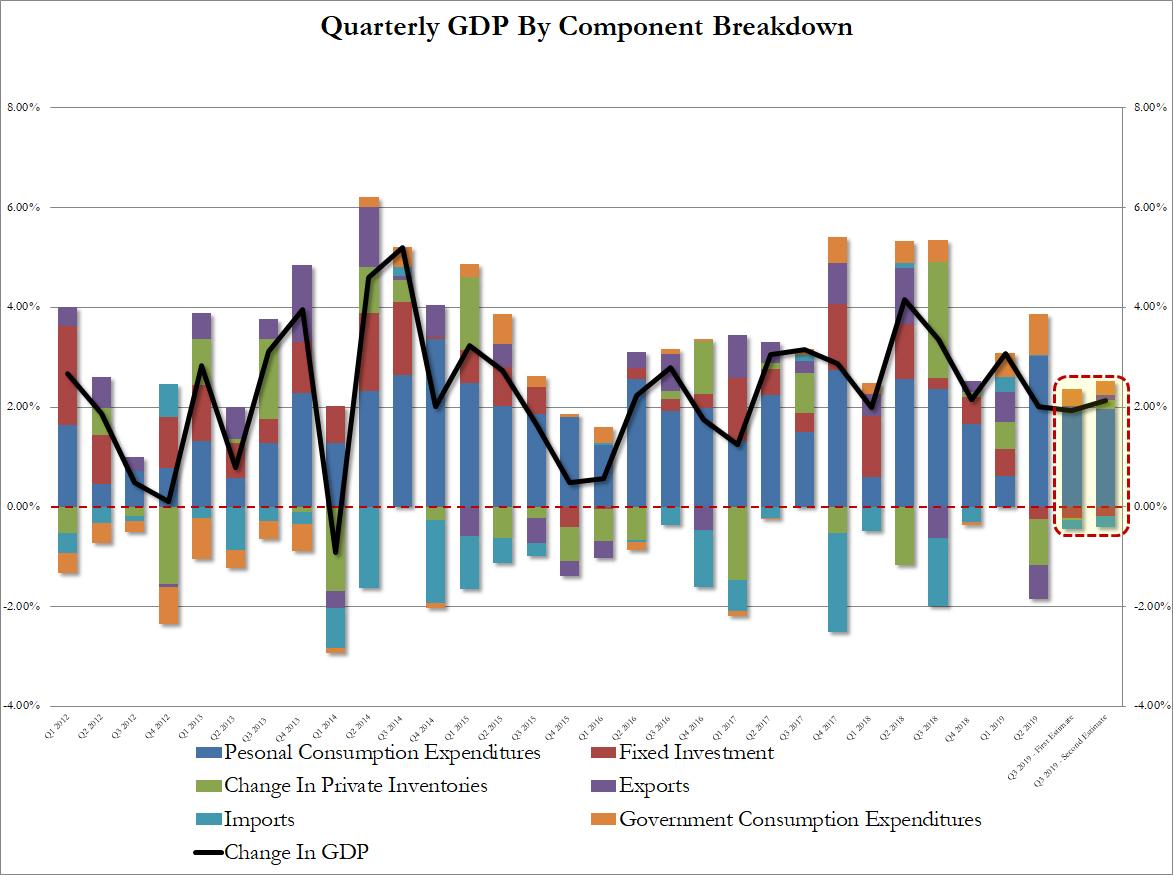

US data: the update (second release) to US 3Q GDP rose to 2.1%y/y from 1.9%y/y, with solid personal consumption but a lift in inventories which could detract from 4Q GDP. Oct. durable goods orders rose a solid +0.6%m/m (vs est. -0.9%), the important ex-transport orders measure also rising +0.6%m/m (vs est. +0.1%m/m). Capital goods orders were also stronger than estimated (non-defence/ex-air rising 0.8%m/m, est. -0.2%m/m)

Chicago PMI rose in line with estimates but remains weak at 46.3 (est. 47.0, prior 43.2). The employment component was weak, though the decline in new orders was more subdued.

