DXY fell again Friday night but can still fall another goodly distance before threatening its uptrend

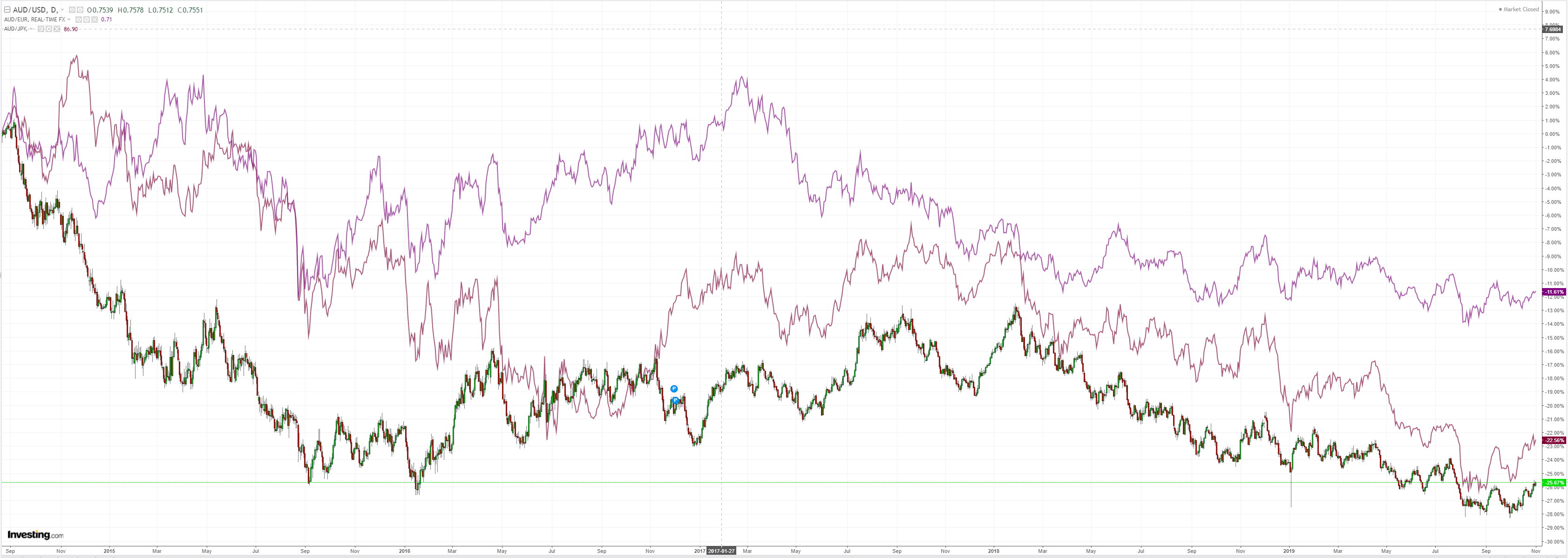

The Autralian dollar was up against DMs:

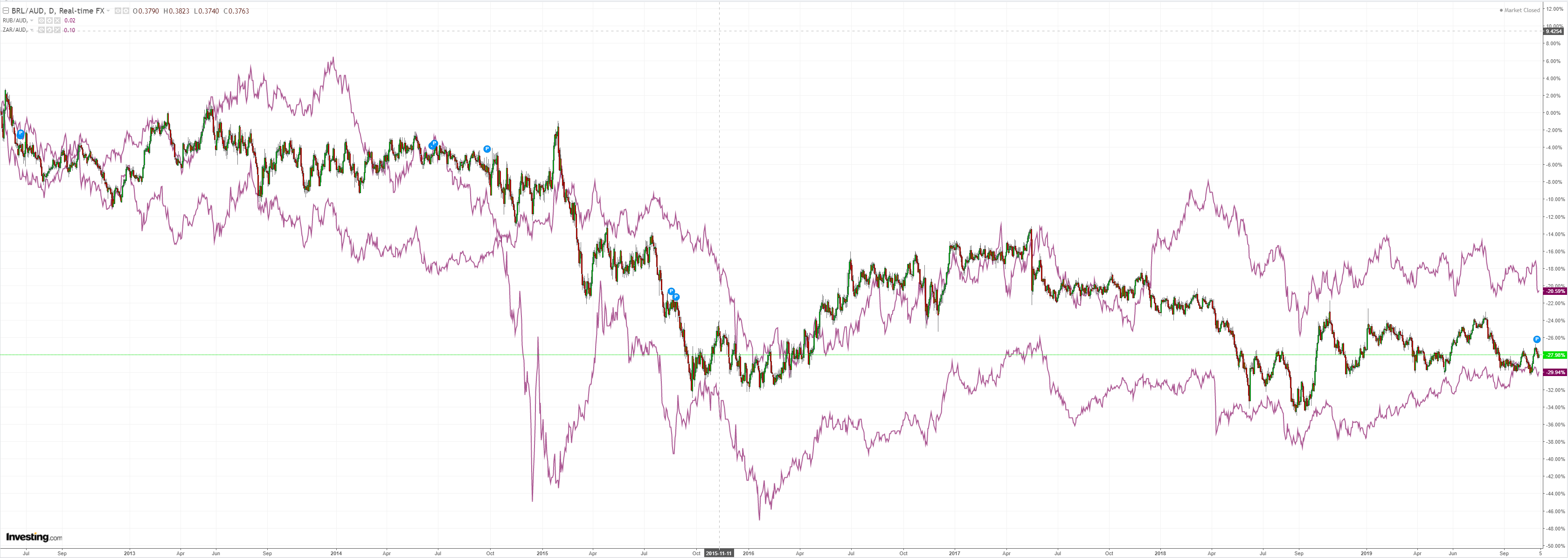

But EMs were stronger:

