So say the excellent Damien Boey at Credit Suisse:

RBA Deputy Governor Debelle has just delivered a “glass half-empty” speech about the housing construction cycle. Key points were as follows:

2020 shapes up as being the low year for residential construction, but the Bank can see through the trough to the other side.

Long lead times on higher-density construction, and tight lending conditions for developers may elongate the downturn.

The house price cycle has turned, but in the opposite way to the construction cycle, with different profiles across states.

Falling house prices have exerted a negative wealth effect on consumption. The Bank has estimated that every 10% fall in house prices tends to cause a 1.5% fall in consumption over time.

Falling house prices have negative impacted state stamp duty receipts … but this has not resulted in state governments changing their expenditure plans materially, so there has not been a pro-cyclical impact. Noting that state governments are funding constrained, unlike Federal governments, Debelle is making a veiled reference to the fact that many state governments have presumed upon Federal/RBA funding to finance future infrastructure spending, without fleshing out the details of how.

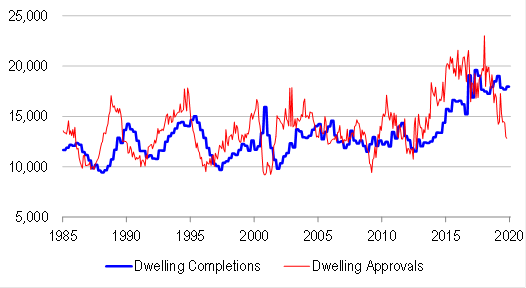

We totally understand where Debelle is coming from. Building approvals are tracking at much lower levels than completions at present, with the lead-lag between approvals and completions lengthening in recent years. So it makes sense that the Bank is bracing itself for the worst of the downturn to come. We also think that supply cuts are a key part of the equilibrating mechanism to support house prices, given that demand has been restrained for some time.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.