DXY was soft as EUR and CNY climbed:

The Australian dollar blasted higher versus DMs:

And EMS:

Gold was stable:

Oil fell:

Metals too:

And miners:

Plus EM stocks:

EM junk is risk on:

As all bonds were bid:

And stocks hit record highs:

It was a not-hawkish Fed that done it:

Information received since the Federal Open Market Committee met in September indicates that the labor market remains strong and that economic activity has been rising at a moderate rate. Job gains have been solid, on average, in recent months, and the unemployment rate has remained low. Although household spending has been rising at a strong pace, business fixed investment and exports remain weak. On a 12-month basis, overall inflation and inflation for items other than food and energy are running below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. In light of the implications of global developments for the economic outlook as well as muted inflation pressures, the Committee decided to lower the target range for the federal funds rate to 1-1/2 to 1-3/4 percent. This action supports the Committee’s view that sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective are the most likely outcomes, but uncertainties about this outlook remain. The Committee will continue to monitor the implications of incoming information for the economic outlook as it assesses the appropriate path of the target range for the federal funds rate.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

Weirdly, it is was not what is a quite hawkish statement that sent markets mad. It was this from Jay Powell in the conference:

“I think we would need to see a really significant move up in inflation that’s persistent before we even consider raising rates to address inflation concerns.”

I say “weirdly” because that is self-evident. The more important take out is that the Fed is not going to cut again unless things get weaker, so I’d fade the bounce.

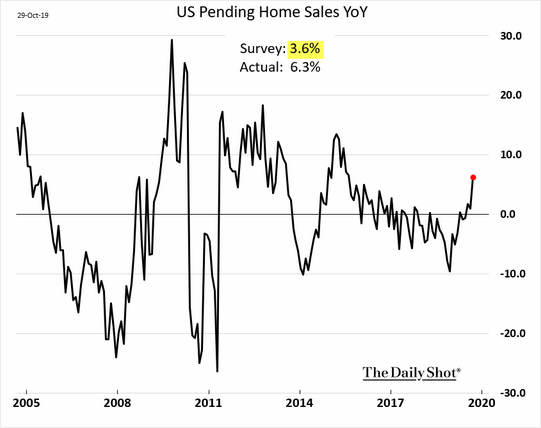

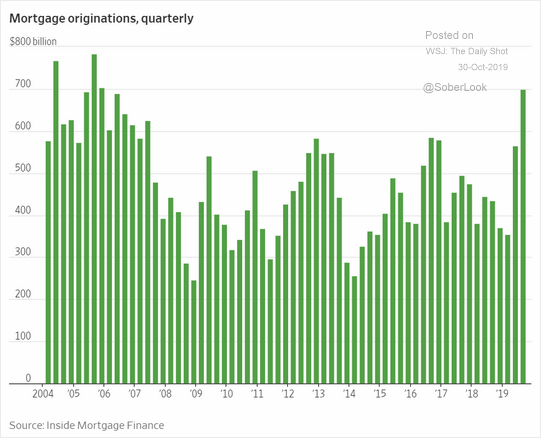

At this stage, the US economy has slowed but housing is showing signs of life:

So the Fed may be done unless or until things get worse in some other way.

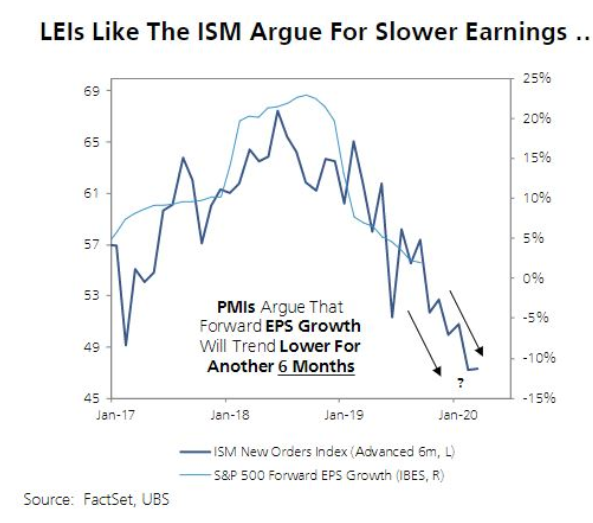

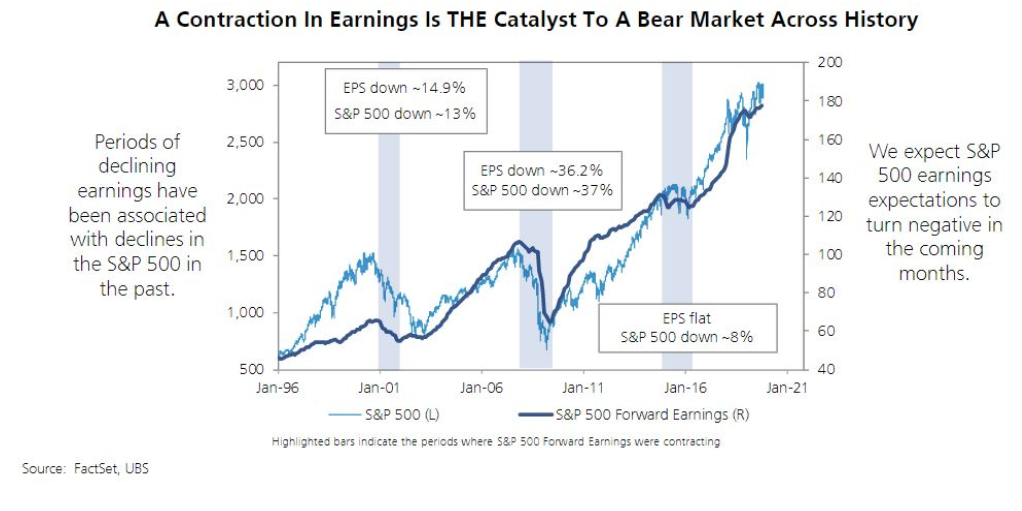

Despite new highs today, that could still be the stock market. It has rosy growth forecasts embedded for next year that will need to be slashed before long, via UBS:

And when the earnings outlook falls so do stocks:

Which would remind the Fed who is boss and get it cutting again.

Anyways, for today, I see this as noise. The Fed’s insurance cuts are done unless or until things get worse. That is AUD dovish not hawkish.