DXY was up last night as EUR sank:

The Australian dollar closed at new lows versus the USD:

It did better versus EMs:

Gold is fading again:

Oil hanging on:

Metals want no part in the rally:

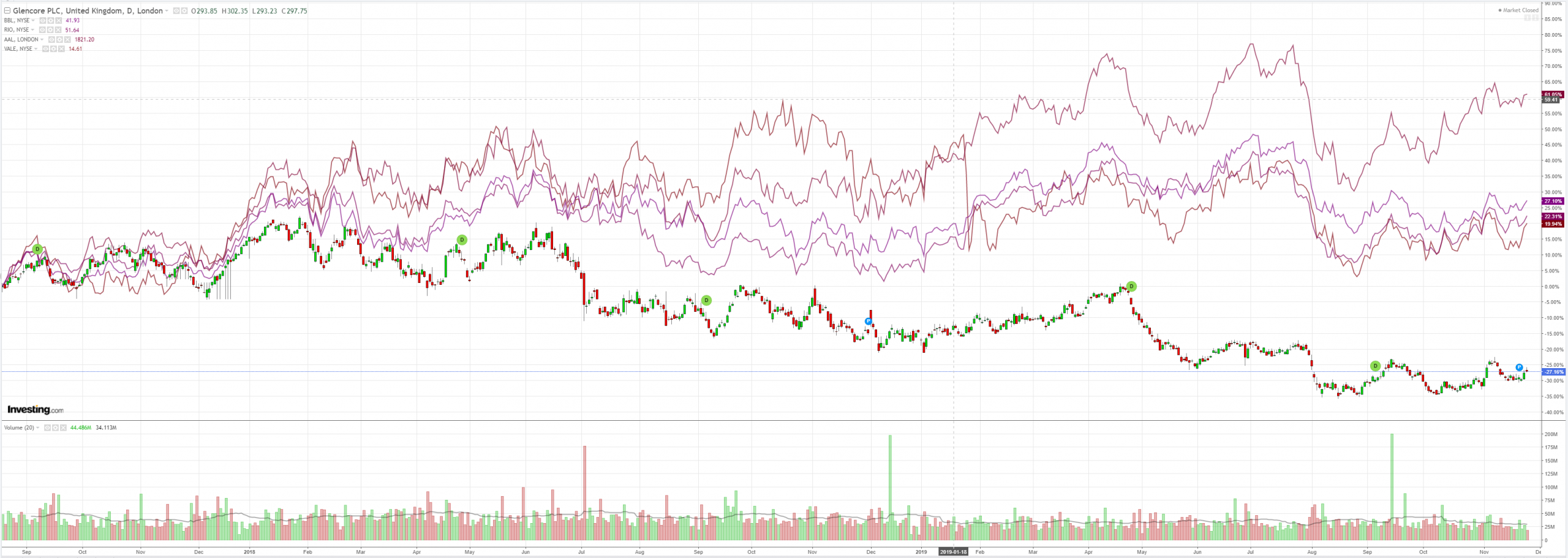

Miners joined anyway:

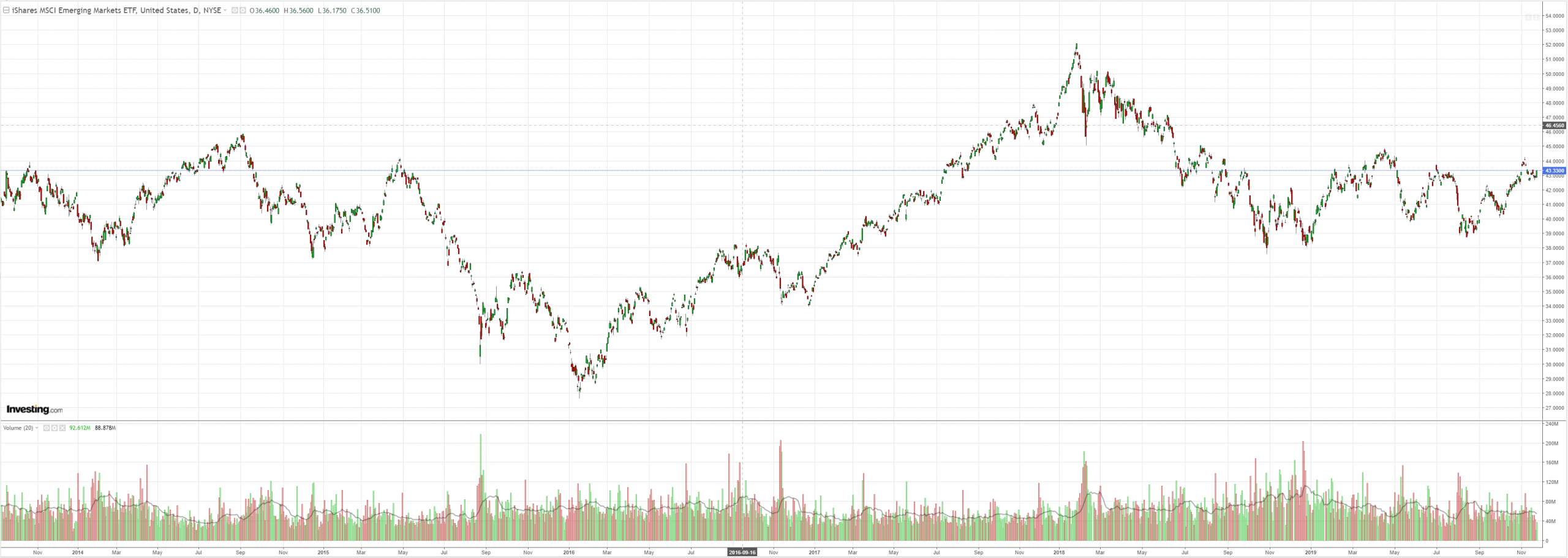

EM stocks jumped:

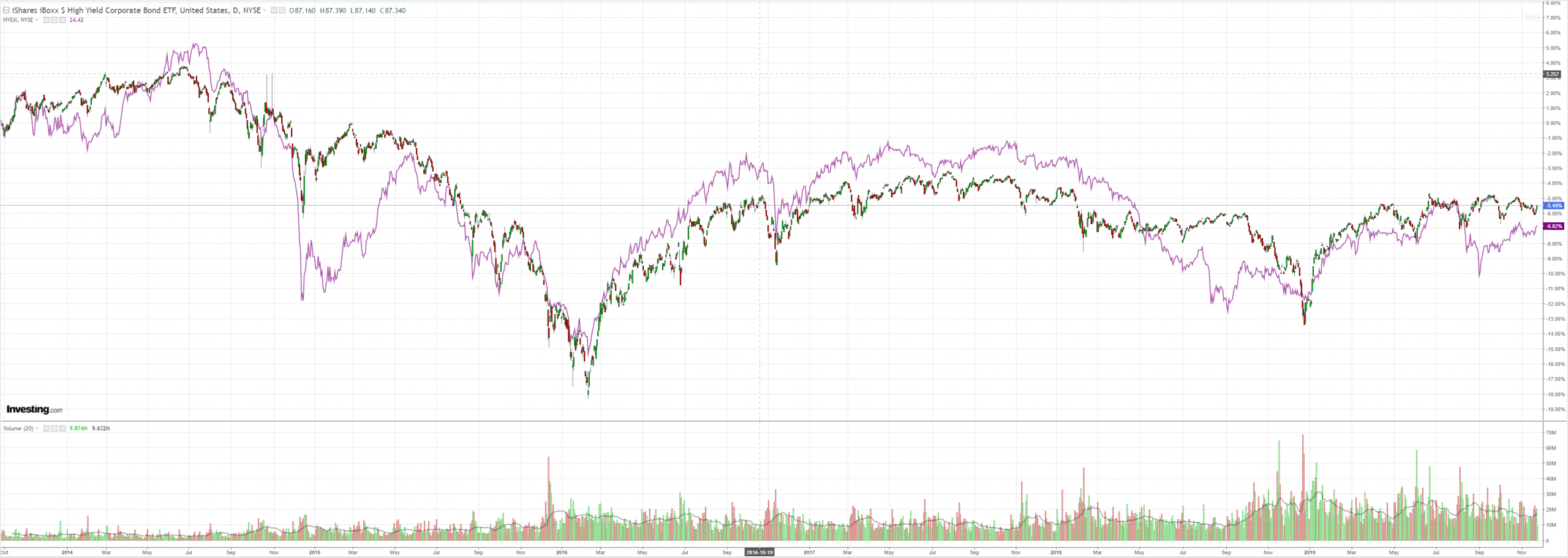

Junk too:

