Via the excellent Damien Boey at Credit Suisse:

Minutes from the RBA’s early October meeting were dovish. The Bank highlighted:

- Its easing bias.

- That rising house prices are not a constraint on policy easing right now.

- The low(er) exchange rate as an especially important channel for rate cuts to be transmitted to the broader economy.

One paragraph in particular caught our eye(s):

“Members also considered the argument that some monetary stimulus should be kept in reserve to address any future negative shocks. However, that argument requires changes in interest rates to be the key driver of demand, rather than the level of interest rates, which experience has shown to be the more important determinant. Members concluded that the Board could reduce the likelihood of a negative shock leading to outcomes that materially undershot the Bank’s goals by strengthening the starting point for the economy.”

We struggle to understand and translate exactly what these sentences actually mean. But our best guess is as follows. The Bank’s view is that the level of interest rates inversely correlates with the rate of growth in GDP. Therefore, low interest rates set the scene for strong real GDP growth. Now, there is uncertainty as to whether further cuts from low levels will cause a meaningful acceleration in real GDP growth. Therefore, the ideal solution is to lift the starting point for real GDP growth now, so that even after a negative shock, the final growth rate does not look too bad.

We think that this thinking is riddled with contradictions. These notwithstanding, the Bank is clearly saying that it is more concerned with building a buffer in real GDP growth now, than building a buffer in interest rates. Indeed, it is so concerned with building a growth buffer – more growth today, that it is almost resigned to the view that there might not be much growth to be had tomorrow. This is an extraordinary turnaround in policy thinking. Over the past few years, Bank officials have told us how important long-term financial stability is. Now, they are saying that today is all that matters – “que sera sera” in the longer-term.

If our interpretation is correct, this is the most dovish statement that the RBA could make. Lower rates, and growth at any cost. Interestingly, officials did reiterate its macro-prudential framework in the minutes in its discussion of house prices – but in a very skewed way. Officials suggested that they are not worried about rising house prices just yet – but they will worry when there is accumulated evidence of a leverage build up. We all know that asset prices lead credit aggregates, and the RBA is waiting to see a clear (lagging) trend in credit growth. So in other words, the RBA is saying that it is willing to apply macro-prudential policy like it did before – after the fact, or when the “horse has bolted”.

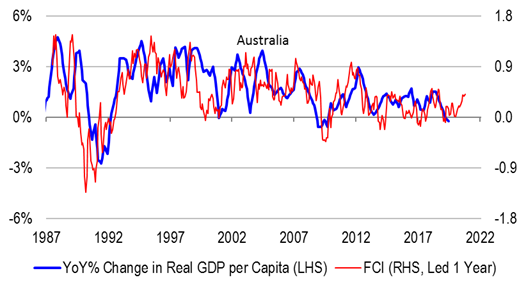

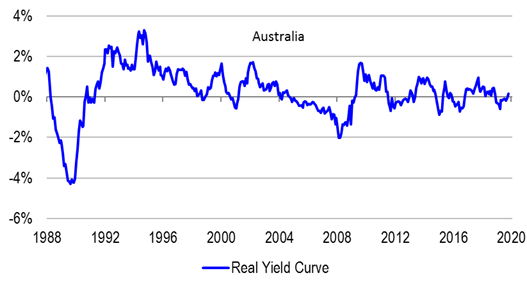

For what it is worth, we think that the RBA is partly right in its thesis that the level of rates lines up with the rate of change in real GDP. It is not so much the absolute level of real interest rates that matters – nor strictly the rate of change. Rather, it is the de-trended level of real interest rates that matters. The trouble is that the trend is changing through time, as our concept of neutral changes. And the best, real-time proxy for the trend in real interest rates is simply the inflation-indexed 10-year bond yield (term risk premia distortions notwithstanding). For this reason, the slope of the real yield curve is a key input into our broader assessment of financial conditions. Right now, the curve is slightly upward sloping, consistent with reflation. There are other factors pointing in the same direction – undershooting in the AUD/USD relative to fundamentals (terms of trade, real interest rate differentials, relative currency scarcity), positive real wage growth, and an improving credit impulse (fiscal expansion, and terms of trade gains). Indeed, our proprietary financial conditions index (FCI) is pointing to rather easy policy settings, consistent with material re-acceleration in growth over the next year.

