The 2018 Federal Budget expanded the Pension Loan Scheme (PLS) to allow all retirees to obtain a state run reverse mortgage, which allowed pensioners to boost their retirement income by up to $17,800 for a couple without impacting on their eligibility for the pension or other benefits.

Now, seniors groups are demanding that the 5.25% interest rate attached to the PLS be lowered in line with rate cuts by the RBA:

The current 5.25 per cent interest rate for reverse mortgages under the Government’s Pension Loans Scheme has not fallen despite three official cash rate cuts this year, most recently to 0.75 per cent in October…

Retiree groups have accused the Government of double standards for holding the reverse mortgage rate at 5.25 per cent since 1987 while slamming banks for not passing on official rate cuts in full to mortgage borrowers.

National Seniors Australia chief advocate Ian Henschke said the unchanged reverse mortgage rate exposed the Government to claims “assets-rich and cash poor” pensioners were being gouged.

“If you’re attacking the banks, you’ve got to do something about your own house and get it in order. They (the Government) are balancing the budget on the backs of pensioners and retirees,” Mr Henschke told the ABC’s AM program…

While the review will consider recent Reserve Bank rate cuts, Mr Frydenberg said the Government’s reverse mortgage rate was lower than deals offered in the private sector.

“The interest rates for reverse mortgages are above standard mortgage rates reflecting their higher risk,” Mr Frydenberg said in a statement.

“The Government continually monitors the appropriateness of the interest rate for the Pension Loan Scheme to ensure the rates are reflective of current market conditions.”

On the face of it, the seniors groups have a point: the PLS should be adjusted to reflect changing official interest rates as well as market mortgage rates.

That said, there is a bigger policy issue here.

The PLS changes in the 2018 Budget are arguably retrograde and unfair to younger Australians, since it helps to ‘lock’ older empty nesters in their family friendly homes by removing their incentive to sell.

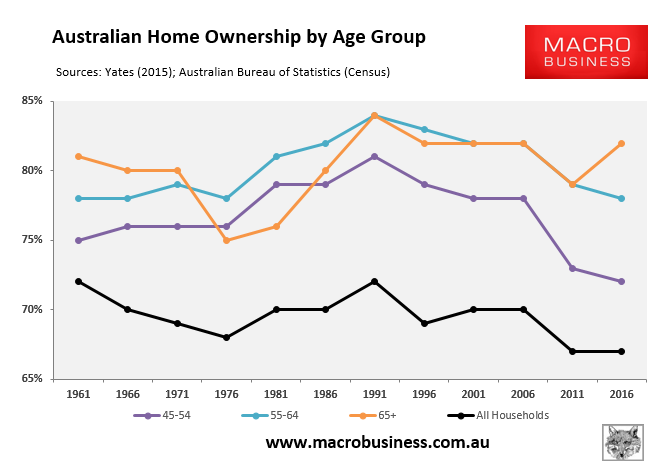

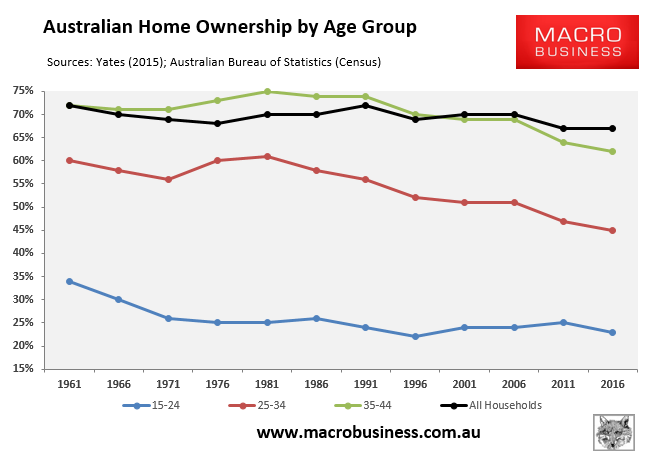

That is, the PLS reinforces current housing inequities, whereby older Australians have maintain high rates of home ownership while younger generations’ home ownership rates have plummeted:

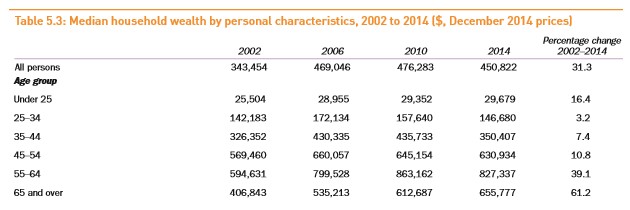

The older generation has enjoyed massive increases in net wealth:

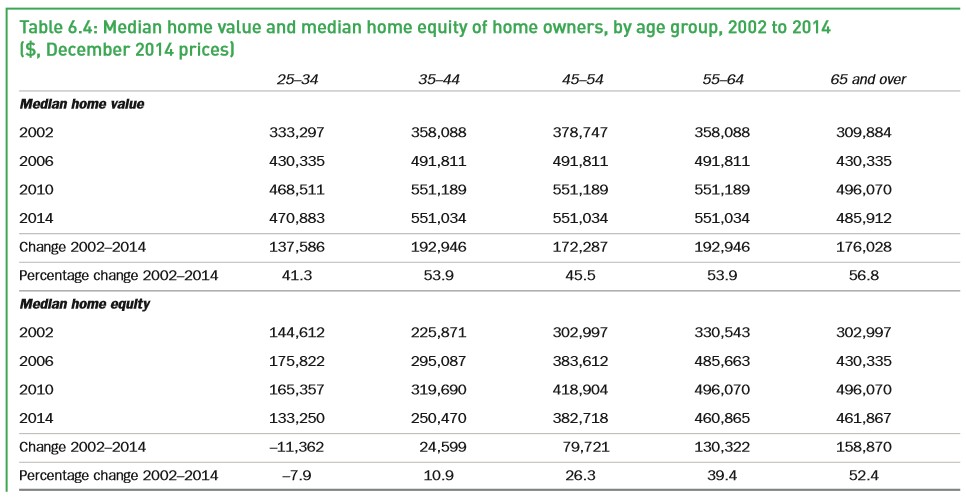

Largely because they have enjoyed the biggest gains in home equity:

The fairer policy solution would be to expand the PLS even further in concert with:

- Including one’s principal place of residence in the assets test for the Aged Pension at some point in the future (e.g. 1 July 2022), thus allowing current retirees and prospective retirees adequate time to make arrangements; and

- Raising the overall pension asset test threshold as well as the base rate.

Under this approach, asset rich pensioners choosing to remain in place could continue to receive an income stream as they do now under the Aged Pension, but with less drain on the Budget and on younger taxpayers. But they would similarly be incentivised to move as the family home would no longer be viewed as a tax free shelter.

Poorer ‘houseless’ pensioners would also be made better-off via the combination of a higher asset test threshold and a higher pension base rate.