Over the past few months, equity investors have received a lot of good news. First, the Fed cut interest rates at the end of July. Next, the ECB announced it would restart QE in November, adding €20 billion per month for as long as it deems necessary. Two weeks ago, we saw “significant progress” from the US and China on trade with Phase 1 of a much larger deal, according to White House officials. If that wasn’t enough, the Fed decided to deal with front-end funding market distress by announcing a US$60 billion-per-month balance sheet expansion, and Brexit seems to be reaching a conclusion.

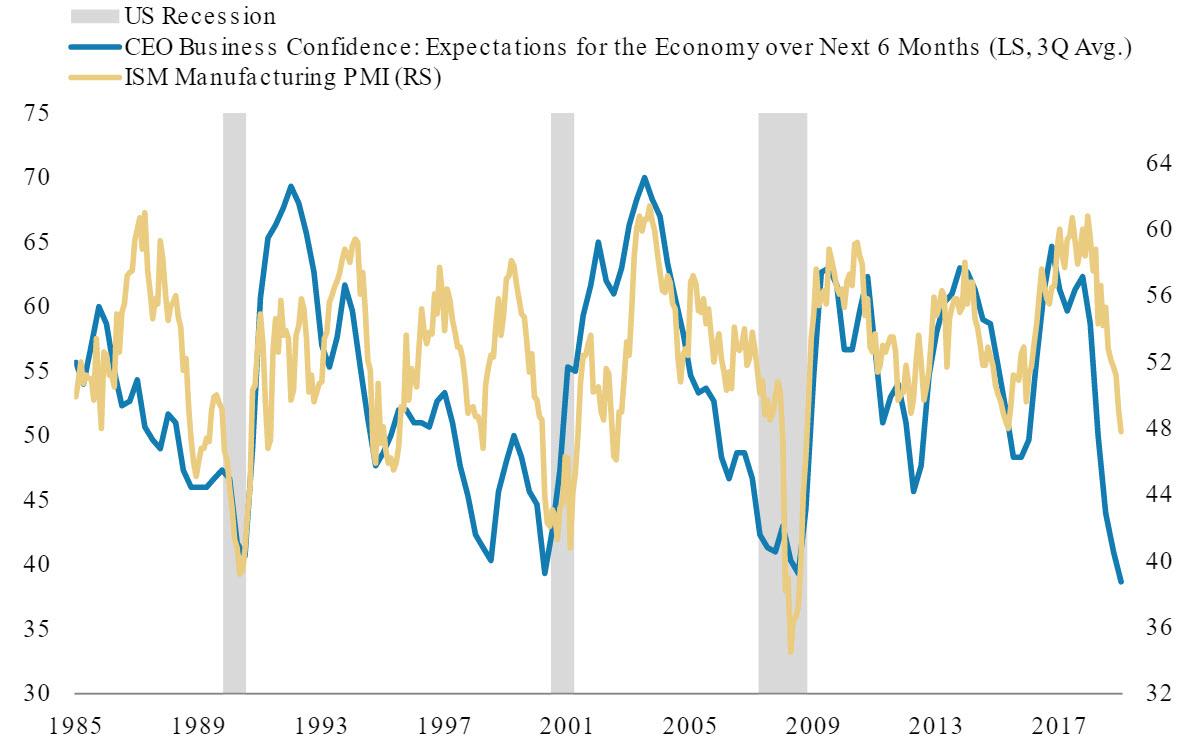

So why hasn’t the S&P 500 been able to definitively break out above July’s highs? We think it’s pretty simple. Growth has disappointed this year, and many leading indicators suggest it will continue to do so, particularly in the US (Exhibit 1). This is precisely why so many central banks are easing and why there are calls for more fiscal stimulus.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.