Advertisement

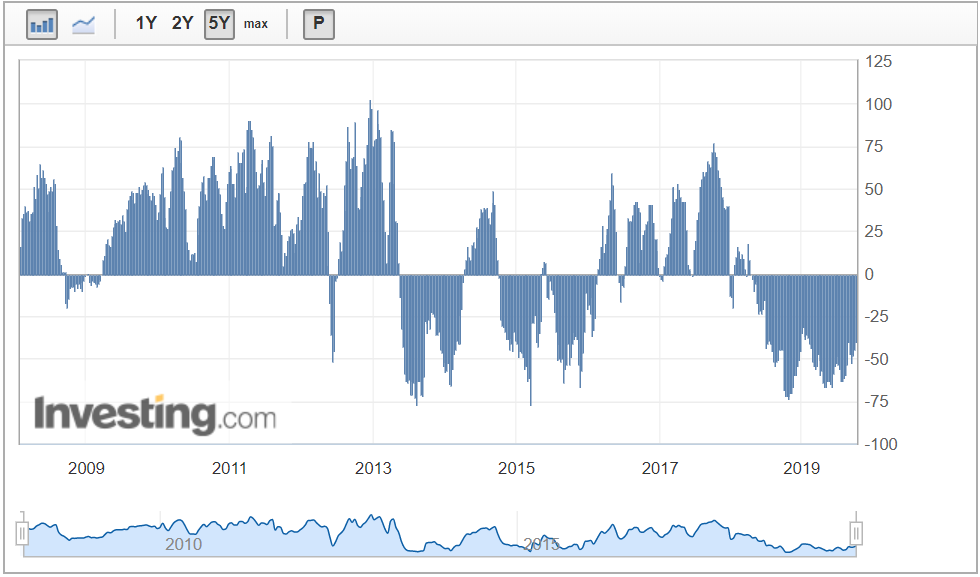

AUD shorts are near the least since the start of 2019 at -40k contracts on CFTC:

Gold looks more constructive:

Advertisement

Oil rose:

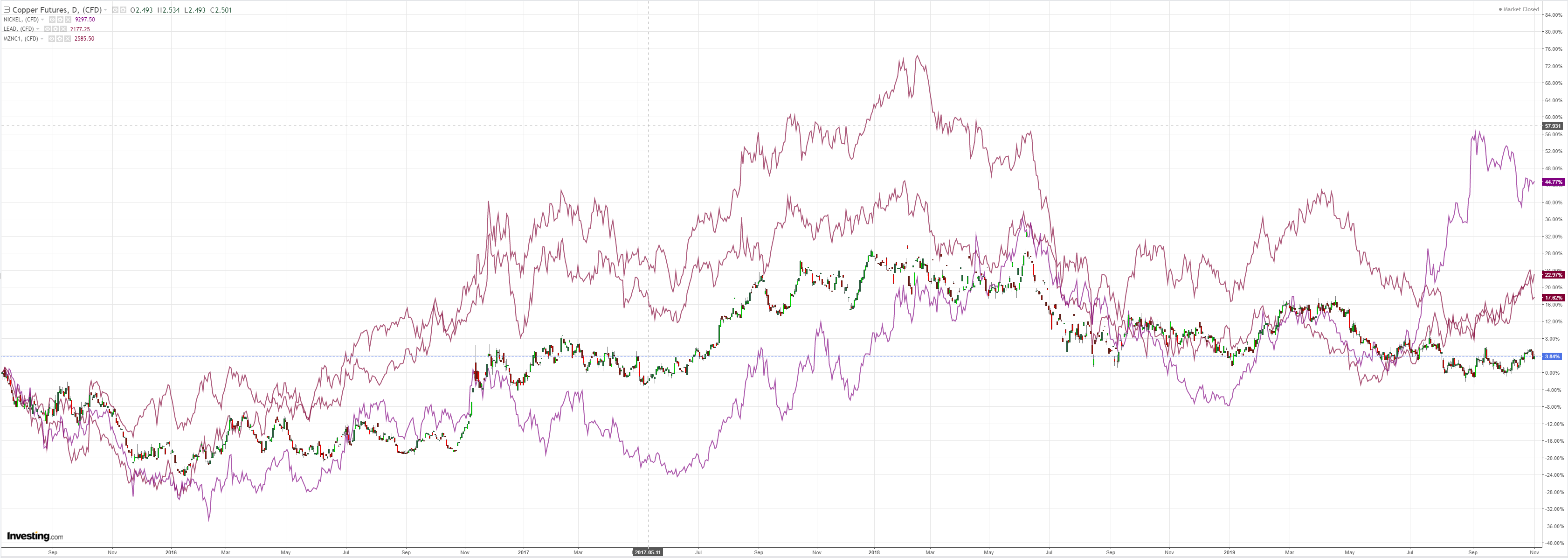

Metals too:

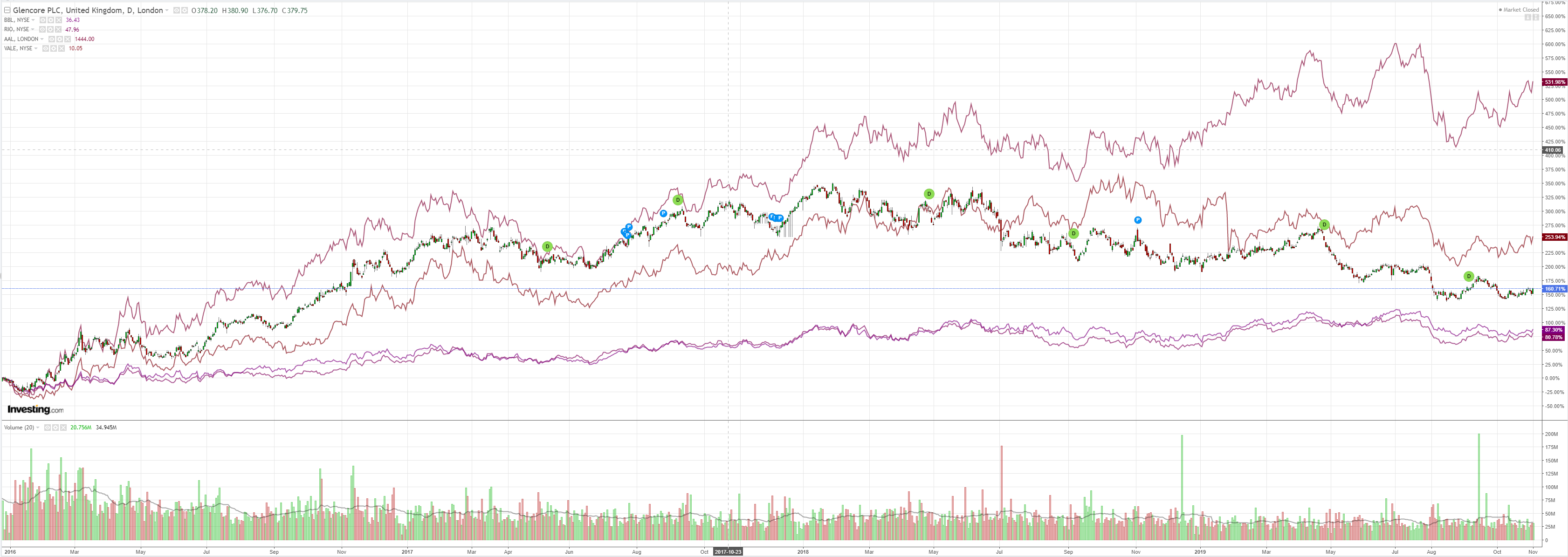

And miners:

Advertisement

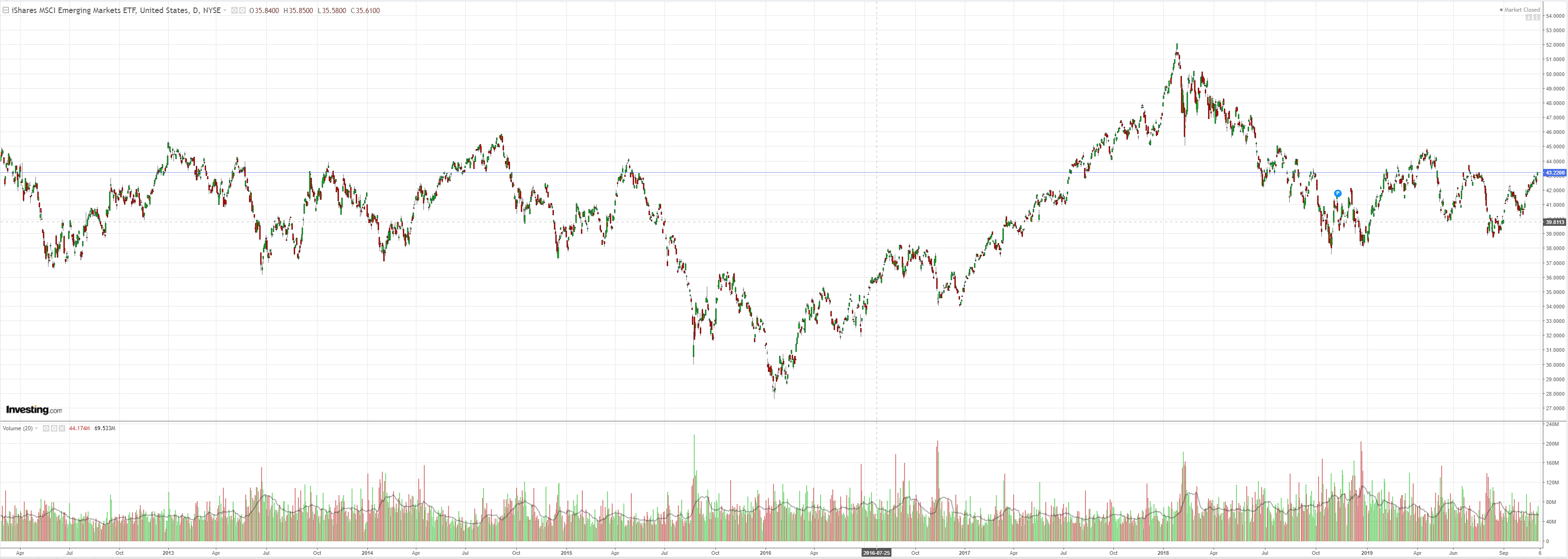

EM stocks are blasting towards breakout:

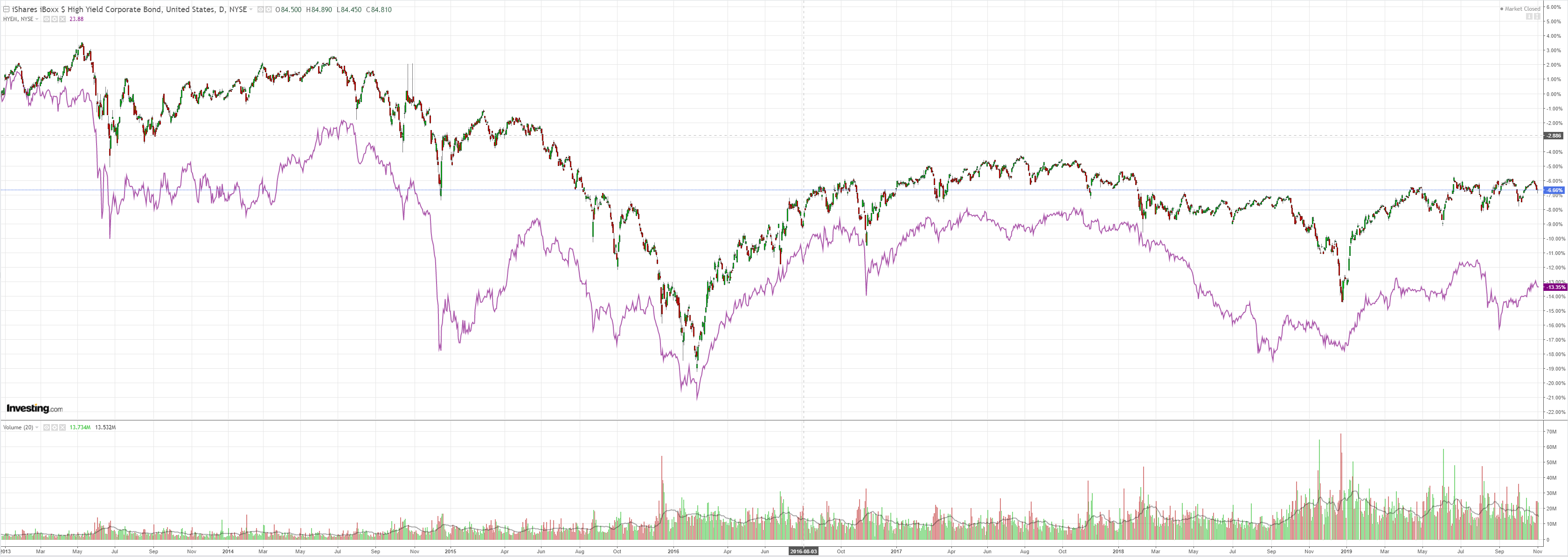

Junk was soft:

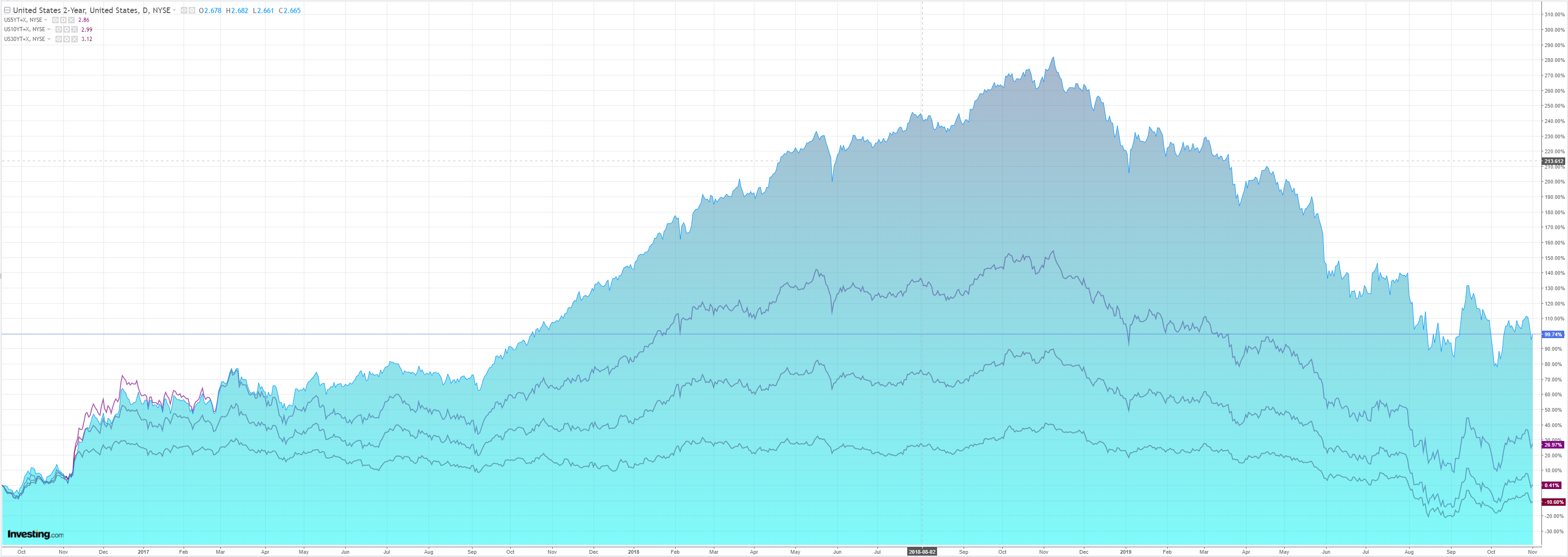

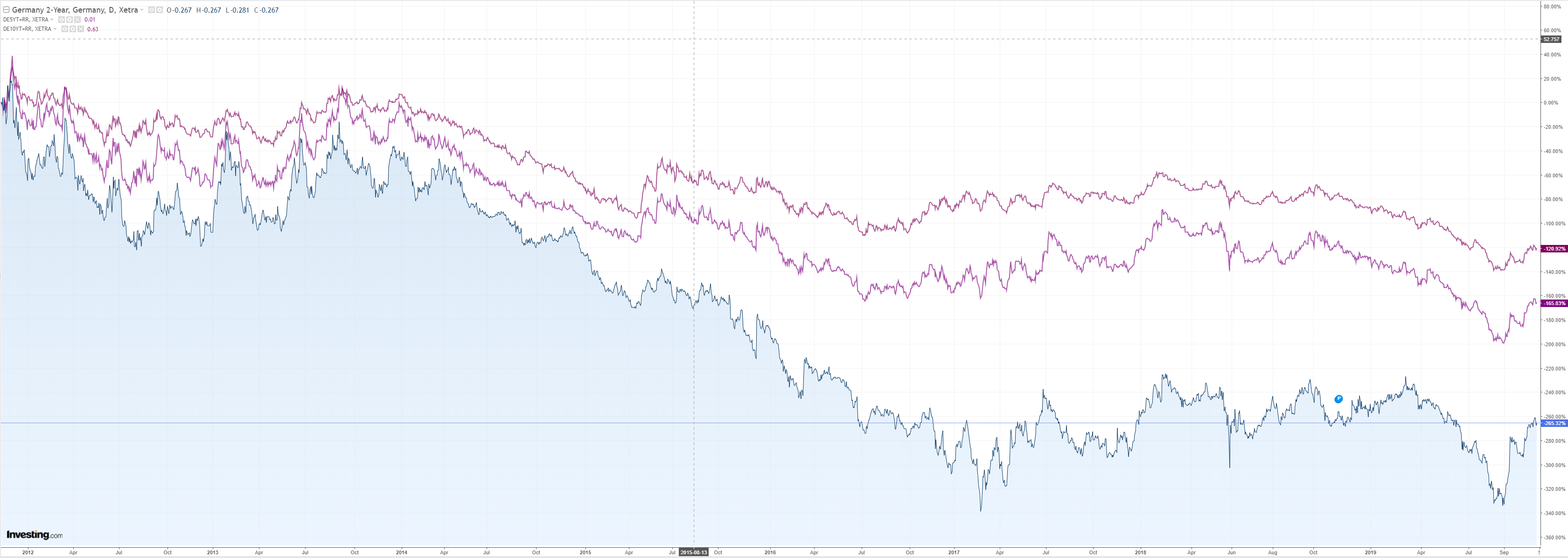

As bonds eased:

Advertisement

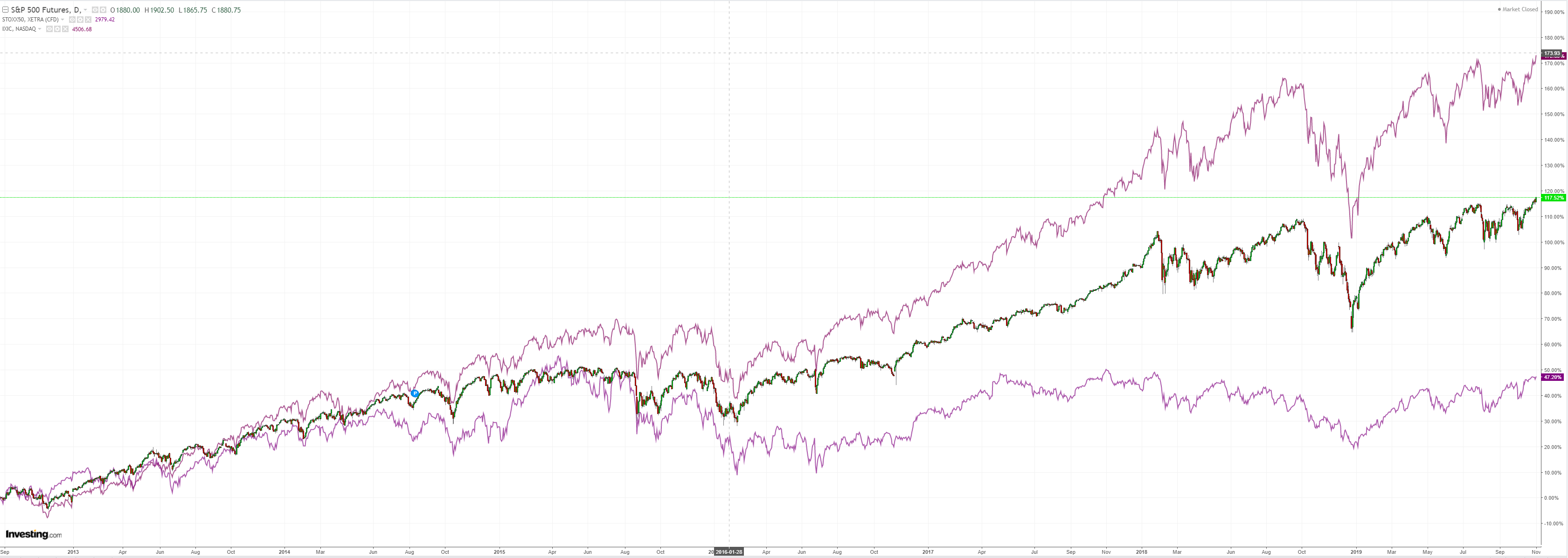

Stocks are now running wild in free air:

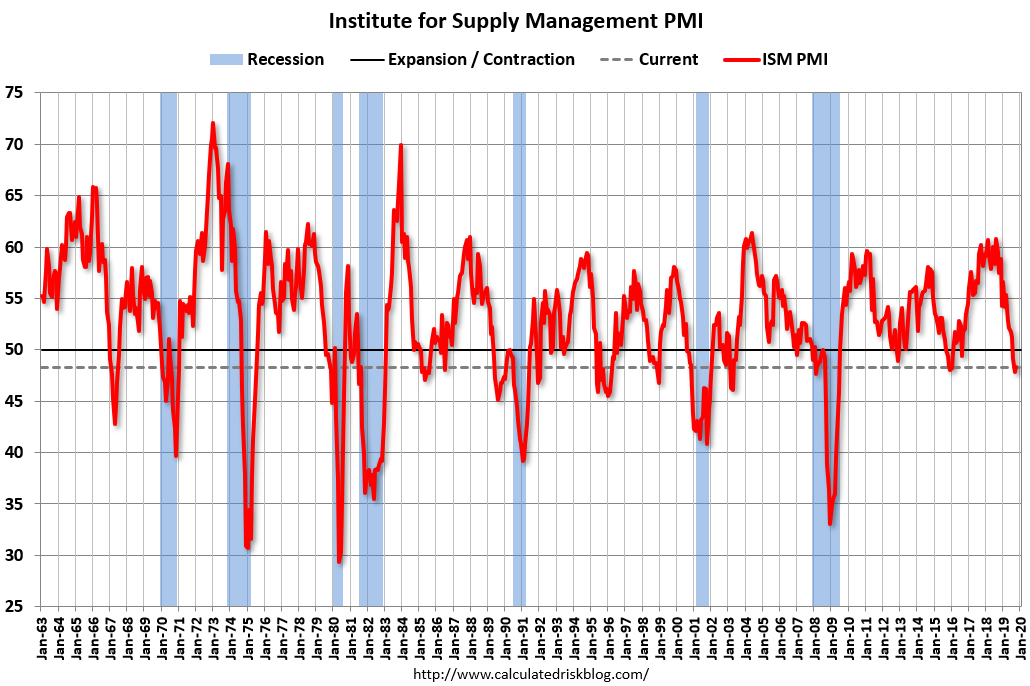

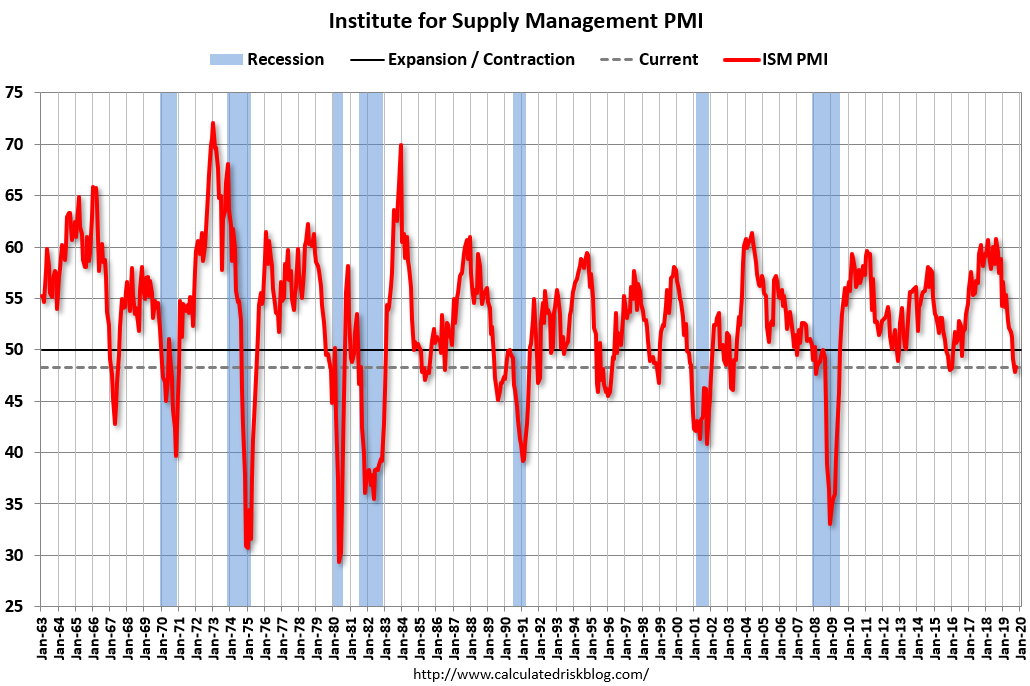

It’s reflation with a perfect combination of strong and weak US data delivering it. The ISM was garbage at 48.3:

Advertisement

The October PMI® registered 48.3 percent, an increase of 0.5 percentage point from the September reading of 47.8 percent. The New Orders Index registered 49.1 percent, an increase of 1.8 percentage points from the September reading of 47.3 percent. The Production Index registered 46.2 percent, down 1.1 percentage points compared to the September reading of 47.3 percent.

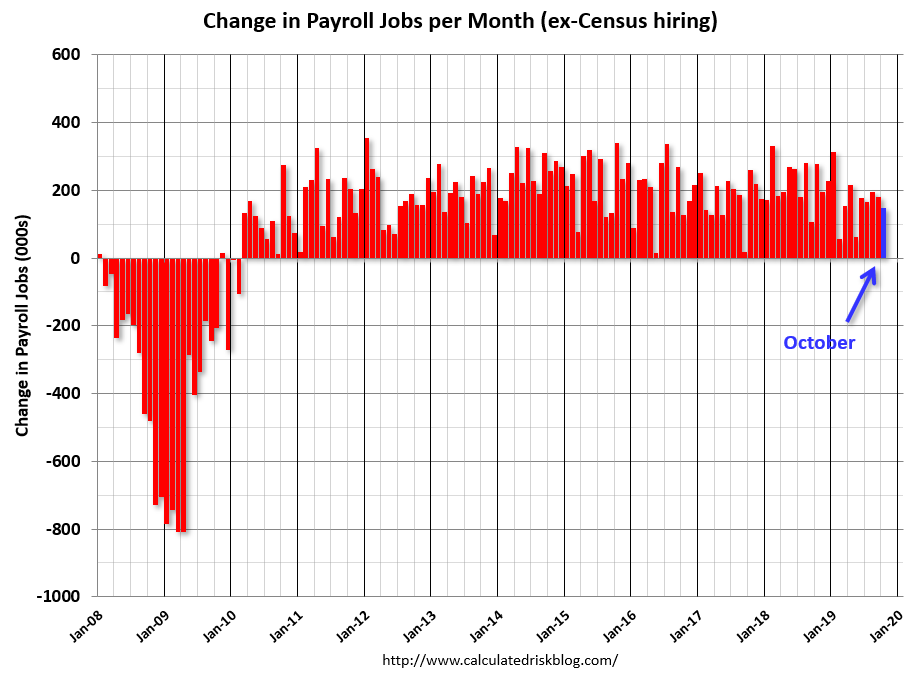

That reasrrured markets the Fed is still dovish. Then, to make metters even better, employment was strong:

Total nonfarm payroll employment rose by 128,000 in October, and the unemployment rate was little changed at 3.6 percent, the U.S. Bureau of Labor Statistics reported today. Notable job gains occurred in food services and drinking places, social assistance, and financial activities. Within manufacturing, employment in motor vehicles and parts decreased due to strike activity. Federal government employment was down, reflecting a drop in the number of temporary jobs for the 2020 Census.

…Federal government employment was down by 17,000 over the month, as 20,000 temporary workers who had been preparing for the 2020 Census completed their work.

…The change in total nonfarm payroll employment for August was revised up by 51,000 from +168,000 to +219,000, and the change for September was revised up by 44,000 from +136,000 to +180,000. With these revisions, employment gains in August and September combined were 95,000 more than previously reported.