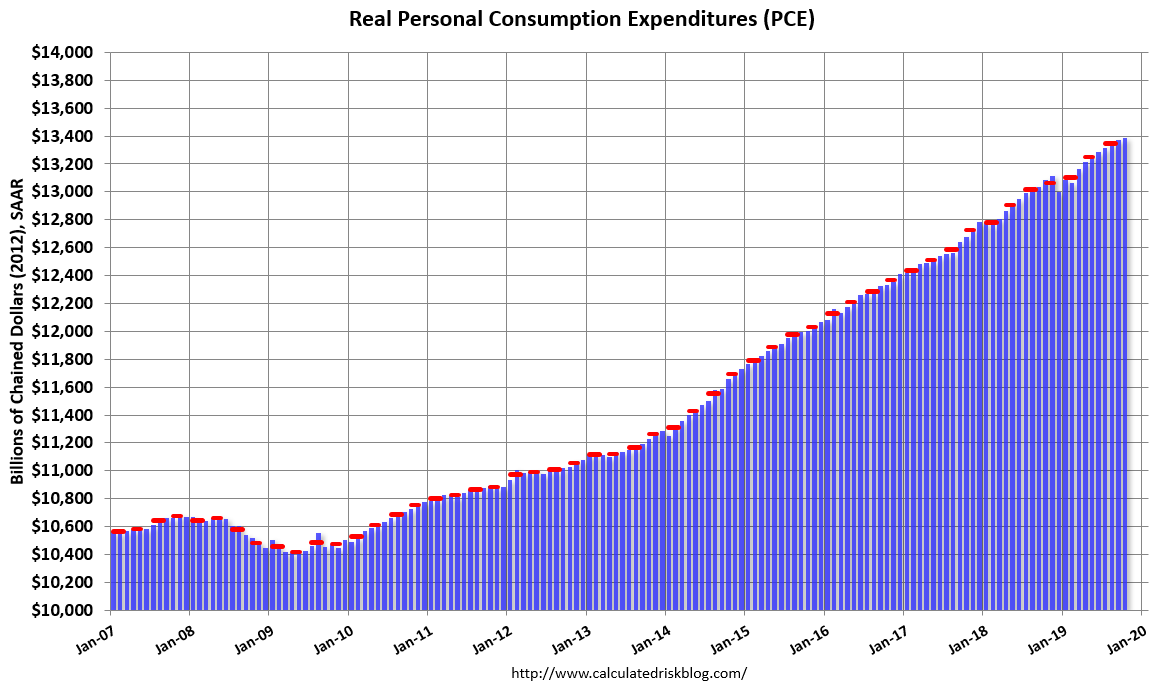

Oct. personal income was disappointing at flat m/m (est. +0.3%m/m) and with spending at +0.3% (as est.) the savings ratio slipped to 7.8% from 8.1%. Core PCE inflation was also disappointing at +1.6%y/y (est. +1.7%y/y).

Oct. pending home sales undershot estimates and fell 1.7%m/m (est. +0.2%m/m), though NAR continued to find positives in the release suggesting that a continuation in low housing inventory had impacted the data despite a favourable economic landscape.

Event Outlook

NZ: Business confidence (ANZ) rebounded in Oct but remains at a very weak level, while the own activity indicator (a proxy for actual GDP) slipped into contractionary territory.

Australia: Q3 private new capex is expected to be flat. Westpac is forecasting a 0.5% decline driven by a 1.5% pull-back in equipment. 2019/20 capex plans estimate 4 is anticipated by Westpac to be in the order of $120bn.

Europe: Oct M3 money supply is expected to hold at 5.5%yr. Nov European Commission surveys are expected to show economic confidence and the business climate indicator edging up from modest levels. Nov German CPI is released ahead of the euro area release on Friday.

US: It is the Thanksgiving public holiday.

US data was good overall. GDP was revised to solid:

Real gross domestic product (GDP) increased at an annual rate of 2.1 percent in the third quarter of 2019, according to the “second” estimate released by the Bureau of Economic Analysis. In the second quarter, real GDP increased 2.0 percent.

The GDP estimate released today is based on more complete source data than were available for the “advance” estimate issued last month. In the advance estimate, the increase in real GDP was 1.9 percent. With the second estimate for the third quarter, upward revisions to private inventory investment, nonresidential fixed investment, and personal consumption expenditures (PCE) were partially offset by a downward revision to state and local government spending.

Advertisement

Pending home sales eased but remain up year on year:

Pending home sales retreated in October, taking a slight step back after two prior months of increases, according to the National Association of Realtors®. The Northeast experienced a minor uptick last month, but the other three major U.S. regions reported declines in month-over-month contract activity. However, pending home sales were up nationally and up in all regions compared to a year ago.

The Pending Home Sales Index (PHSI), a forward-looking indicator based on contract signings, fell 1.7% to 106.7 in October. Year-over-year contract signings jumped 4.4%. An index of 100 is equal to the level of contract activity in 2001.

