The gender gap between men’s and women’s superannuation accumulation has once again come to the fore with the federal government’s review of the retirement income system being urged by a group of 100 high-powered business women and men to examine the specific needs of women. Sandra Buckley, the CEO of Women in Super, says men always have more superannuation than women, whereas Australian Institute of Superannuation Trustees CEO, Eva Scheerlinck, notes that most women have broken work patterns and are more likely to work part-time. From The New Daily:

“There have been at least five reviews into or including superannuation [Cooper, Henry, Financial System Inquiry, Productivity Commission, Hayne Royal Commission] in the past decade and the issue of women’s retirement outcomes was not explicitly addressed, so we continue to have the situation whereby women are retiring with less than half the superannuation of men,” Ms Buckley said…

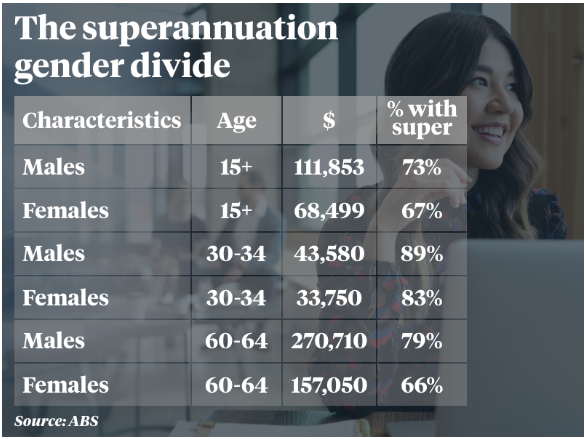

Currently, 23 per cent of women retire with no super, and one in three women has no super account, WIS found.

“Men always have more super than women,” Ms Buckley said.

“In the early years of careers until the ages of 30-34 there is a less than 10 per cent difference. However, the gap steadily grows to 33 per cent at 55-59 before closing at 79 per cent at 60-64.”

The inherent bias against women’s superannuation stems from the inequitable way that concessions are distributed, which disadvantages lower paid workers irrespective of gender.

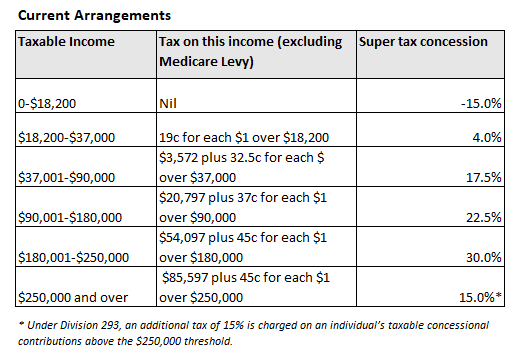

Under current arrangements, superannuation contributions/earnings are taxed at a flat rate of 15%. Accordingly, those on lower incomes receive minimal concessions (or are penalised), whereas those on higher incomes receive the biggest tax concessions:

Advertisement

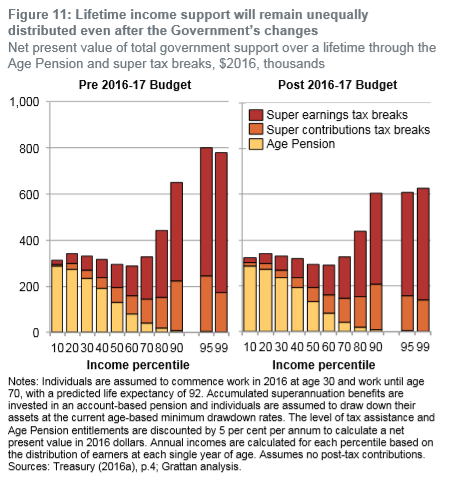

Division 293 remedies the situation for those very high income earners above $250,000. But even then, the lion’s share of superannuation concessions still flow to the highest income earners, whereas the lower income earners continue to be disadvantaged by the system, as shown in the next chart from the Grattan Institute:

Advertisement

Since women typically earn less then men over their working lives – because they tend to work in lower paid professions (e.g. nursing and teaching), work part-time, or take time off from working to raise children – they obviously accumulate much lower superannuation balances.

The first best solution to this problem is to reform the superannuation system to make concessions more equitable and sustainable.

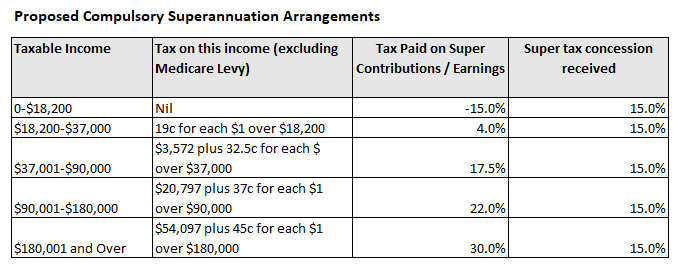

In particular, the 15% flat tax on contributions/earnings should be replaced with a flat-rate refundable tax offset (e.g. 15%):

Advertisement

This way, everyone that contributes to superannuation would receive the same concession, the system would be made progressive, and lower income earners – be they male or female – would get a better deal.

The 30-year old rule that stops earnings under $450 from an employer in a month from attracting superannuation should also be removed.

Advertisement

As an aside, the growing concerns over the disparity between male/female superannuation and earnings is largely a non-issue. We are family units whereby husbands/wives pool their financial resources – both incomes and savings – and share workloads, be it paid or domestic.

Moreover, when couples divorce, financial resources are split-up and distributed among the spouses, including superannuation savings.

Instead of fighting manufactured gender wars, policy makers should focus on eliminating poverty, irrespective of gender. Making superannuation concessions more equitable is a good start.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.