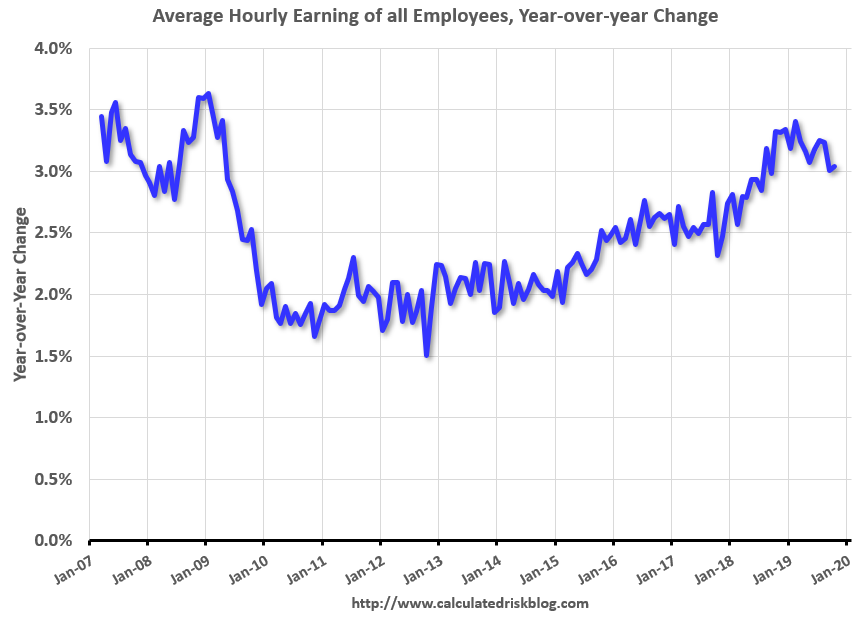

…In October, average hourly earnings for all employees on private nonfarm payrolls rose by 6 cents to $28.18. Over the past 12 months, average hourly earnings have increased by 3.0 percent.

Advertisement

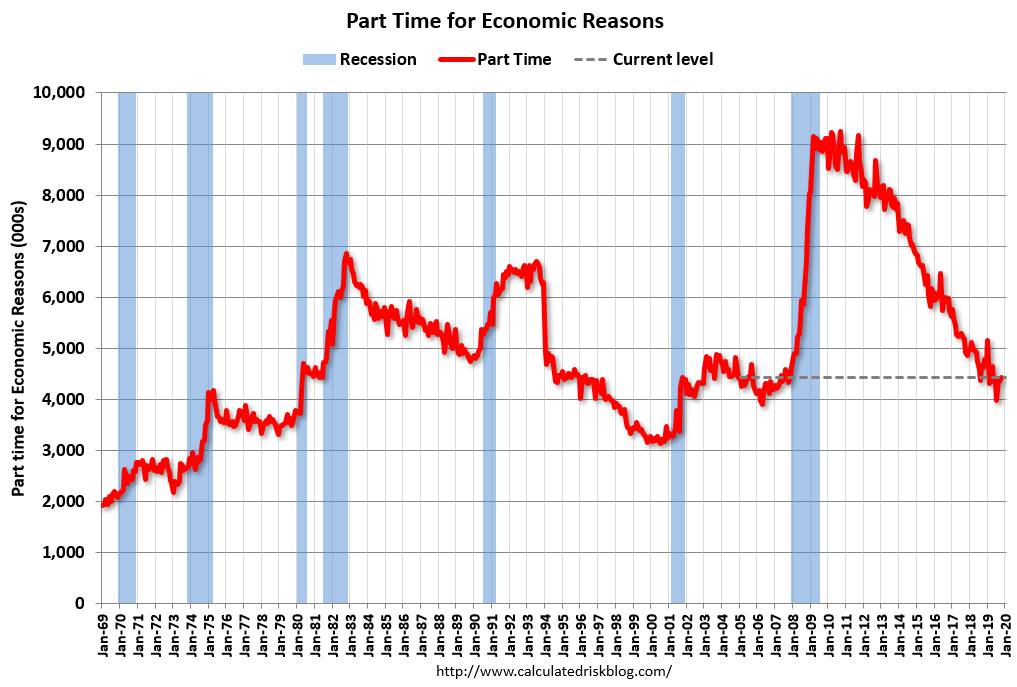

Shadow slack rose a little:

But wages held at 3%:

That’s what you call Goldilocks and stocks did not miss it.

Advertisement

Trade non-deals and Fed cuts have been enough to give markets a reflation bid, even if there is no reflation, notwithstanding that the market can actually create reality in some measure. The strength of this narrative was nicely summed by GaveKal:

In the spring of 2003, with global economic activity depressed by the successive blows of the dot com bust, the aftermath of 9/11, and the Sars scare, Gavekal asked Where Will The Growth Come From? Our answer was that China would become the new locomotive of world growth—a conviction that had led us to move our office from London to Hong Kong. As it turned out, China exceeded even our expectations. Not only did the “Sars stimulus” trigger a massive post-2003 boom in China, but the stimulus-driven rebound in the Chinese economy following the 2008 Lehman bust, and again after the 2015 slowdown, prevented the world economy from experiencing any protracted slump in growth.

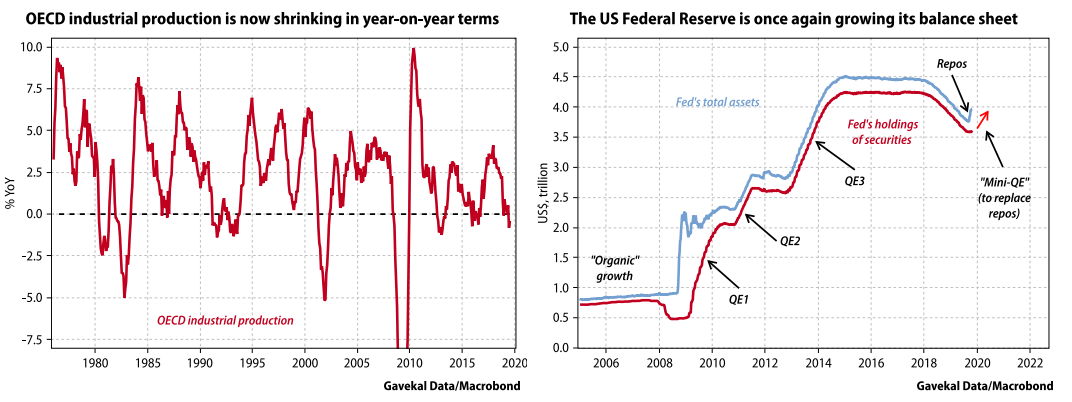

Now, however, the days when China could be counted upon to gear up its balance sheet and pull global growth up by its bootstraps are coming to an end. And as global activity slows—OECD industrial production is now shrinking again in year-on-year terms (see the left-hand chart overleaf)—investors are once again asking “where will the growth come from?”

