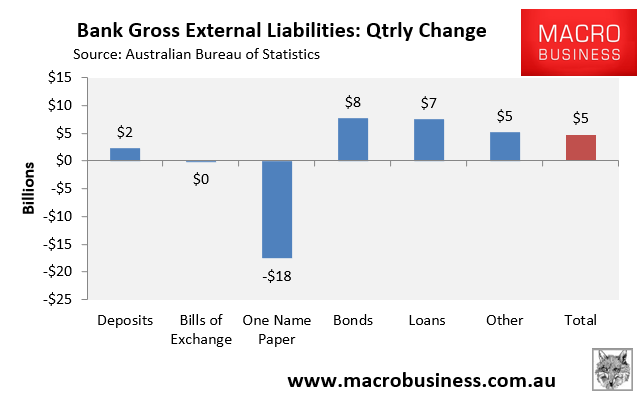

The Australian Bureau of Statistics (ABS) recently released its National Financial Accounts for the June quarter, which revealed a 0.5% quarterly rise in Australian banks’ gross external liabilities (offshore borrowings), but a 0.6% decrease over the year.

Bonds (+$8 billion), Loans (+$7 billion) and Other (+$5 billion) drove the quarterly rise in offshore borrowings by the banks over the June quarter, partly offset by an $18 billion fall in One Name Paper:

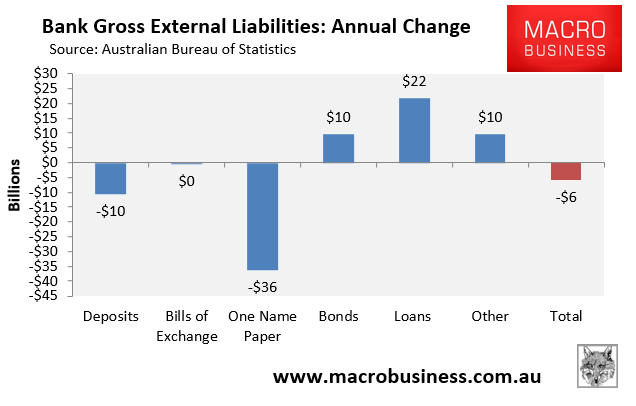

Over the year to June 2019, Australian banks’ offshore borrowings fell by $6 billion, with falls in One Name Paper (-$36 billion) and Deposits (-$10 billion) outweighing rises in Loans (+$22 billion), Bonds (+$10 billion) and Other (+$10 billion):

Advertisement