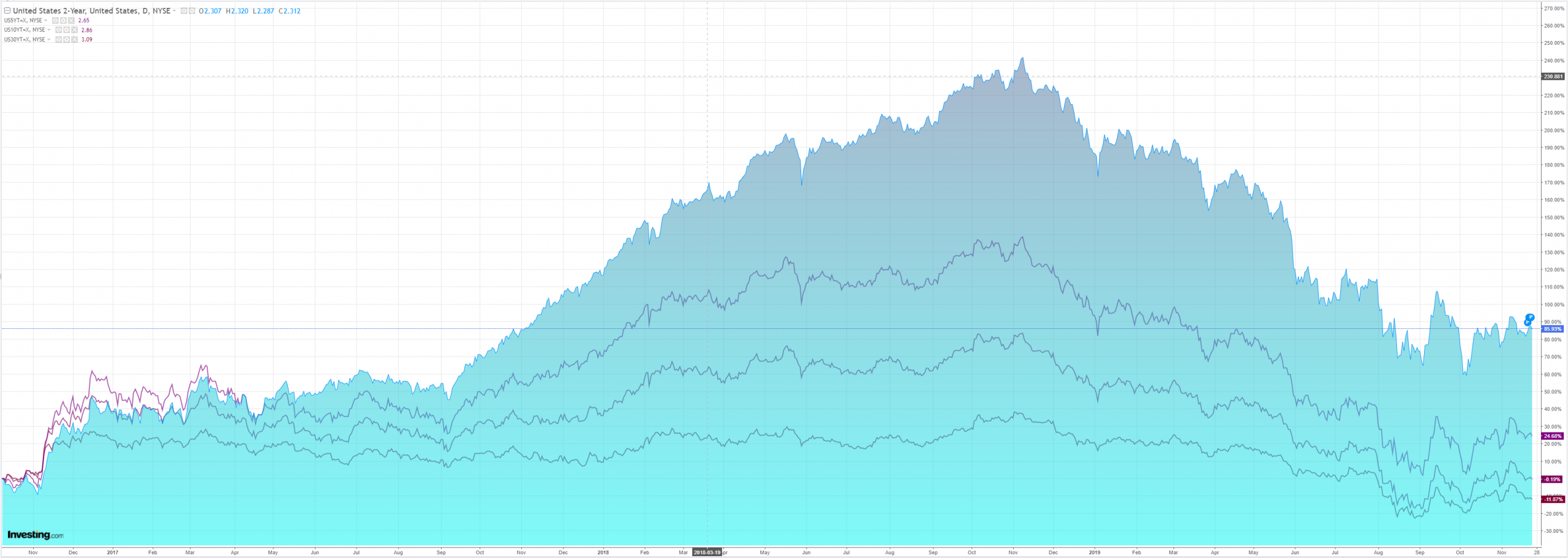

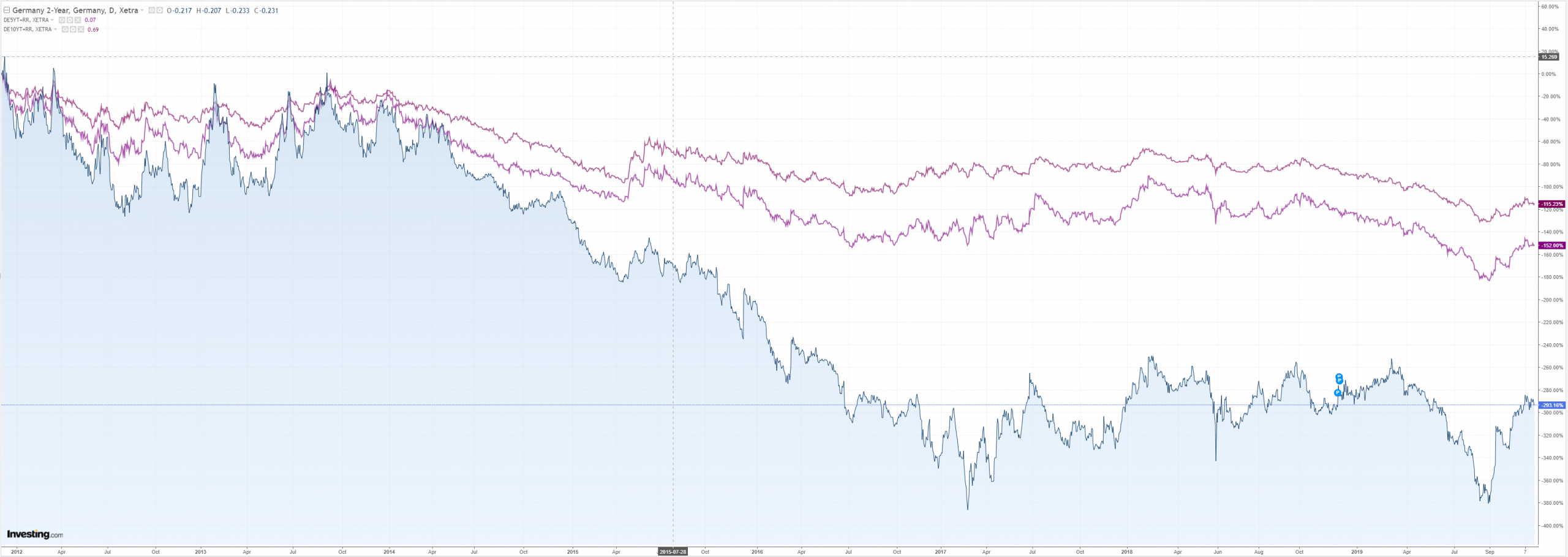

