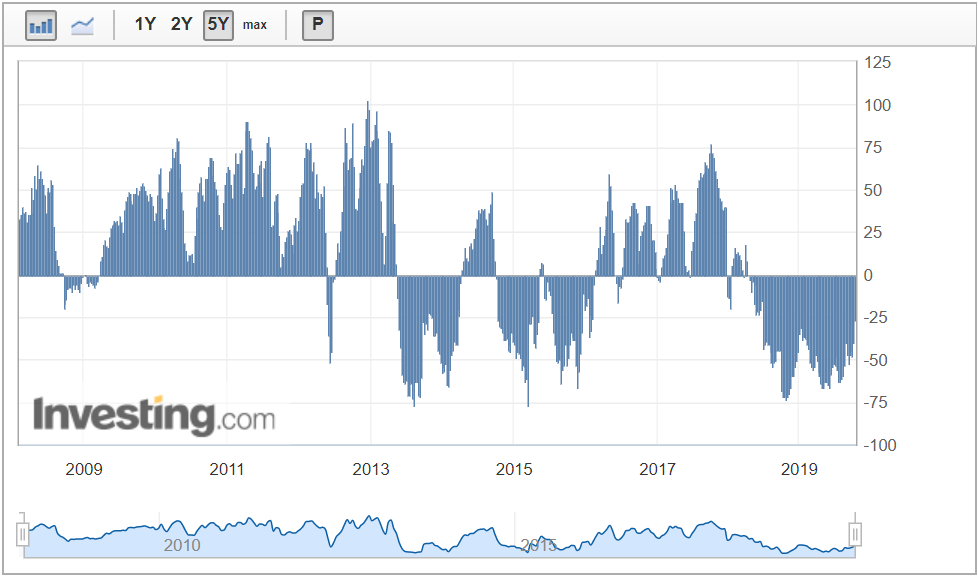

That seems reaonable to me. Australian dollar shorts puked last week on the risk trade, falling heavily to -26k contracts, the lowest since mid-2018:

This is great news for bears. The market has been so short for so long that it has struggled to go lower. A good clear out with prices only lifting 1 cent sets us up for material downside. Hopefully the washout gets us back to neutral without much further price damage.

Then still weak/ening global growth in 2020 that hammers bulk commodities such as iron ore and coking coal can be expressed through a falling Australian dollar.