With all of this in mind, we think that the RBA is going to err on the side of over-stimulating the economy. So will the Federal government “push comes to shove”. All of this is very supportive of curve steepening in the fixed income (flat-to-higher long-term bond yields, lower short rates). It is also supportive of value investing within the equity market, especially in the domestic cyclical and financial spaces. For further discussion, please see our recent article “The case for curve steepening: part II” dated 10 October 2019.

Sometimes you have to look beyond your quanty models. The RBA said a lot of sensible stuff for the first time yesterday:

The Board’s discussions also focused on the ongoing strength in employment growth. The period of strong employment growth had not reduced spare capacity in the labour market significantly. Almost all of the strength in employment growth over the preceding three years had been matched by higher participation, so there had been little progress on reducing unemployment and underemployment. It was also possible that participation was rising partly in response to weak growth in incomes. Moreover, employment growth was forecast to slow over the period ahead.

Members also discussed the possibility that policy stimulus might be less effective than past experience suggests. They recognised that some transmission channels, such as a pick-up in borrowing or the effect on the home-building sector, may not be operating in the same way as in the past, and that the negative effect of low interest rates on the income and confidence of savers might be more significant. Notwithstanding this, transmission through the exchange rate channel was still considered likely to work effectively, and evidence suggested that the positive effects of lower interest rates on aggregate household cash flows via lower debt repayments was likely to support household spending, given that household interest payments exceed receipts by more than two to one.

Members also noted that the housing market and other asset prices might be overly inflated by lower interest rates. Members acknowledged that asset prices were part of the transmission mechanism of policy, including by encouraging home building. By themselves, higher asset prices were considered unlikely to present a risk to macroeconomic and financial stability. This assessment would need to be reviewed if rapidly increasing asset prices were accompanied by materially faster credit growth, weak lending standards and rising leverage. Although household debt was still considered high, members saw only a limited risk of excessive borrowing at the current juncture: household disposable income growth (and thus borrowing capacity) is weak; the memory of recent housing price falls is still fresh; and banks are still quite cautious in their appetite to lend. Nonetheless, members assessed that close monitoring of this risk was warranted.

Members concluded that these various factors did not outweigh the case for a further easing of monetary policy at the present meeting. Taking into account all the available information, including the reductions in interest rates since the middle of the year, the Board decided to lower the cash rate by a further 25 basis points. Members judged that lower interest rates would help reduce spare capacity in the economy by supporting employment and income growth and providing greater confidence that inflation would be consistent with the medium-term target. Members also noted the trend to lower interest rates globally and the effect this was having on the Australian economy and inflation outcomes.

The RBA is slowly recognising the structural changes wrought upon the economy by destructive population growth, without naming it:

- income can’t grow as immigration creates its own supply and ravages work security;

- dwelling construction has been dislocated by the defect crisis arising from breakneck approvals and foreign builders;

- house price wealth effects are waning as household debt hits extremes and bear monitoring as the Government pours in more warm bodies, and

- these are structural changes that mean interest rates need to be structurally lower if we are to generate inflation.

A rise in a leading financial conditions index is all well and good but it, too, is likely to misfire in these changed circumstances.

To my mind, the RBA is finally turning sane. It can’t rebuild an interest rate buffer in this economy. Indeed, it is still miles behind the curve in its easing efforts regarding inflation and growth. And dead ahead is an entirely predictable terms of trade crash that will make it all worse.

Preserving ammunition for a cyclical shock when a structural change is already demolishing everything in site makes no sense.