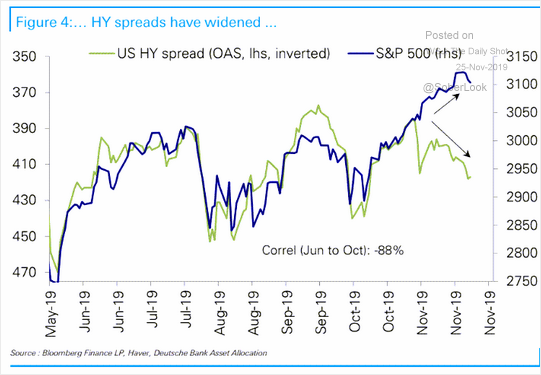

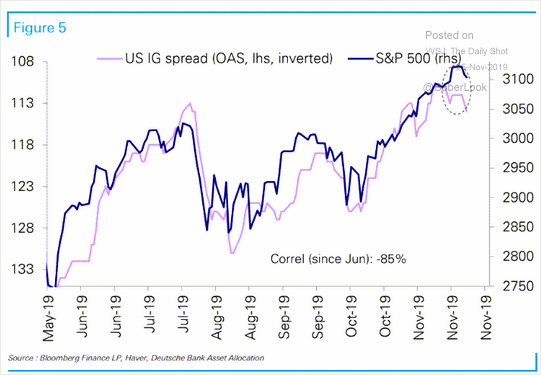

All bonds were bid:

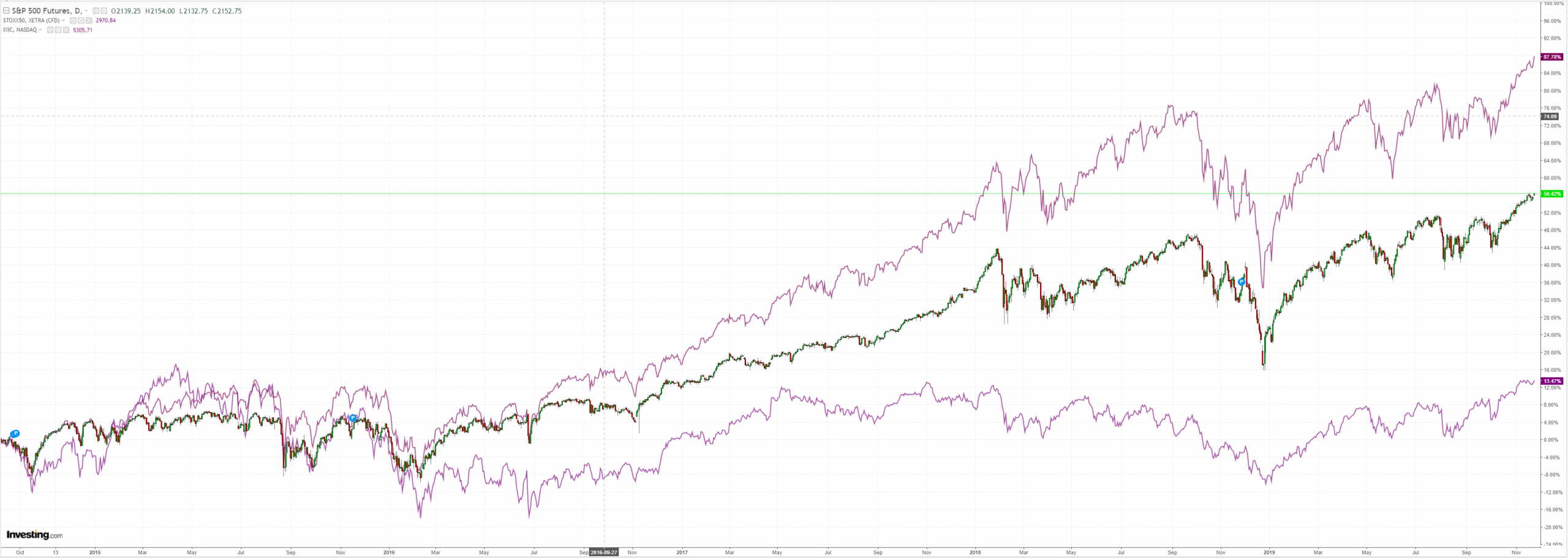

Which helped shove stocks to record highs:

Westpac has the wrap:

Event Wrap

Chicago Fed.’s Oct. National Activity Index slipped to -0.71 (est. -0.20, prior -0.45). Although profiles were generally softer, the index remains above the April low and within the range since 2010.

Dallas Fed.s Nov. regional survey contracted again but at -1.3 was less than estimates (-3.8, prior -5.1). The majority of components remained negative or softened, though the six month future profile did lift (General business 7.3 from 2.4 in Oct.).

Germany’s Nov. IFO business survey edged firmer but failed to lift as much as mild market estimates. The Climate Index rose to 95.0 (est. 95.0, prior 94.7) but Expectations only reached 92.1 (est. 92.5, prior 91.6).

Event Outlook

NZ: Q3 retail sales is expected to have risen 0.6%, vs 0.2% inQ2.

Australia: RBA Governor Lowe speaks on “Unconventional Monetary Policy: Some Lessons from Overseas” at the Annual ABE Dinner, Sydney 8:05pm. RBA Deputy Governor Debelle speaks on “Employment and Wages” at the 2019 ACOSS National Conference, 10:50 am.

Europe: ECB Chief Economist Lane speaks in London.

US: Oct new home sales and Sep home price data are released. Nov Conference Board consumer confidence is expected to edge up to 127.0. Fed Chair Powell speaks on “Building on the Gains from the Long Expansion” (11am Sydney time). Other Fedspeak involves Brainard on the Fed’s policy framework review.