Today, for a number of reasons, the answer to their question may be “the emerging markets.”

• A shifting global political landscape. A couple of weeks ago, Donald Trump indicated that he was willing to declare “victory” in his trade war with China, and move on (see Trump’s Unreal Deal With China). Shortly after, the European Union and the British prime minister managed to agree a Brexit deal that made sense for both parties. These events removed two major political risks from the global system and so have been bearish both for US treasuries and for the US dollar. And by reducing funding costs and sharpening risk appetite, a weak US dollar is usually good news for emerging markets.

• A major shift in monetary policy. Until last month, the US Federal Reserve was still signaling it would keep its balance sheet stable. Following dislocations in the US repo market, it ditched this resolution. Instead, the Fed is now expanding its balance sheet again (see The Fed Goes On The Offensive). This shift is US dollar-bearish (see US Dollar Under Fire), which should be good news for emerging markets.

• China is back to injecting liquidity and easing policy. The days of massive stimulus are long gone. But the leadership is making sure that Chinese growth does not crater. And the emerging market cycle is

typically a big beneficiary of Chinese stimulus.

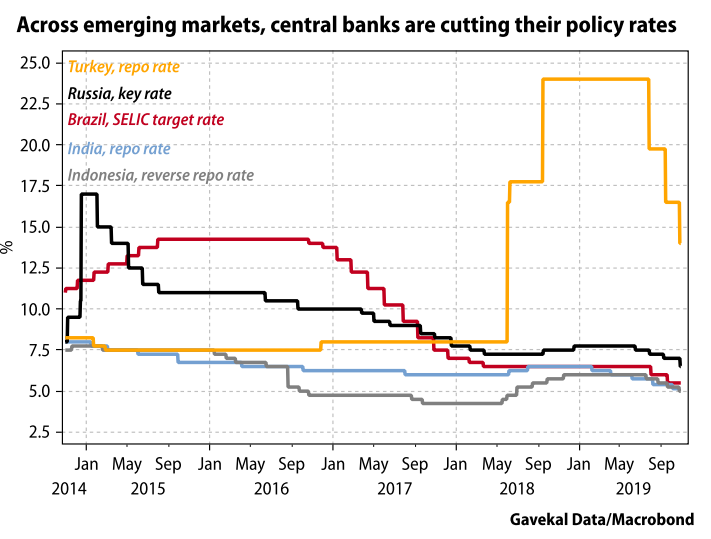

The combination of a topping-out US dollar and Chinese stimulus would usually be enough to make a cyclical case for emerging markets. But it appears something more is happening. Almost anywhere you look across the emerging markets, you find either significant fiscal reforms (Brazil, India), important regulatory changes (Brazil, India, Indonesia), or significant interest rate cuts (India, Indonesia, Russia etc.). In short: stimulus on the fiscal side, stimulus on the regulatory side, and stimulus on the monetary policy front.

Admittedly, the impact of fiscal stimulus may be limited in countries such as India or Indonesia, where too few people actually pay taxes. However, the other side of the coin is that lower interest rates will have much more of a stimulative impact than they do in the developed economies. Cutting interest rates from -40bp to -50bp does little except make life impossible for banks, insurance companies and pension funds. But cutting rates from 7% to 5% promotes consumption, capital spending, and increased risk taking.

Considering all this, why is it that investors have yet to get excited about the growth prospects in emerging markets? One possible explanation is that over the past decade, investors have got used to looking at emerging markets through the prism of China. Given the size of the Chinese economy and the impact of the Chinese economic cycle on other emerging market peers, this bias makes sense. In recent years, China and the emerging markets have indeed tended to move as one. As a result, given the modest outlook for Chinese growth, most investors seem to have come to the conclusion that the outlook for other emerging markets just isn’t that compelling

This conclusion may prove to be both hasty and simplistic. In a world in which the US dollar is no longer rising (whether because of abating trade war risk, an easing Fed, or reduced Brexit dangers), emerging markets gain a lot of policy room. Today, most of them are using this policy room to adopt very stimulative policies.

Back in 2003, few investors would have believed that China would contribute half of all global GDP growth over the following 10 or so years. Yet over the past decade, roughly half of global growth was indeed delivered by China, a quarter by other emerging markets, and a quarter by the advanced economies.

Given the policy choices currently unfolding across these three separate zones, would it be a such stretch to imagine that over the next decade half of global growth could come from ex-China emerging markets, a quarter (or less?) from China, and a quarter from the developed economies?

Given the macro backdrop, this could easily prove the path of least resistance: over the next decade, with the combined growth of Brazil, India, Indonesia, Russia, Vietnam and others outpacing growth in China, and probably in the developed economies too. Fortunately for investors, this increasingly likely scenario is nowhere near being priced in by currency values, bond markets, commodity markets, or even by local emerging market equity markets.

It’s a persuasive narrative in some ways. So long as the USD falls it could come true before we see any kind of end of cycle accident. In turn, that hangs on a number of factors including a European rebound, trade non-deals turning into real deals that wind back tarrifs, and more Fed cuts than easing elsewhere. I am not confident on any of the three, for now.

Advertisement

Hence I am not yet convinced that DXY is headed for further falls beyond this narrative as a short term pain trade. DXY can correct another 5% before its uptrend is even threatened.

Thus for now I see the GaveKal vision more as the likely dynamic of the enxt cycle. Before we get there I still fear we will see greater volatility and more DXY safe haven buying.

That said, this is looking more like a tradaeble rally for the AUD as the market pretends that the EM reflation narrative is already a reality.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

{kind=link}