PCE was soft but the trend is fine:

Advertisement

Personal income increased $3.3 billion (less than 0.1 percent) in October according to estimates released today by the Bureau of Economic Analysis. Disposable personal income (DPI) decreased $12.6 billion (-0.1 percent) and personal consumption expenditures (PCE) increased $39.7 billion (0.3 percent).

Real DPI decreased 0.3 percent in October and Real PCE increased 0.1 percent. The PCE price index increased 0.2 percent. Excluding food and energy, the PCE price index increased 0.1 percent.

Durable goods (capex) jumped after a weak run:

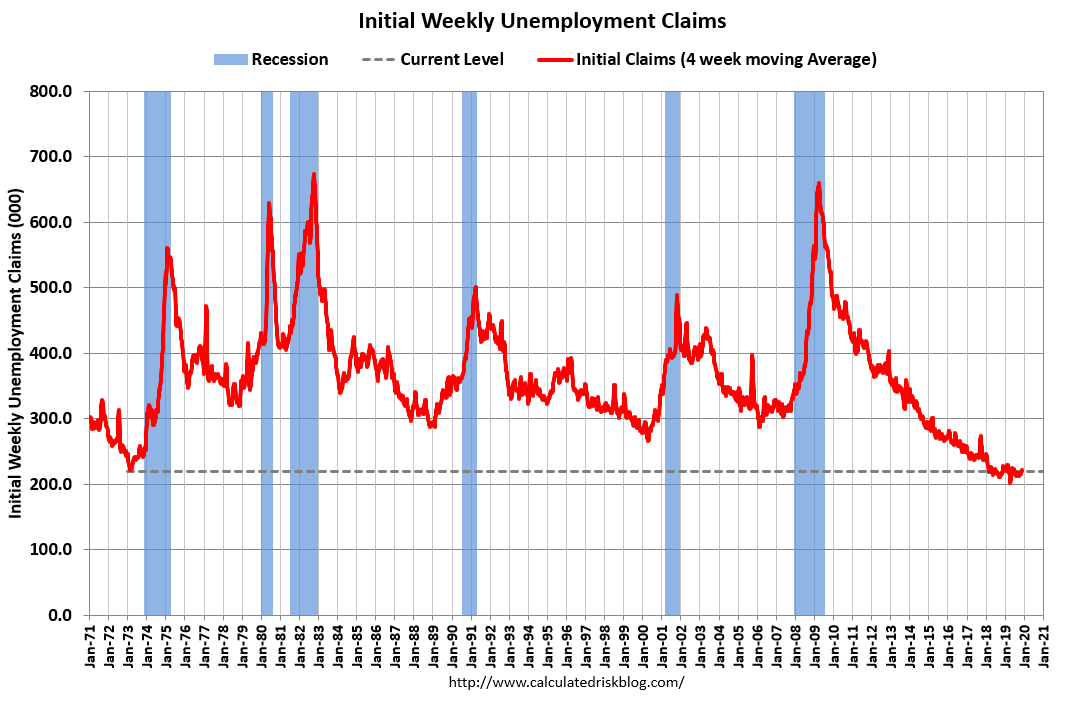

Unemployment claims are still low:

In the week ending November 23, the advance figure for seasonally adjusted initial claims was 213,000, a decrease of 15,000 from the previous week’s revised level. The previous week’s level was revised up by 1,000 from 227,000 to 228,000. The 4-week moving average was 219,750, a decrease of 1,500 from the previous week’s revised average. The previous week’s average was revised up by 250 from 221,000 to 221,250.

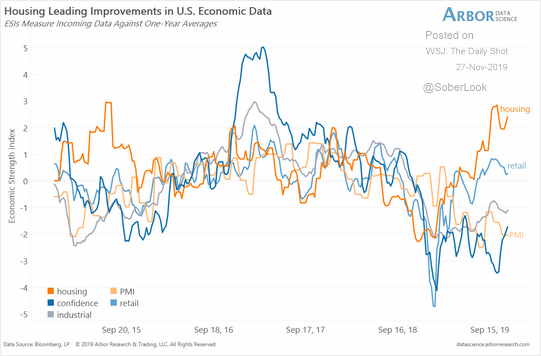

The bounce is led by housing:

Advertisement

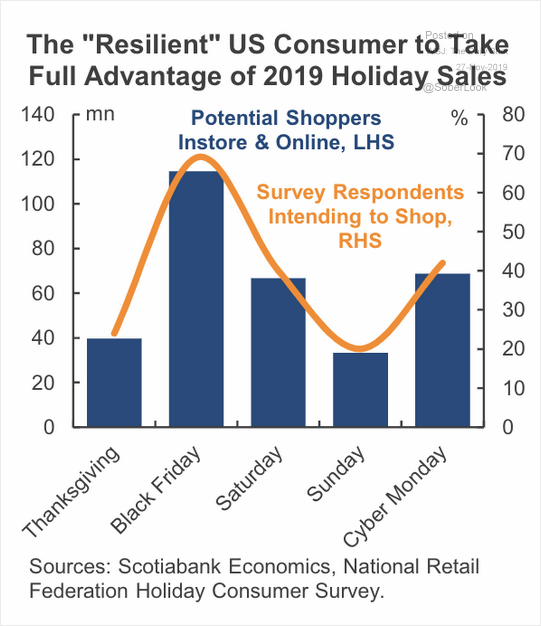

With consumers on its coatails:

No doubt aided by stocks.

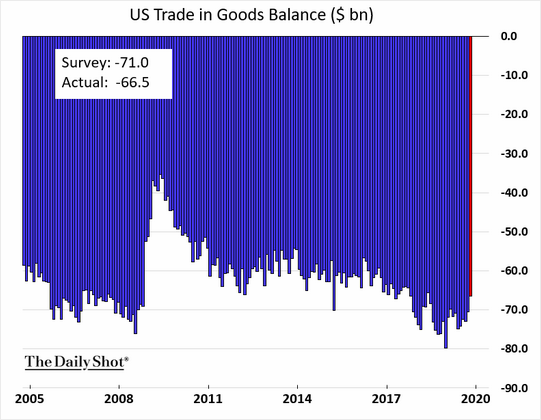

The problem is, the bounce no longer fans out into China via imports. Indeed, since the tariff frontloading, the US trade deficit has been declining:

Advertisement

Very unsual during a US consumer boom. Helped by oil but also imports killed by tariffs meaning the mercantilsits in China and then Europe keeps slowing anyway.