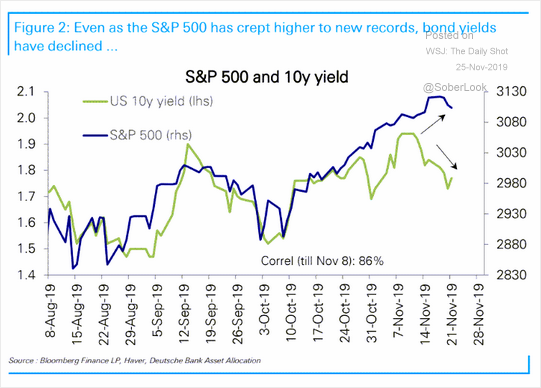

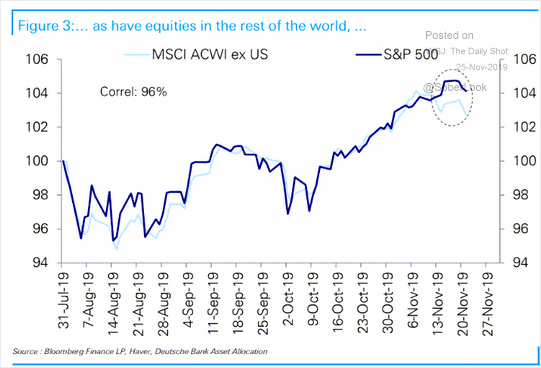

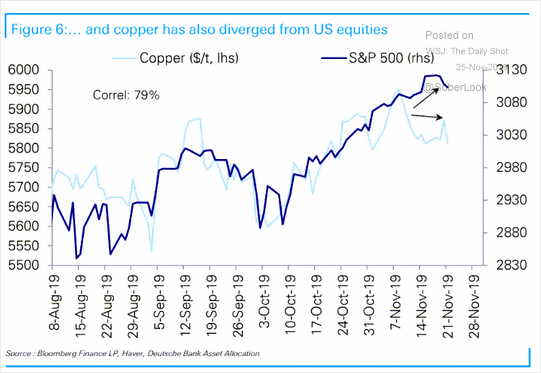

US stocks are flying clear of all growth correlations. Versus bonds:

Versus other stocks:

Versus Dr Copper:

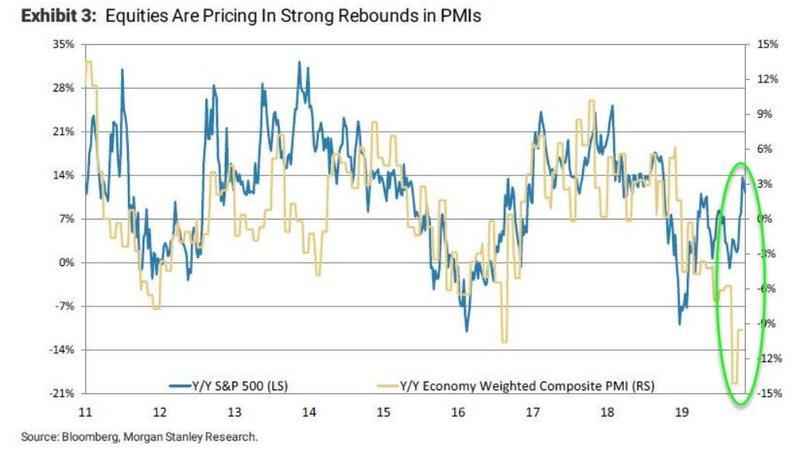

Versus PMIs:

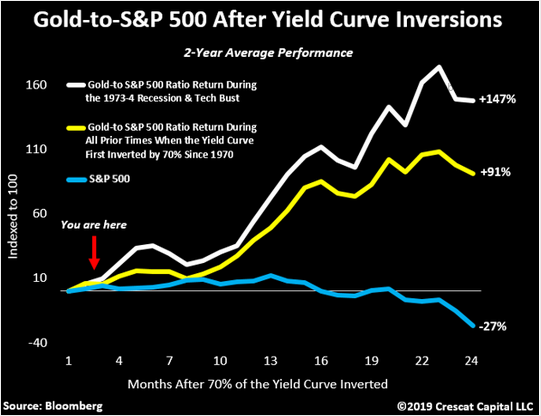

It won’t be long before folks start mentioning the word “bubble” again.

Ever since 2011, the Australian dollar has struggled to follow these risk on rallies in US stocks, except from 2016 to 2018:

The reason is simple. When the global economy is led by US strength then DXY rises, EMs and commodities struggle and so does the AUD.

This has become entrenched with America First which has cut off some material amount of spillovers from a strong US consumer to Chinese exports. In turn, Europe’s export machine struggles as well.

America First still makes US stocks are the only game in town and the Australian dollar is a forgotten backwater while it persists.

The MB Fund and MB Super is long international stocks that benefit from a falling Australian dollar.

The information on this blog contains general information and does not take into account your personal objectives, financial.