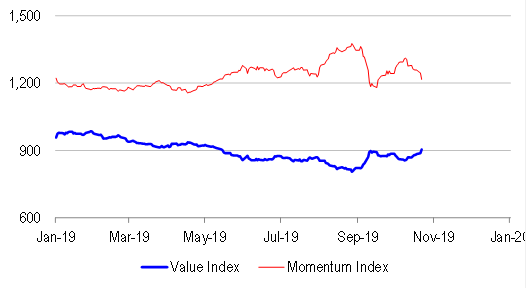

Overnight, and indeed, over the past week, we have seen a very sharp rotation into value factors and out of momentum factors. This follows on from the sharp rotation we saw from late August to early September. To be sure, there was a brief intercession in the rotation from mid-September to early October. But now, on a sector neutral, equally-weighted basis, the value index has broken through its September peak, while the momentum index is close to re-testing its September lows.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.