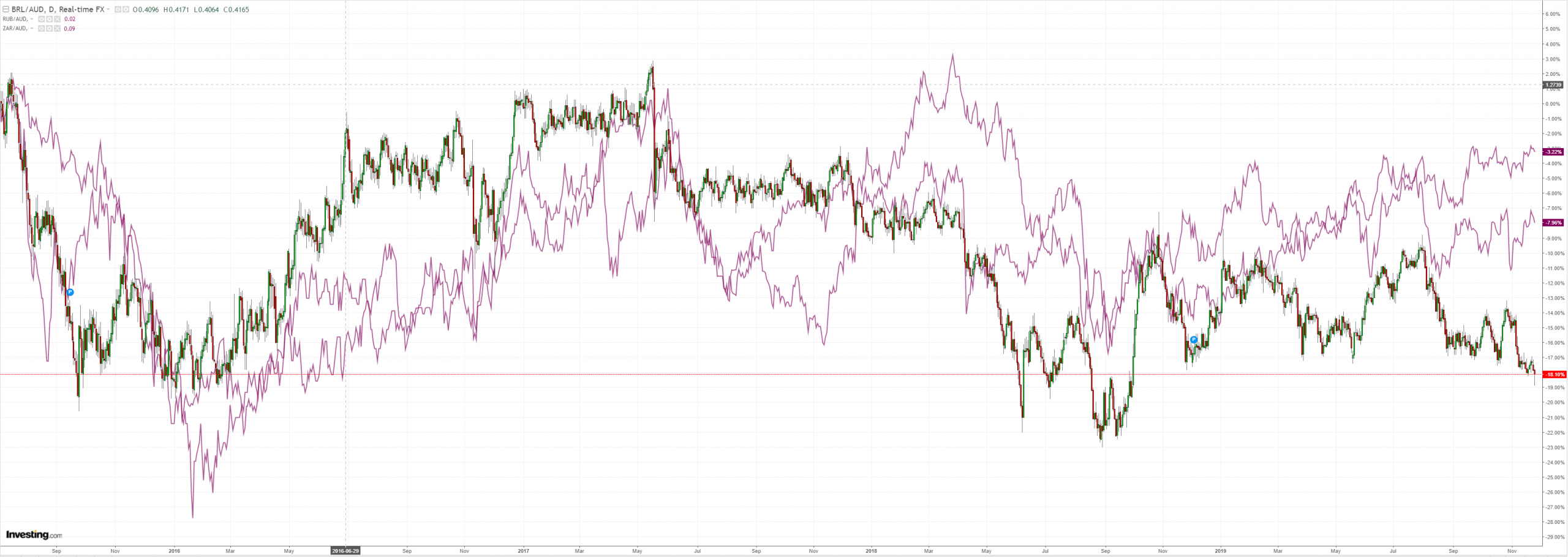

Espeically Australia as the RBA targets a 25bps cash rate:

Stocks kept on going:

Advertisement

Westpac has the wrap:

Event Wrap

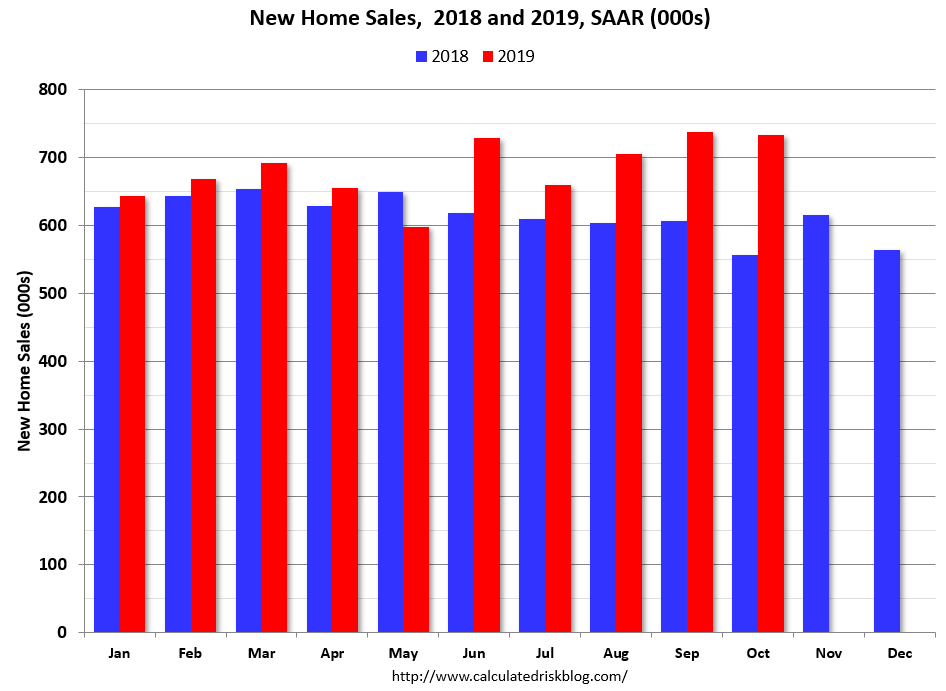

US new home sales for Oct beat expectations at 733k (vs est. 705k), while Sep sales were revised up to 738k from 701k. CoreLogic Sep. house prices rose +3.2%y/y (est. +3.3%, prior revised to 3.1%y/y from 3.2%y/y). Richmond Fed. manufacturing survey fell to -1 from 8 and disappointed estimates of +5. New orders and employment components fell. The Conference Board’s consumer confidence survey fell to 125.5 (vs est. 127.0, prior 126.1) but remains firm and close to its cycle highs. Despite the fall in the present situation measure (166.9 from 173.5) the expectations measure notably rose to 97.9 from 94.5. Wholesale inventories for Oct were in line with expectations at +0.2%m/m, though Sep was revised to -0.7%m/m from -0.4%m/m.

RBA Governor Lowe delivered a speech plus Q&A on Unconventional Monetary Policy, saying quantitative easing would be considered if the cash rate fell to 0.25% but considered that scenario to be “extremely unlikely”. He also said government bond purchases would be their preferred form of quantitative easing.

Fed Chair Powell repeated his signal that interest rates are on hold for now: “At this point in the long expansion, I see the glass as much more than half full … with the right policies, we can fill it further, building on the gains so far and spreading the benefits more broadly to all Americans.”

Event Outlook

NZ: The RBNZ’s Financial Stability Review, including Q&A, is released, with most interest likely to be on (1) any changes to LVR restrictions (we don’t expect them to be relaxed), and (2) any discussion of the proposed bank capital changes. Datawise, Oct trade balance is expected to be -$1bn.

Australia: Q3 construction work is expected to decline by 1.0%.

US: Q3 GDP 2nd estimate follows the 1st estimate of 1.9% annualised growth. Oct durable goods orders are anticipated to decline 0.9% following a 1.2% decrease in Sep. Oct personal income and personal spending are seen to rise 0.3% while core PCE deflation holds at an annual pace of 1.7%yr. The Federal Reserve Beige Book is released.

Check out the booming US residential construction market:

“Sales of new single‐family houses in October 2019 were at a seasonally adjusted annual rate of 733,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 0.7 percent below the revised September rate of 738,000, but is 31.6 percent above the October 2018 estimate of 557,000.”

Advertisement

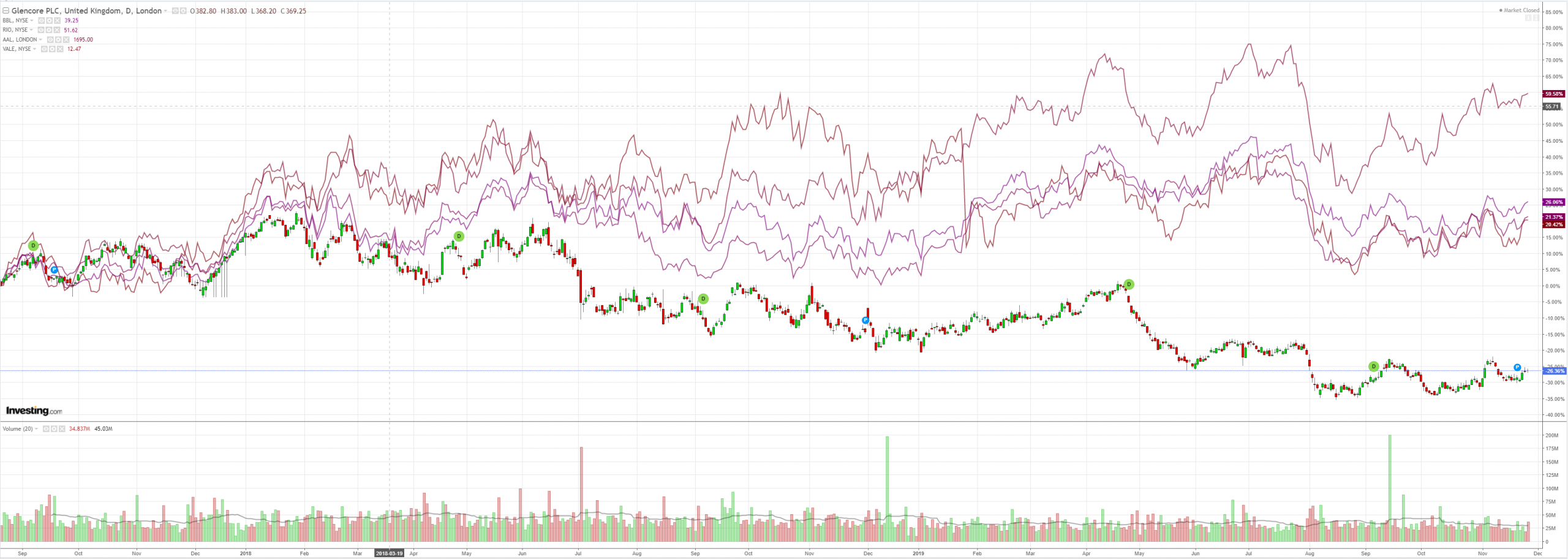

With associated reflations:

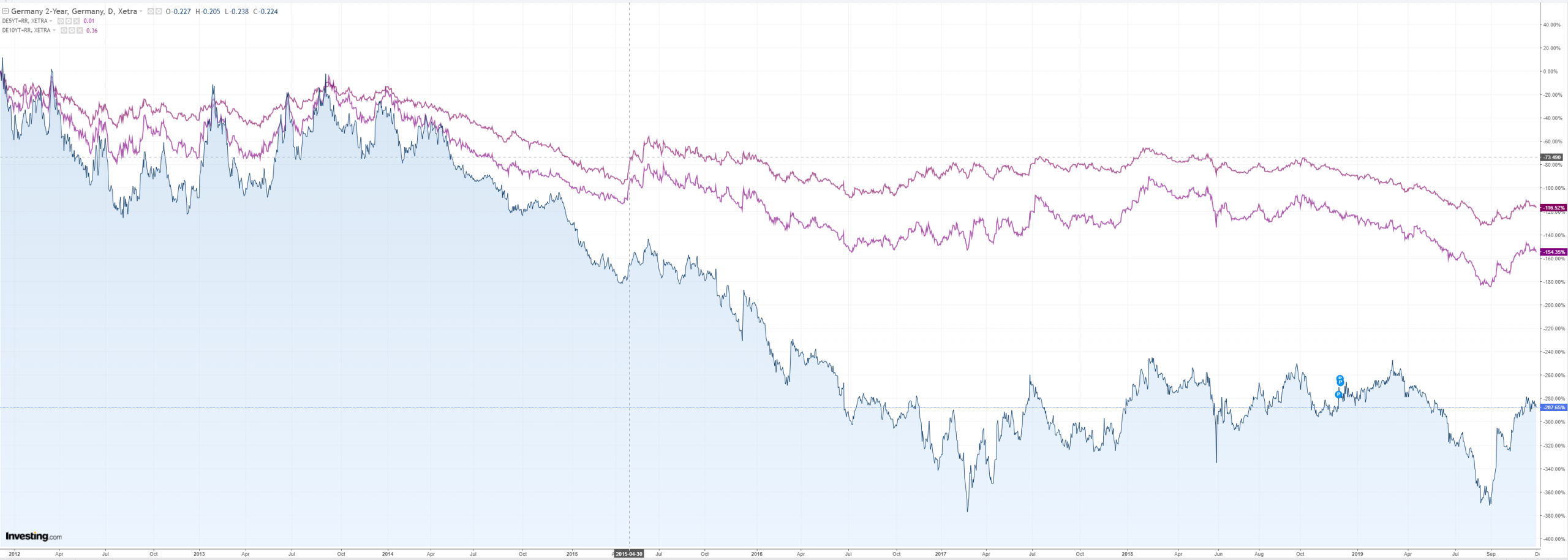

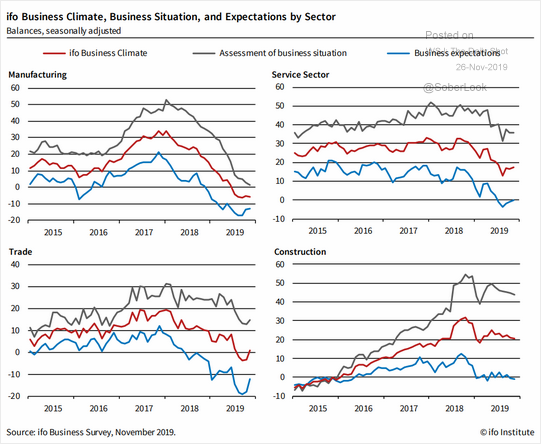

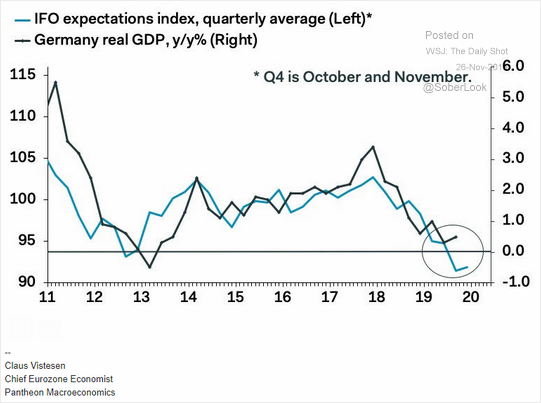

Versus still fading European construction:

Advertisement

It’s still all the way with ther USA for stocks and forex with the immediate implication that the Australian dollar simply can’t get off the matt.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.