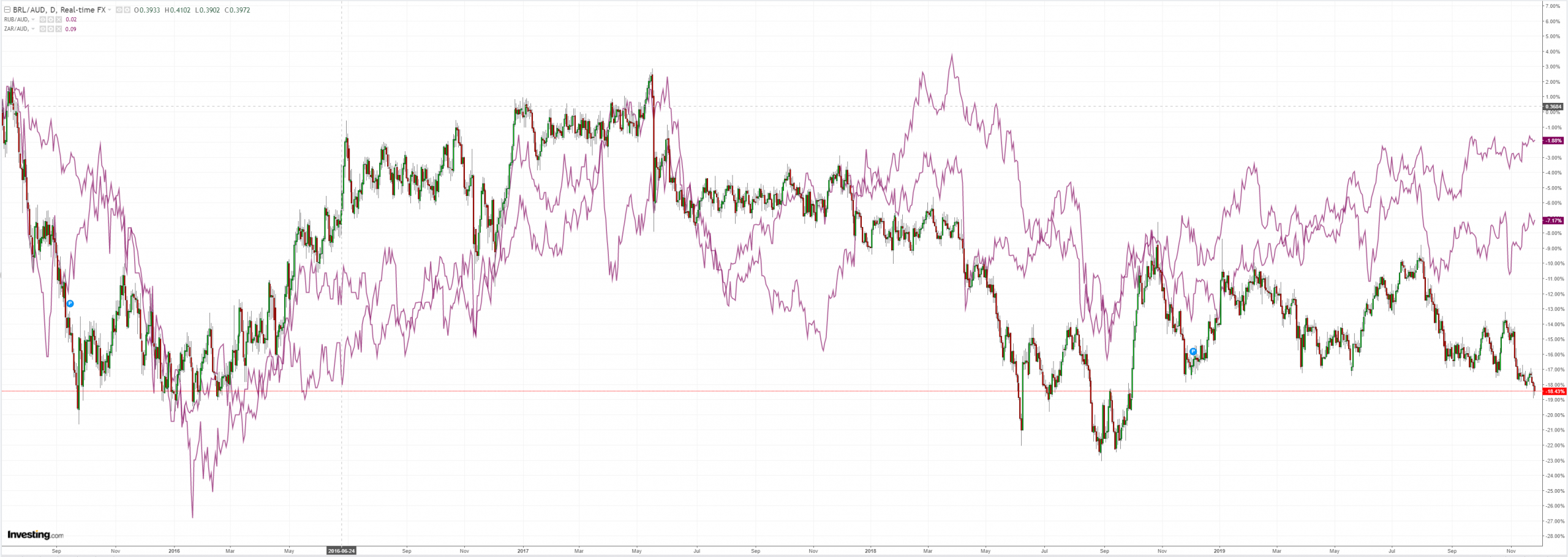

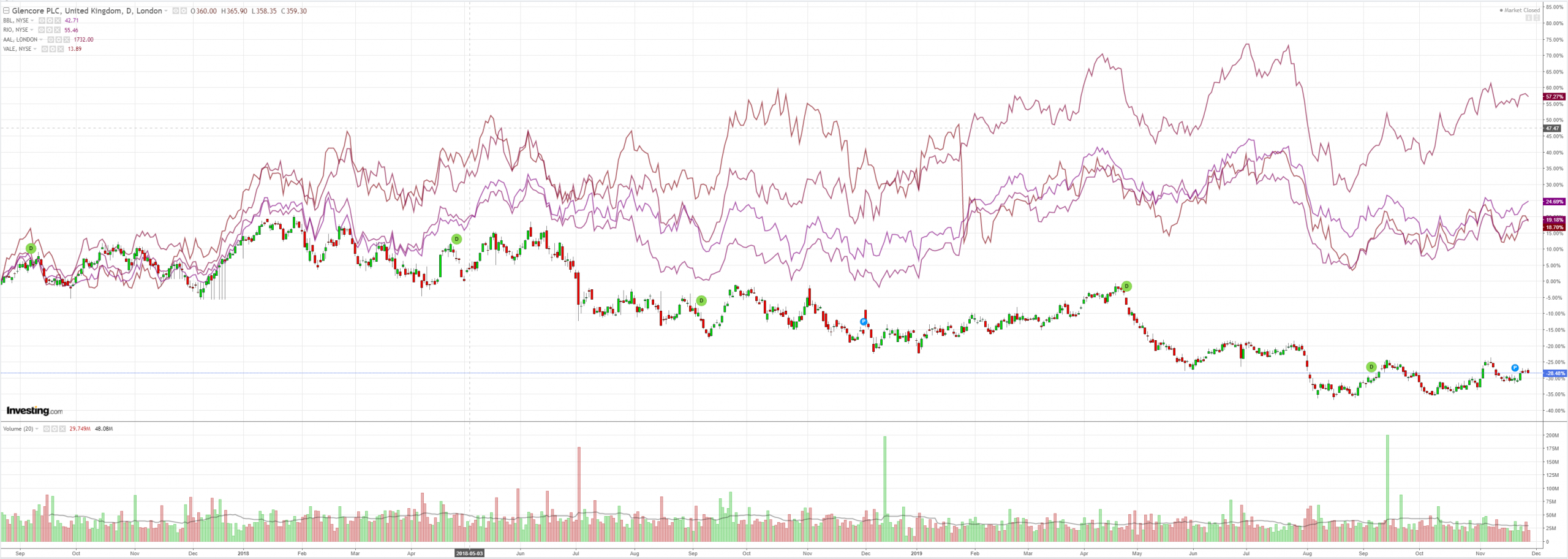

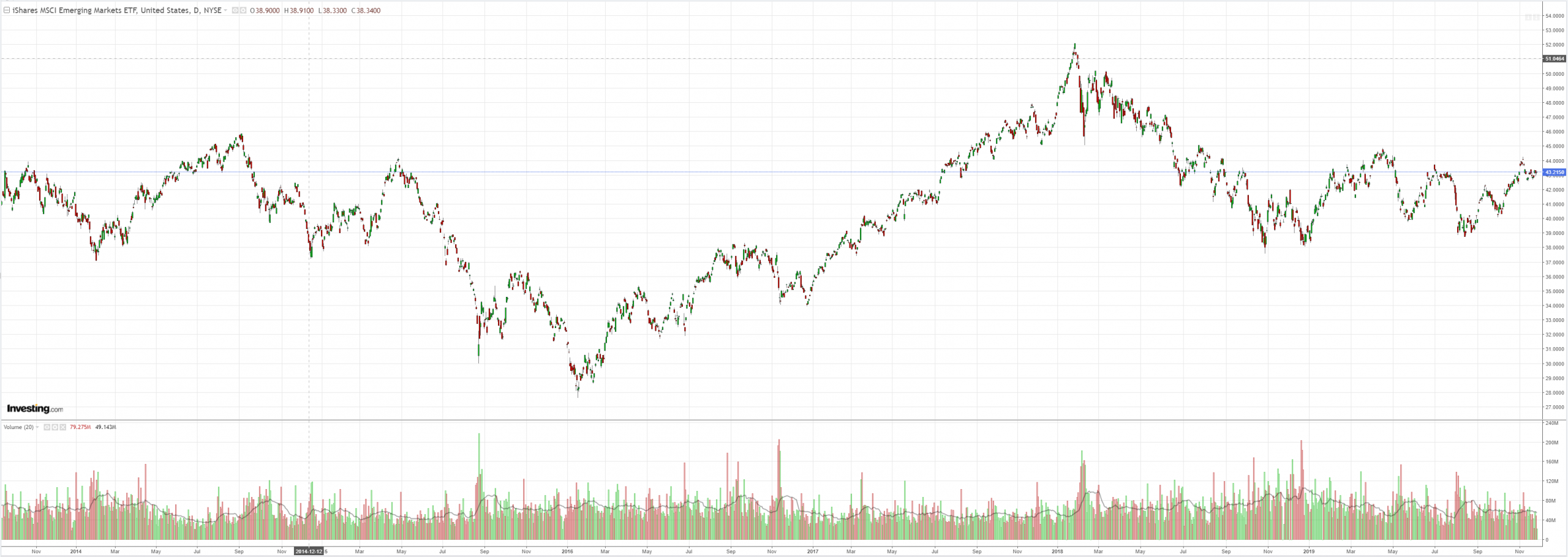

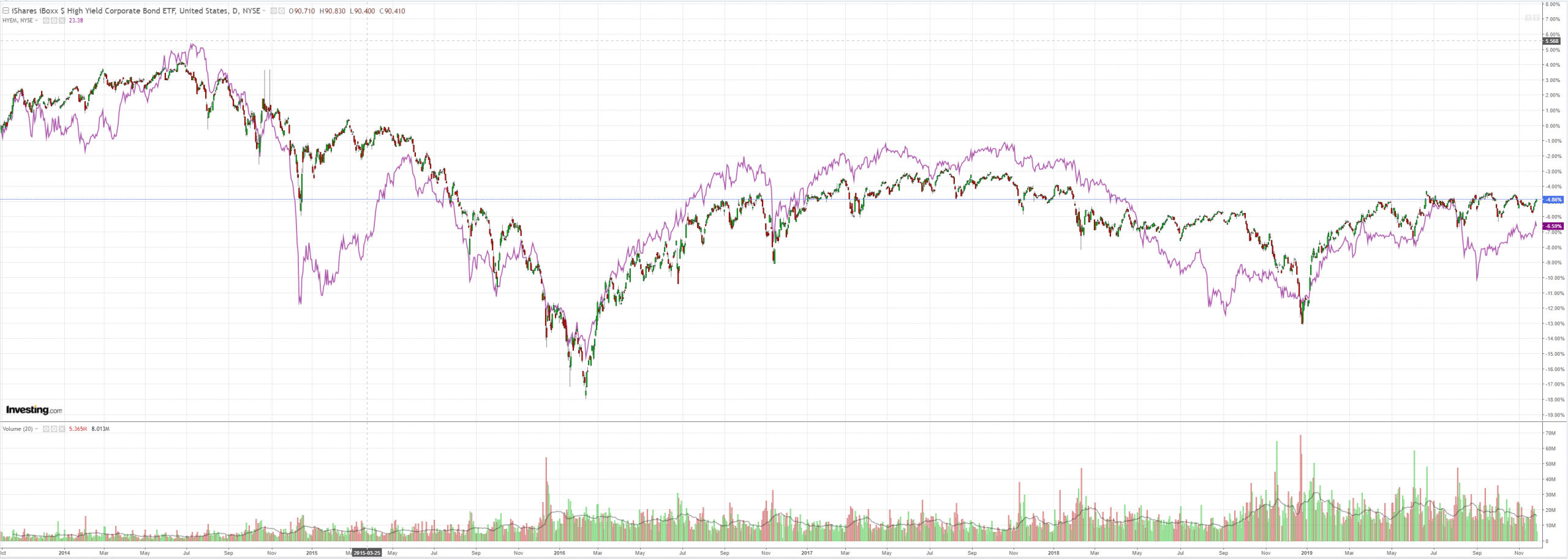

Such US growth and inflation leadership boosts the USD and makes it all worse emerging markets and commodities, landing squarely on the AUD.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.